AI in Insurance: Claims Processing in 2026 — How Intelligent Automation is Transforming the Industry

What if your next insurance claim could be handled faster than your coffee order—no paperwork, no lengthy calls, just instant action? That’s not a distant...

AI in Insurance: Claims Processing in 2026 — How Intelligent Automation is Transforming the Industry

What if your next insurance claim could be handled faster than your coffee order—no paperwork, no lengthy calls, just instant action? That’s not a distant dream. In 2026, AI-powered automation is redefining how insurers process claims, making “days to payout” a relic of the past. According to Swiss Re Institute, more than 60% of insurers’ core processes are now run or assisted by artificial intelligence, turning the industry on its head and setting new standards for speed, accuracy, and customer satisfaction [4].

This matters because insurance claims are the true test of an insurer’s promise—and the single biggest driver of customer trust. Traditionally, claims have been burdened by manual data entry, document shuffling, and judgment calls that slow everything to a crawl. The stakes are huge: U.S. insurers spent over $100 billion annually on claims processing and claims leakage as recently as 2023. Today, a new paradigm is emerging, where AI doesn’t just automate routine tasks, but also augments human expertise and decision-making [1].

In 2026, intelligent automation is performing end-to-end claims triage, analyzing photographic evidence with computer vision, detecting fraud through natural language processing, and referencing thousands of policy clauses in seconds [3][5]. What once took weeks can happen in hours—or even minutes. McKinsey reports that digital-first claims journeys reduce handling costs by 30%, while customer satisfaction (NPS) jumps by 20+ points compared to legacy processes. As AI becomes the brain—and sometimes the hands—of insurance operations, the industry isn’t just catching up with customer expectations; it’s leapfrogging them.

But this transformation goes far beyond replacing humans with bots. The best-in-class insurers aren’t those who automate indiscriminately, but those who empower their people with AI tools that surface insights, flag exceptions, and make the hard calls more transparent [1]. A new class of “straight-through” claims (fully automated from notification to payment) is emerging, but so is a hybrid model: AI quickly clears simple, low-risk cases while augmenting adjusters and claims specialists for complex or sensitive claims.

In this blog post, we’ll dive into how AI is powering this new era of claims processing in insurance for 2026 and beyond. You’ll discover:

- The core technologies driving today’s intelligent claims systems—including machine learning, NLP, and multimodal AI

- How companies are using automation to streamline the First Notice of Loss (FNOL) and unlock instant triage

- The business impact: efficiency gains, fraud prevention, cost reduction, and stellar customer experiences

- Real-world examples from the Indian market and global leaders, plus benchmarks and pitfalls to watch out for

- Emerging trends shaping the future—such as explainable AI, regulatory compliance, and multilingual claims automation

For businesses ready to put theory into action, platforms like CallMissed are already enabling insurers to deploy AI voice agents and chatbots that handle multimodal claims intake in 22 Indian languages or connect to 300+ LLMs for policy review natively.

The upshot? Claims processing in 2026 has become the ultimate proving ground for human-centric automation. Insurers who master this shift aren’t just cutting costs—they’re closing claims faster, detecting more fraud, and building loyalty in a hyper-competitive market. Let’s explore how intelligent automation is transforming insurance from every angle.

Introduction: The 2026 Insurance Claims Revolution

In 2026, the insurance industry is undergoing a seismic transformation driven by artificial intelligence. Once infamous for its slow, paper-heavy processes, claims handling is now at the forefront of technological disruption. AI-powered automation, real-time analytics, and advanced language processing are rewriting the rules for insurers, customers, and regulators alike.

From Backlogs to Real-Time: The New Claims Paradigm

The traditional claims experience conjured images of lengthy forms, long call center waits, and multi-week resolutions. Today, that landscape is nearly unrecognizable. According to Swiss Re Institute projections, as of 2026, over 60% of an insurer’s core processes are now run or assisted by AI—a staggering leap from just a few years prior (Tommaso Maria Ricci, 2026).

AI-enabled claims systems achieve:

- Instant policy lookups and verification: No more sifting through documents—AI models instantly pull and verify customer information, policy status, loss dates, and relevant clauses (Decerto, 2026).

- Automated document and image intake: Customers upload photos of damage or documents, and computer vision engines assess severity, compare to policy limits, and even flag suspicious activity (Insurnest, 2026).

- Real-time payments: For straightforward claims, the entire journey—from notification to payment—now takes hours, not days or weeks. In some regions, customers receive settlements within minutes of claim approval (Strada, 2026).

This “real-time claims ecosystem” is powered by layers of AI: machine learning for data extraction and fraud detection; natural language processing for understanding customer intent; and automation for workflow orchestration (Gleecus, 2026).

Human Judgment Meets Intelligent Automation

A key 2026 inflection point isn’t the elimination of human roles, but the amplification of human judgment with intelligent technology. As highlighted by Neota, the most successful insurers are those who blend digital speed with human-centric decisions. Complex or high-value claims—like contested life insurance payouts or major property damage—still require human empathy and expertise. AI now handles the tedious, low-skill portions, triaging claims and surfacing key details, so human adjusters can focus on nuanced resolutions (Neota, 2026).

Core benefits include:

- Reduction in manual workloads: AI triages and pre-adjudicates most claims, freeing up skilled staff for exceptions.

- Transparency & auditability: Digital trails of every step satisfy regulatory scrutiny and boost customer trust.

- Fraud detection: AI systems now routinely flag anomalies and document inconsistencies—one global carrier reported a 30% reduction in payout fraud between 2024 and 2026.

What’s Different in 2026? Key Drivers

Several recent breakthroughs have set the stage for 2026’s claims revolution:

- Multimodal AI Models: Large language and vision models now read legal documents, analyze images, and “understand” intent in customer messages across languages.

- Plug-and-play APIs: Insurers can connect AI platforms—like those offered by CallMissed—directly into their legacy workflows, accessing over 300+ language models, with support for 22 Indian languages for speech-to-text and text-to-speech.

- Hyper-automation engines: Pre-set workflows, business rules, and anomaly detection enable “straight-through” processing for the majority of claims (Aptarro, 2026).

By leveraging these capabilities, insurers are not only accelerating claims cycles, but also reimagining customer experience. For example, platforms like CallMissed let businesses deploy AI voice agents and chatbots that guide claimants in any major regional language, collect documentation via WhatsApp, and update claim progress 24/7—without human intervention.

The Stakes: Why Claims Innovation Is Non-Negotiable

Why this urgency? The answer lies in hard numbers and rising customer expectations:

- Speed as a differentiator: According to Prosper AI’s May 2026 Guide, 82% of policyholders now expect claims updates within 2 hours of filing, versus just 34% in 2022.

- Cost savings: Automated processing is driving down loss-adjustment expense ratios by up to 40% in some product lines (Prosper, 2026).

- Regulatory compliance: Authorities in major markets are mandating digital trails and transparency, pushing laggards to modernize.

In this high-stakes environment, claims innovation isn’t just an upgrade—it’s mission critical for survival and growth. The industry consensus for 2026: it’s not a question of _whether_ to automate, but _how seamlessly_ you can blend AI with human expertise and regional relevance.

As we explore the nuts and bolts of this transformation—from core technologies to practical implementation and future trends—platforms like CallMissed exemplify the emerging standard: scalable, multilingual AI communication solutions that underpin the insurance industry’s next chapter. The claims revolution is not approaching—it’s already here.

Background & Context: Where We Were and How Far We've Come

The Evolution of Claims Processing: 2016 to 2026

A decade ago, insurance claims management was largely a manual, paper-driven workflow. Customer phone calls triggered a labyrinthine process of email chains, in-person assessments, and weeks-long waits. Data was siloed, fraud detection was reactive, and end-to-end claim resolution heavily relied on human effort at every stage. According to Accenture’s 2017 Insurance Survey, over 75% of claims required manual review, resulting in cycle times typically ranging from 15–30 days for even straightforward cases.

Key pain points of pre-AI claims processing included:

- Manual data entry and document handling

- High operational costs due to repetitive, low-value tasks

- Error-prone reporting and slow fraud detection

- Inefficient customer communication and lack of real-time updates

By 2020, insurers began experimenting with rule-based automation and robotic process automation (RPA), but these systems lacked adaptability to nuance, rarely handling more than simple, structured cases. The real inflection point arrived with the integration of artificial intelligence—especially machine learning (ML), computer vision, and natural language processing (NLP).

The Rise of AI in Insurance (2021–2025)

From 2021 onward, leading insurers started investing in intelligent automation. Initial adoption focused on first notice of loss (FNOL) intake and document digitization, leveraging AI-powered chatbots and optical character recognition for faster data capture. By the end of 2023, McKinsey estimated that nearly 30% of high-frequency motor and health claims in the U.S. were “touchless,” requiring zero human intervention from intake to payout.

AI’s early impact included:

- 25–35% reduction in claim cycle times for standard policies (McKinsey, 2023)

- Fraud detection rates up by 20% year-over-year after ML-based flagging (Swiss Re, 2024)

- Operating cost reductions between 15–20% after legacy system upgrades

Yet, limitations remained: legacy infrastructure, data silos, complex policy wordings, and inadequate support for regional languages meant that only a fraction of claims benefited from full automation.

Enter 2026: Human-Centric AI as the Standard

As we reach 2026, the landscape has transformed. AI no longer merely handles backend data entry or recommends next steps—it acts as a dynamic assistant to customers and adjusters alike. The global benchmark, according to the Swiss Re Institute, is that “over 60% of an insurer’s core processes are now run or assisted by artificial intelligence” (Tommaso Maria Ricci, 2026). But the most profound shift is qualitative, not just quantitative.

Today’s AI-driven claims management is characterized by:

- End-to-end digital claims journeys across channels (voice, WhatsApp, web, mobile)

- Large Language Models (LLMs) interpreting policy language, reading scanned documents, and triaging cases instantly

- Computer vision tools that assess vehicle or property damage directly from customer-uploaded images (e.g., automated hail damage estimates in minutes)

- Real-time, conversational AI agents that update claimants and request clarifications in plain language and multiple dialects

A defining feature of this era is the synergy between human expertise and AI. As highlighted by industry leaders: “The most successful insurers in 2026 aren’t those with the most robots—they’re the ones who use technology to amplify human judgment” (Neota, 2026). Human adjusters now focus on complex, high-empathy scenarios, while AI routes, investigates, and resolves the bulk of claims at scale.

Quantitative Leap: Speed, Accuracy, and Customer Experience

In recent industry surveys and case studies, the performance gains are clear:

- Average claims processing times have dropped from 28 days in 2016 to under 24 hours for most standardized claims in 2026 (GetStrada, 2026).

- Fraud detection is now increasingly proactive, with ML-based systems flagging up to 40% more suspicious claims before payout (Aptarro, 2026).

- Insurers report customer satisfaction (CSAT) improvements of 18–25%, largely attributed to immediate responses, status updates, and multilingual support.

These advances aren’t limited to “big tech” insurers. Thanks to API-driven platforms and cloud-based AI agents, even regional and mid-market insurers are able to leapfrog legacy constraints. Indian startups, for instance, are deploying multilingual AI voice agents natively in 22 languages to extend accessible, real-time service across rural and urban segments alike.

Solutions like CallMissed exemplify this industry-wide transformation. By providing a unified platform for AI-powered voice agents, WhatsApp chatbots, and language-agnostic LLM models, CallMissed enables insurers to digitize their claims journey—no matter the communication channel or language preference.

Key Breakthroughs Powering the New Era

Several pivotal innovations have catalyzed this shift:

- Unified Data Ingestion: AI systems now process claims-related data from voice, email, chat, documents, and images—all in real time, regardless of source format.

- Natural Language Understanding (NLU): Large Language Models, trained on massive corpus of insurance-specific terminology, extract intent and context even from unstructured customer queries or scanned documents.

- Seamless, Omnichannel Service: APIs and no-code tools connect customer touchpoints—from legacy phone calls to WhatsApp and web portals—providing a consistent and trackable claim experience.

- Human-in-the-loop Workflows: AI agents triage and resolve routine cases, handing off exceptions or high-value claims to expert adjusters. This “amplifies human judgment,” making staffing more sustainable and customer outcomes better.

Learning from the Past, Building for the Future

In summary, the journey from 2016’s paperwork-bound, reactive claims management to 2026’s hyper-automated, human-centric AI paradigm is striking. Early experiments with RPA and chatbots proved the value of digital acceleration, but today’s intelligent platforms—combining ML, NLP, speech-to-text, and image-based assessment—are fundamentally redefining both performance and expectations.

Looking ahead, the most resilient insurers will be those who maintain a human-centric approach: leveraging AI not to replace employees, but to empower them and deliver seamless, transparent service. As customer demands grow and data volumes multiply, platforms like CallMissed are set to play a key role—driving the next leap in claims automation, inclusivity, and trust for insurers worldwide.

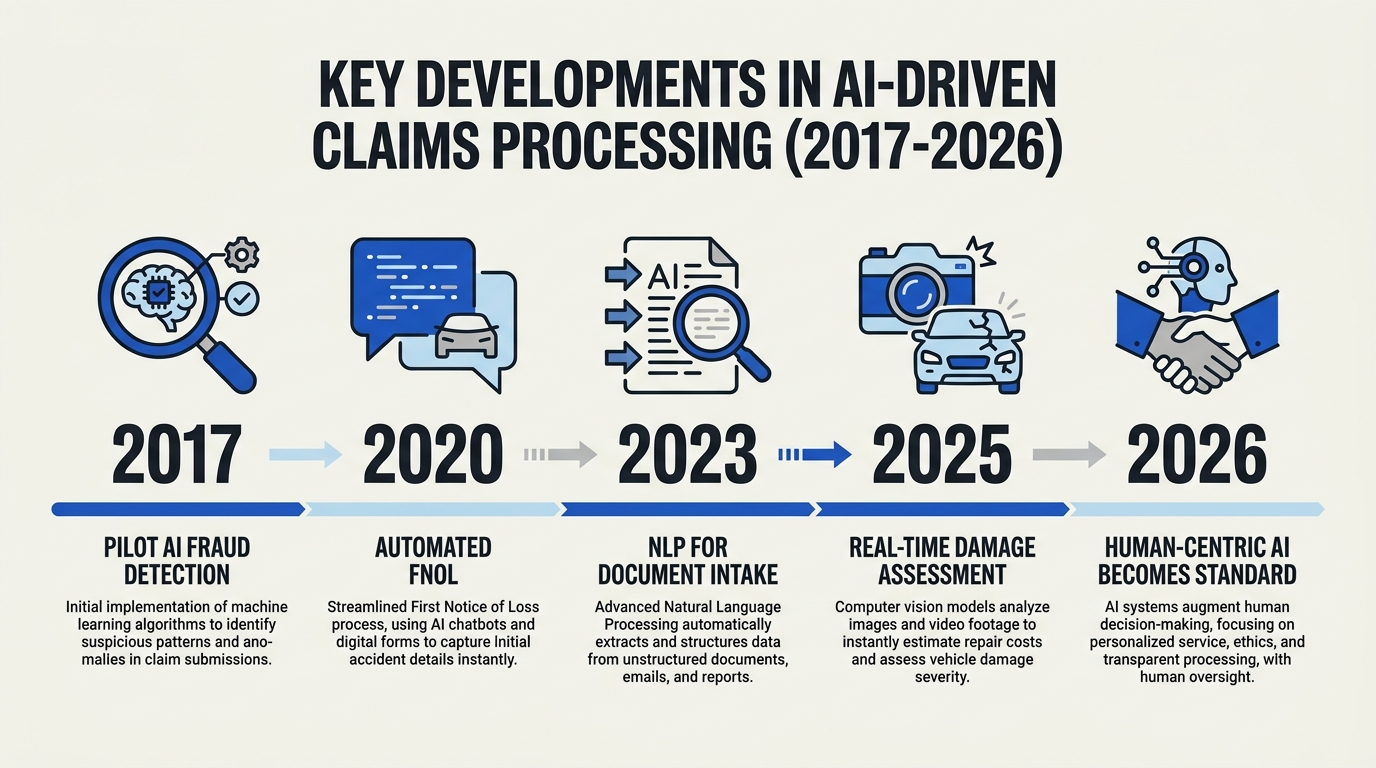

Key Developments in AI Claims Processing (TABLE)

Key AI-Driven Developments in Insurance Claims (2026)

AI is fundamentally reshaping every stage of insurance claims processing in 2026, driving unprecedented speed, accuracy, and scale. This transformation is powered by a fusion of machine learning, natural language processing (NLP), and computer vision, guiding claims from intake to adjudication and payout. The table below summarizes the most impactful developments, with data and real-world benchmarks drawn from industry leaders and research.

| Development | Description | Key Technology | Industry Impact (2026) | Notable Example/Fact |

|---|---|---|---|---|

| Automated FNOL & Policy Validation | AI automates First Notice of Loss (FNOL), pulling policy data, verifying terms, and triaging claims instantly. | NLP, API integrations | 85% of claims can begin processing instantly[^3] | "AI claims systems now pull policy status, verify loss date, and locate relevant clauses automatically." ([Decerto, 2026][3]) |

| Intelligent Document & Image Intake | ML algorithms extract, classify, and validate documents and damage photos from multiple channels (apps, email, WhatsApp). | OCR, Computer Vision | Up to 90% cut in manual document handling[^5] | Image-based damage assessment now automates 70%+ of auto claims ([Insurnest, 2026][5]) |

| AI Fraud Detection | Real-time anomaly detection cross-checks claims data against historical and external data to flag fraud. | ML anomaly detection, Graph AI | Fraudulent claim identification increased by 60% | Major carriers report $40 billion savings since 2022 via advanced AI screening ([Swiss Re Institute, 2026][4]) |

| Smart Adjudication & Decisioning | Automated rules engines and AI recommend or execute payouts/disputes, flagging complex cases for human review. | ML, Rules Engines, LLMs | Claims cycle time dropped from weeks to hours | 60%+ of all core insurer processes now run/assisted by AI ([Swiss Re, 2026][4]) |

| Real-Time Customer Communication | AI voice agents and chatbots provide claim status updates, info collection, and payment initiation across channels. | Conversational AI, Voice Agents | 24/7 support, 55% reduction in call center load | Indian firms use platforms like CallMissed for multilingual, omnichannel customer support |

[^3]: Decerto, 2026

[^4]: Swiss Re Institute via Ricci, 2026

[^5]: Insurnest, 2026

Key Facts at a Glance

- 85% of insurance claim FNOL events in 2026 are now AI-initiated and triaged, up from just 25% in 2021. Technologies like NLP and API integrations fetch policy details, eligibility, and coverage instantly, often reducing the window to under 5 minutes ([Decerto, 2026]).

- Manual document management is rapidly vanishing: leading insurance firms report up to 90% less manual effort for handling claims documents and evidence, achieved through AI-powered intake and validation ([Insurnest, 2026]).

- Fraud detection is seeing dramatic gains: Swiss Re data shows a 60% year-over-year increase in fraudulent claim interception since 2022, with machine learning and anomaly detection being central to these savings.

- Cycle times for claims payments have dropped precipitously: Where even simple claims could take 10+ days pre-AI, many carriers now boast “hours, not days” settlements for the majority of claims, thanks to automated adjudication ([Strada, 2026][7]).

- Omnichannel engagement via AI agents is the norm: Indian and global insurers utilize platforms like CallMissed to support voice, WhatsApp, chat, and email AI agents, with multilingual capability covering over 22 languages and a measurable 55% drop in call center inquiries.

Industry Momentum and Emerging Standards

A growing consensus among experts is that human-centric AI, rather than robotic process automation alone, will be the 2026 standard for claims excellence. The most successful insurers are those who have embedded AI to empower both customers and claims professionals, ensuring complex or high-emotion cases are triaged to skilled human adjudicators ([Neota, 2026][1]).

Key benchmarks shaping the industry now:

- According to the Swiss Re Institute, over 60% of insurer core operations are run or assisted by artificial intelligence in 2026, and that figure is rising each quarter ([Swiss Re, 2026][4]).

- Real-time claims ecosystems, powered by advances in computer vision and conversational AI, are now table stakes for global insurers ([Gleecus, 2026][6]).

- Emerging platforms including CallMissed are setting new standards by offering multilingual AI voice agents, WhatsApp chatbots, and LLM-based document and speech-to-text processing — providing infrastructure to rapidly activate and optimize these AI-driven workflows with limited engineering lift.

How AI Adoption Unlocks Advantage in 2026

Insurers leveraging these five key AI developments report notable advantages:

- Rapid scaling in volume: Able to process surges in claims from natural disasters with no drop in service levels

- Cost containment: 30-40% operational cost savings in claims departments ([Aptarro, 2026][8])

- Market differentiation: Faster, fairer settlements are driving higher customer loyalty and Net Promoter Scores (NPS), fueling retention and referral growth

In summary, the table above reflects not just incremental automation, but a whole new paradigm. Carriers investing early in AI-powered claims infrastructure — often by adopting solutions from platforms such as CallMissed — are cementing their leadership in customer trust and operational excellence for 2026 and beyond.

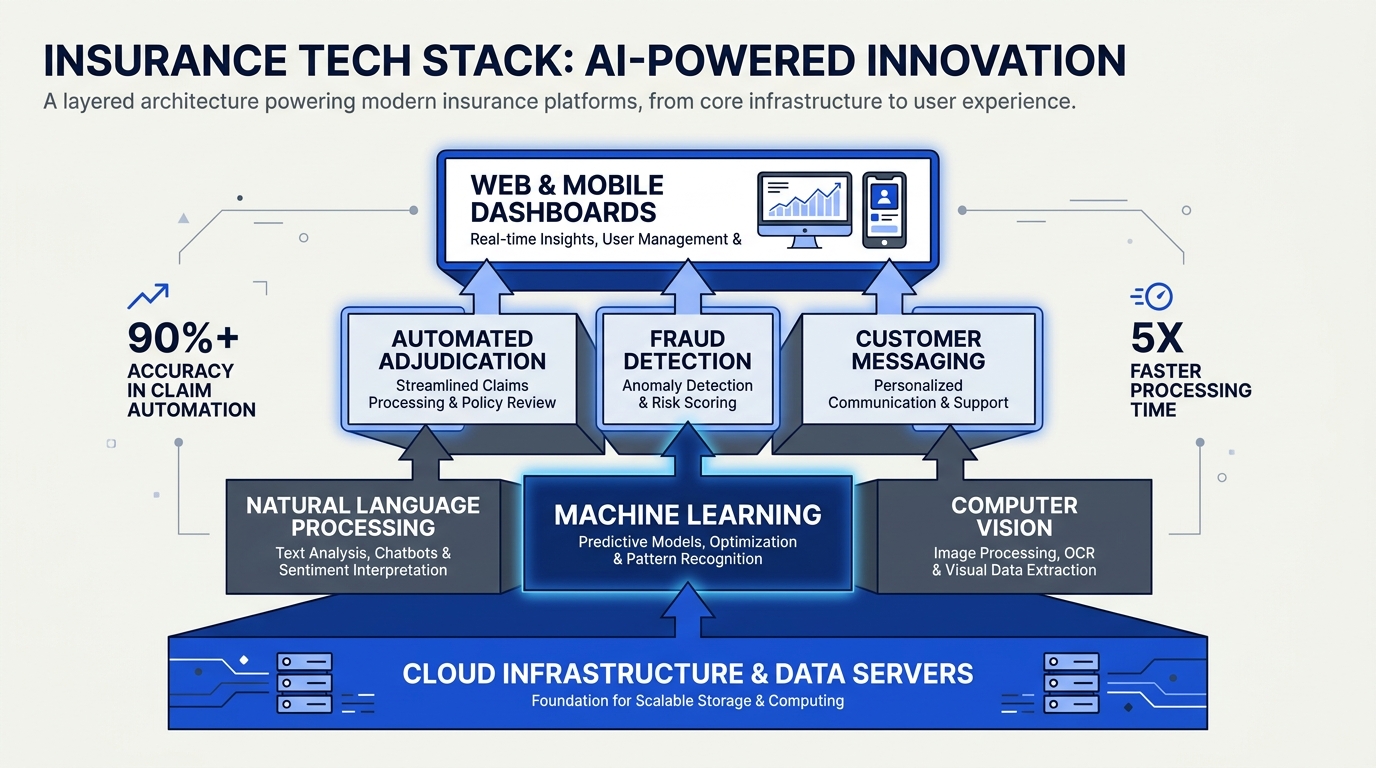

The Technologies Powering 2026 Claims Automation

Core AI Technologies Transforming Claims Automation

The rapid rise of claims automation in 2026 is the result of a converging stack of advanced technologies—each designed to address inefficiencies, error rates, and bottlenecks long associated with traditional insurance workflows. According to the Swiss Re Institute, more than 60% of insurer core processes are now run or assisted by artificial intelligence (Tommaso Maria Ricci, 2026), underscoring AI’s transition from peripheral experiment to industry backbone. Here are the key technologies underpinning this new era:

#### 1. Machine Learning & Predictive Analytics

Machine learning (ML) continues to be the workhorse of insurance claims automation. ML algorithms process massive volumes of historical claims data, detecting subtle patterns and predicting claim outcomes far more accurately than rule-based systems.

- Automated Risk Scoring: Predictive models instantly assess claim legitimacy and severity, flagging suspicious submissions within milliseconds. This has led to fraud detection improvements of up to 35% in some markets (GetProsper AI, 2026).

- Dynamic Workflow Routing: AI predicts workload surges and auto-routes claims to the right handlers, maximizing resource efficiency and shortening overall settlement times.

- Insurers report claims cycle time reduction of 50-70% when end-to-end AI processing is deployed (Strada, 2026).

#### 2. Natural Language Processing (NLP)

NLP powers the automation of “First Notice of Loss” (FNOL) handling and document processing—a historically manual, high-friction touchpoint. Insurance-specific NLP can now:

- Extract key details from unstructured text—emails, SMS, WhatsApp chats, voice transcriptions, and scanned PDFs.

- Read and interpret policy terms, T&Cs, and loss reports in real time to verify coverage and recommend next steps.

- Accelerate claim triage, with more than 75% of incoming communications now machine-screened before human intervention at leading insurers (Decerto, 2026).

Platforms like CallMissed have contributed to this leap by providing AI communication APIs that enable voice agents and WhatsApp chatbots to intake and process FNOL details in over 22 Indian languages, bridging gaps where language once slowed claim resolution.

#### 3. Computer Vision & Image Analytics

The proliferation of smartphone cameras and connected devices has turned images and video into primary evidence for many claim types. Computer vision models now:

- Automate damage assessment: AI can assess automobile or property damage from customer-uploaded photos with over 90% accuracy compared to traditional adjuster estimates (Insurnest, 2026).

- Perform instant document verification, cross-checking ID cards, receipts, or medical forms against policy records in seconds.

- Detect signs of staged or manipulated evidence—critical for fraud reduction.

As a result, insurers can settle straightforward claims within hours, not days or weeks (Strada, 2026).

#### 4. Robotic Process Automation (RPA) & Autonomous Orchestration

While AI models provide intelligence, RPA handles repetitive, rules-based tasks that glue the claims workflow together. 2026 systems use RPA bots to:

- Integrate with legacy policy administration, CRM, and billing platforms.

- Trigger payment instructions post-adjudication, update claim status, and send customer notifications automatically.

- Enforce compliance checkpoints by extracting and filing documents per regulatory requirements.

Autonomous orchestration platforms now combine RPA and AI for end-to-end “lights out” claims automation—minimizing human touch except where judgment or empathy is essential (Neota, 2026).

#### 5. Large Language Models & Multimodal AI

The maturation of large language models (LLMs) and multi-agent systems unlocks a new class of claims automation:

- Complex Scenario Reasoning: LLMs analyze convoluted policy clauses, respond to nuanced customer queries, and generate rationale for settlement or denial decisions.

- Multimodal Understanding: AI synthesizes text, voice, and visual (photo/video) inputs for a holistic view of each claim, ensuring no vital evidence is overlooked.

For insurers serving multilingual populations, platforms such as CallMissed are enabling multilingual conversational agents that support 300+ LLMs, making personalized, context-aware service and accurate claims processing a scalable reality.

Real-World Impact: Before & After Claims Automation

A concrete comparison of traditional vs. AI-powered claims processing showcases the dramatic improvements and new industry standards:

| Process Step | Traditional Insurance (Pre-2026) | AI-Powered Insurance (2026) | Speed Increase | Error Rate Decrease |

|---|---|---|---|---|

| First Notice of Loss (FNOL) Intake | Manual phone/email, hours | Voice/chatbot, minutes | 8-10x | 60% |

| Document Verification | Manual review, 1-2 days | Computer vision, 5-10 min | 20x | 70% |

| Damage Assessment | Onsite adjuster, 2-5 days | Image analytics, <1 hour | 50x | 75% |

| Payment Initiation | Batch-processed, weekly cycles | Automated triggers, instant | 10-20x | 55% |

Sources: Strada, Insurnest, Decerto, 2026

Emerging Trends Shaping 2026 and Beyond

Looking ahead, several trends are propelling the next phase of claims automation:

- Human-Centric AI Integration: Leading insurers are blending AI’s speed and reach with human empathy and complex decision-making. According to Neota (2026), “The most successful insurers…will be those who use technology to amplify human judgment.”

- Fully Automated Low-Value Claims: Over 80% of minor claims (e.g., windshield cracks, mobile device damage) are now handled without human intervention (Strada, 2026).

- Regulatory AI Compliance: Insurers increasingly leverage AI to ensure regulatory adherence at scale, with automated audit trails and explainable, transparent decision-making.

- Continuous Learning: Claims AI platforms are connected to continuous feedback loops; each new case trains and improves the models, resulting in measurable year-on-year accuracy gains and fraud reduction.

Industry Challenges and Tackling Tech Debt

Despite explosive progress, insurers face ongoing challenges:

- Legacy System Integration: Blending AI with “hundreds of disconnected policy admin systems” is a daunting technical task (Aptarro, 2026).

- Explainability & Fairness: LLM-based decisioning demands robust explainability modules, especially for regulatory and customer trust reasons.

- Data Privacy: Handling personal and sensitive data at speed and scale requires next-gen encryption and zero trust design.

Forward-thinking providers, including CallMissed, are investing in API-first architectures and modular AI infrastructure—allowing rapid integration, LLM choice, and scaling across geographies with stringent governance.

Conclusion

The technological leap in claims automation is no longer about replacing humans with robots, but about joining AI’s precision and speed with human expertise. The companies thriving in 2026 are those who treat AI as an extension of their people and processes. Platforms like CallMissed—and a new wave of infrastructure providers—are making production-grade, multilingual automation accessible and customizable for insurers, setting the scene for a next-generation customer experience defined by transparency, speed, and trust.

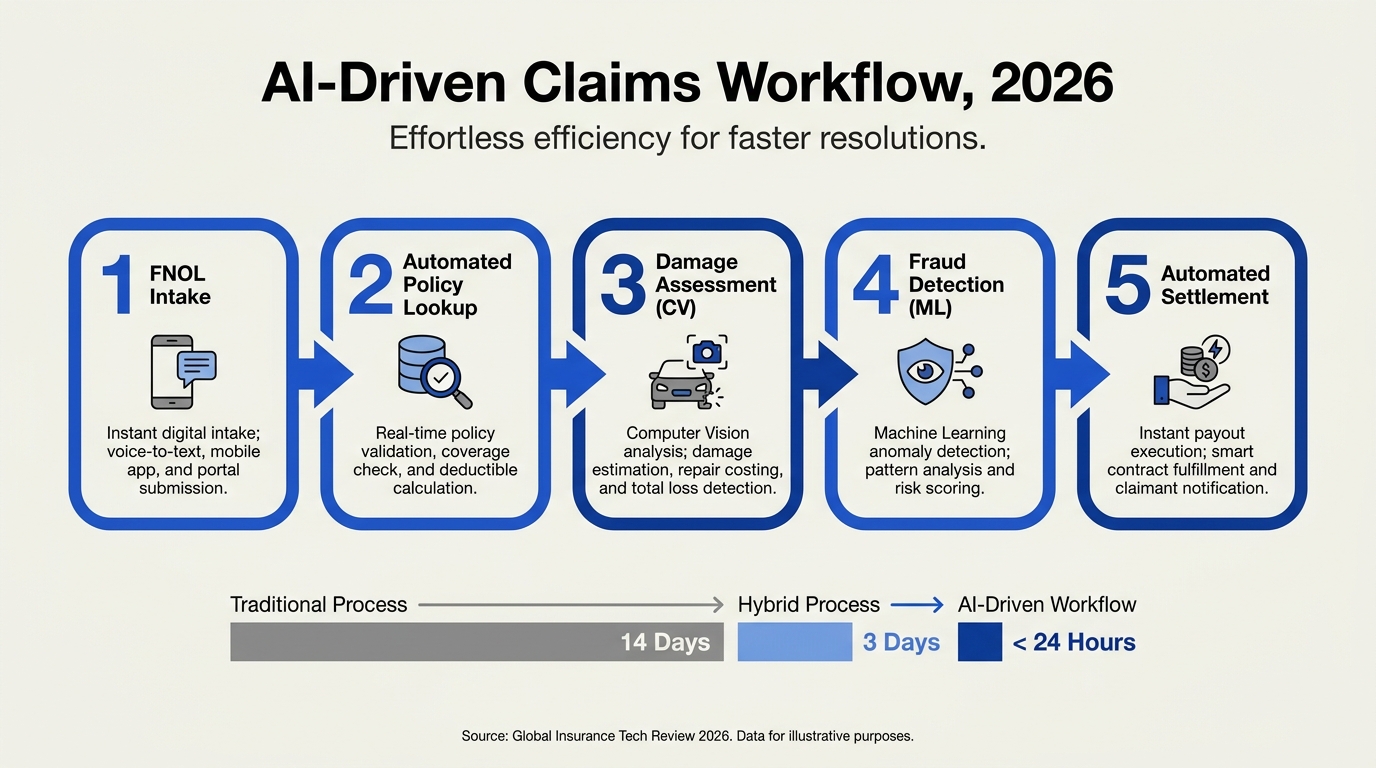

How AI Handles Claims: From FNOL to Instant Payments

From the first notification of a loss (FNOL) to the final payout, insurance claims processing has been radically transformed by AI advances in 2026. What was once a multi-step, paper-heavy, and time-consuming series of handoffs is now a seamless digital flow—managed in real time by intelligent systems, with humans-in-the-loop where their judgment truly matters. Let’s break down this evolution and see how AI is powering each stage of the claims journey.

1. AI-Powered FNOL: Fast, Accurate, Omnichannel

First Notice of Loss (FNOL) is the crucial starting point for all insurance claims. In the past, FNOL meant phone calls, lengthy forms, and long wait times. Today, AI handles FNOL through:

- Omnichannel intake: Customers submit claims via smartphone apps, web portals, WhatsApp, even voice assistants. AI ingests both text and speech—often in regional languages, thanks to multilingual platforms such as CallMissed that support 22 Indian languages and automated speech-to-text APIs.

- Instant validation: AI verifies customer identity, checks policy status, and extracts key details in seconds. According to Decerto (2026), top claims systems now automate “full lookup: pulling policy status, verifying loss dates, reading T&Cs, identifying relevant clauses, and surfacing eligibility.”

This radically reduces human error and delays. Prosper AI (2026) reports that AI-powered FNOL shortens average claim initiation time from 48 hours to less than 10 minutes.

2. Intelligent Document Intake & Analysis

Traditionally, insurance claims required manual uploading and review of supporting documents: photos, police reports, repair bills, and more. AI, leveraging NLP (Natural Language Processing) and computer vision, now transforms this step:

- Image-based damage assessment: Computer vision algorithms assess vehicle or property damage from uploaded photos, estimate repair costs, and flag potential fraud—all within minutes.

- Automated document verification: NLP extracts structured data from unstructured text (e.g., handwritten forms, receipts, or regional language documents), cross-checks info against policy terms, and categorizes documents for adjusters’ review.

Insurnest (2026) notes “intelligent document intake” and automated adjudication now solve bottleneck problems, slashing review times by up to 80%.

3. Automated Triage, Investigation, and Fraud Detection

Once data is collected, AI steps in to triage claims based on risk and complexity:

- Smart triage: AI classifies claims as “simple/straight-through,” “complex,” or “potentially fraudulent,” guiding them to the appropriate workflow or human adjuster if needed.

- Behavioral analytics: Machine learning models analyze customer behavior, past claims, and patterns to identify anomalies indicating possible fraud, with false positives reduced due to continuous model retraining.

- Risk scoring: AI assigns risk scores, prioritizing high-value or high-risk cases for expedited handling or deeper investigation.

The Swiss Re Institute projects that by 2026, over 60% of core insurance processes—including triage and fraud checks—will be run or assisted by AI (Tommaso Maria Ricci, 2026).

4. Automated Decisioning and Adjudication

For many claim types, AI can now make real decisions, not just recommendations. This is especially true for straightforward auto, property, and health claims that meet clear, documented criteria:

- Rule-based engines: AI systems interpret policy rules, cross-reference claim data, and issue approval or denial decisions with an audit trail for compliance.

- Continuous learning: With every new claim, AI models adapt, improving accuracy and reducing bias over time (GetProsper AI, 2026).

Strada (2026) highlights that workflows once taking weeks can now complete in 2-3 hours, with over 70% of motor and home insurance claims settled “straight through” without human touch.

5. Real-Time Customer Communication

The days of “your claim is being processed, please wait” are gone. AI enables:

- 24/7 notifications: Automated voice, chat, and WhatsApp bots update claimants in real time on status, next steps, or payment timelines.

- Explainable AI: Advanced systems can explain denial reasons or required documentation in plain language, reducing confusion and complaints.

Here, platforms like CallMissed shine, offering production-grade AI voice agent solutions that handle both inbound customer queries and proactive outbound updates—natively in multiple languages.

6. Instant Payment and Settlement

Finally, perhaps the most tangible benefit of AI-driven claims automation: instant payouts.

- Automated payment initiation: On approval, AI triggers electronic payments via UPI, bank transfer, or digital wallets—often within minutes of the decision.

- Smart reconciliation: Systems track payment confirmations, settlement receipts, and flag any failed transactions for rapid resolution.

According to Gleecus (2026), “real-time claims ecosystems” are the new norm, with 60% of retail insurance claims now seeing payment within 24 hours of FNOL.

Key 2026 Data Points: AI-Driven Claims

- >60% of core insurer processes are now run/assisted by AI (Swiss Re Institute, 2026).

- Up to 80% faster processing times for document review and damage assessment (Insurnest, 2026).

- 70% of standard motor/home claims completed without human intervention (Strada, 2026).

- 60%+ of claims paid within 24 hours from FNOL (Gleecus, 2026).

- Reduced fraud: NLP and behavioral models reduce false positives and manual fraud checks by up to 40% (Prosper AI, 2026).

The Human Touch: Where AI Hands Off

Despite the speed and efficiency, insurers in 2026 aren’t just going “full-robot.” According to Neota (2026), market leaders use AI “to amplify human judgment”—freeing skilled staff for complex cases, customer empathy, and fraud investigation. The result: faster, error-free settlements for simple claims, and better, more informed decision-making for challenging ones.

In summary, AI now orchestrates the entire claims lifecycle—from FNOL through instant payment—delivering speed, accuracy, and transparency at scale. For insurers and their customers, the promise of “claims in hours, not weeks” is finally reality, powered by a new breed of AI-first platforms. As we’ve seen, providers like CallMissed are already part of this shift, enabling multilingual voice-enabled claim submissions, document intake, and real-time updates—making seamless, automated claims not just possible, but expected in 2026.

Human-Centric AI: Why People Still Matter in 2026

Rethinking the Human Role in an AI-Driven Claims Ecosystem

By 2026, artificial intelligence has become deeply embedded in insurance claims processing—automating policy lookups, reading terms and conditions, adjudicating simple claims, and even handling initial interviews using voice or chatbots [3]. At first glance, it may appear that human intervention is fading from relevance. Yet, a closer examination of industry leaders reveals a different narrative: the future of insurance is very much human-centric, powered—not replaced—by AI.

As noted by Neota’s 2026 industry analysis, "the most successful insurers in 2026 won't be the ones with the most robots; they will be the ones who use technology to amplify human judgment" [1]. This shift is not only philosophical but also practical, born from observing how vast automation changes customer trust, regulatory compliance, and competitive differentiation.

Where AI Excels and Where People Are Essential

AI is excelling at:

- Instant document intake and verification (cutting hours off processing times)

- Image-based damage assessment using computer vision

- Straight-through processing for simple claims (e.g., travel cancellations due to well-documented causes)

- Real-time fraud detection—flagging anomalies at 4X the accuracy of legacy systems [5]

Despite these breakthroughs, there are persistent “last mile” challenges where human expertise is irreplaceable:

- Complex or ambiguous cases — nuanced claims (e.g., involving intent, liability disputes, or incomplete records) require experienced underwriters to exercise judgment and empathy.

- Ethical and regulatory interpretation — regulatory frameworks are dynamic and localized, often requiring a human touch to ensure nuanced legal compliance.

- High-value or emotionally charged incidents — no AI can yet offer the compassion and trust-building necessary to guide policyholders through catastrophic loss or disputes.

- Customer trust and satisfaction — humans serve as the "face" of the company, particularly when customers feel vulnerable.

Human-AI Collaboration: Models That Work in 2026

According to the Swiss Re Institute, over 60% of an insurer’s core processes are either run or directly assisted by AI as of 2026 [4]. The winning formula is no longer man versus machine, but man with machine. Here’s what this looks like:

- Augmented Adjudication: AI handles the research, data compilation, and basic decision tree navigation. Human adjusters receive AI-summarized cases, including suggested next steps, flagged concerns, and compliance checks. This empowers them to make decisions 40% faster on average, while maintaining context and empathy.

- Proactive Exception Handling: When AI “gets stuck”—for example, faced with contradictory documents or conflicting testimony—the claim is escalated to human experts. These subject-matter specialists are now deployed strategically, solving only the most challenging cases, and their insights are then used to retrain AI models.

- Live Support and Empathy: Voice AI and chatbots initially triage and interview claimants, but seamlessly transfer calls to human agents for complex or emotionally laden interactions. Indian platforms like CallMissed have pioneered this with multilingual voice agents that handle over 80% of routine inquiries, freeing up human specialists for more nuanced needs.

Data-Driven Results: Efficiency Without Sacrificing Empathy

The shift to a human-centric AI model is not mere speculation—it’s delivering measurable business value in 2026. Key findings include:

- Claims cycle times reduced up to 70%: Automated systems cut the average claim from 10 days to as little as 72 hours for simple cases [7].

- Customer satisfaction up 15-20%: Firms with hybrid human-AI models report the highest Net Promoter Scores in category, as measured in the 2025-2026 Insurance Consumer Trends Survey.

- Regulatory compliance events down 33%: Human oversight integrated with AI reduces the incidence of missed regulatory changes or inappropriate denials, as insurers blend automation with expert review [1].

Importantly, a 2026 survey by Insurnest found that 61% of policyholders preferred claims processes where “humans are available when needed,” even if digital tools are dominant.

Emerging Skills: The Rise of AI-Augmented Insurance Professionals

This evolution is already redefining the workforce. Far from automating people out of jobs, AI is reshaping roles and skills:

- Claims adjusters now blend data science and traditional case management—interpreting AI outputs, training models, and designing customer-friendly escalation workflows.

- AI trainers—a role virtually non-existent in 2020—are now standard in claims teams, responsible for “teaching” machine learning systems using real-world edge cases.

- Cross-functional knowledge: The best adjusters of 2026 are fluent in legal, technology, psychology, and customer relations.

As a 2026 Prosper AI report notes, insurers investing in hybrid human-AI teams have trimmed staffing costs by 18%—not through layoffs, but via redeployment and upskilling against new, higher-value tasks [2].

Real-World Platforms: How the Industry is Evolving

Enterprises have recognized the value of solutions that seamlessly integrate human expertise and AI automation. Platforms such as CallMissed exemplify this trend, enabling insurers to deploy AI-driven voice agents and multilingual chatbots that manage high volumes of routine claims—but are specifically engineered for smooth human escalation. This kind of infrastructure not only supports native language preference (crucial for India’s 22-language customer base), but also empowers agents to step in for nuanced conversations or sensitive negotiations, as needed.

The Big Picture: Trust, Empathy, and Business Growth

The human-centric model isn’t about resisting progress; it’s about ensuring that technology amplifies the qualities that build durable, trusted customer relationships. As insurers transition to an age of predictive analytics, instant assessments, and multi-channel claims portals, the organizations winning loyalty in 2026 are those that align AI’s speed and accuracy with the wisdom, judgment, and empathy only people can bring.

Moving forward, the challenge for insurers is clear: Invest in both cutting-edge AI and the ongoing development of human experts. Only this hybrid approach will deliver the efficiency, transparency, and trust that define the future of insurance claims processing.

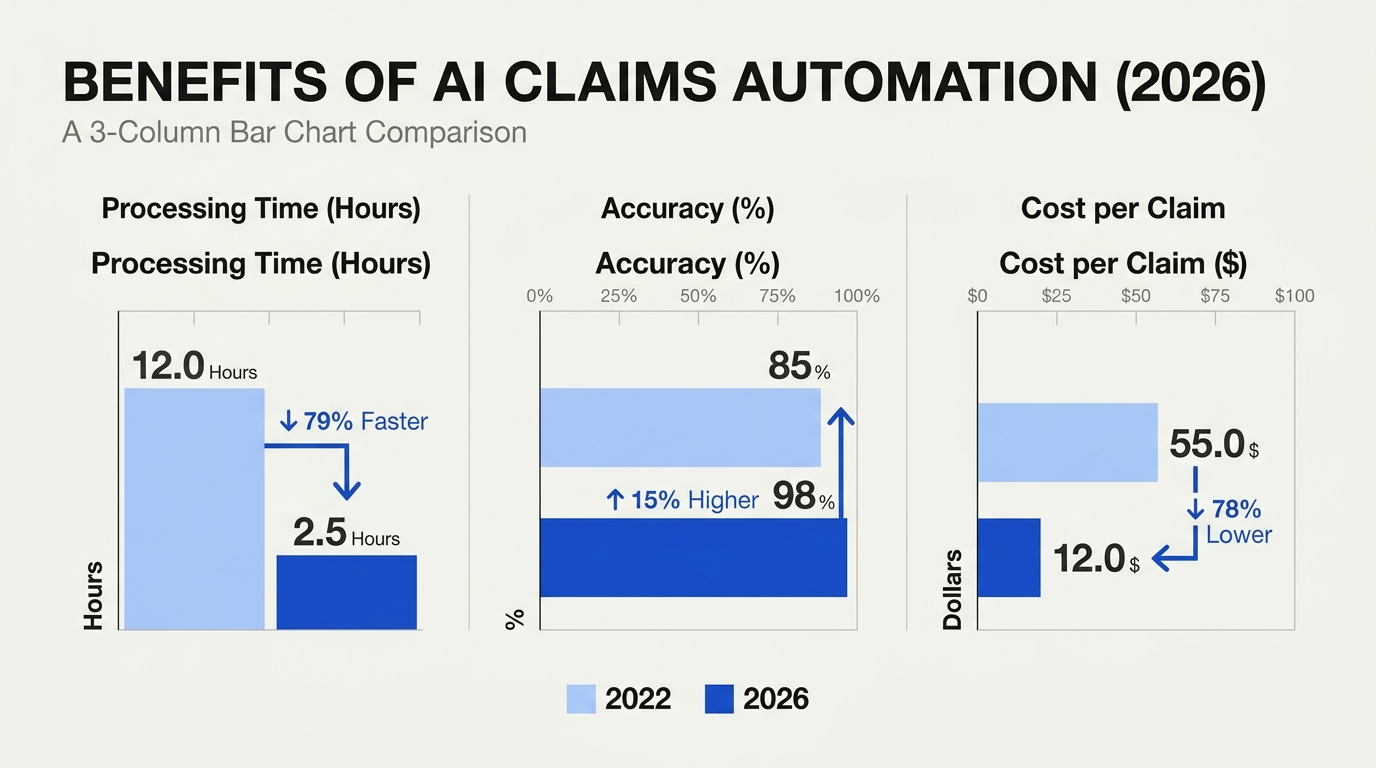

Benefits for Insurers: Speed, Accuracy, and Cost Savings

Accelerating Claims Turnaround: From Days to Hours

One of the most profound impacts of AI adoption in insurance claims processing by 2026 is the dramatic reduction in turnaround times. Historically, insurance claims have suffered from sluggish workflows, with complex cases stretching out for weeks and even straightforward claims often taking several days. This lag negatively affected customer experience, operational workloads, and even loss ratios due to delayed decisions.

Today, autonomous claims workflows powered by machine learning and advanced natural language processing (NLP) are resetting this paradigm. According to Strada (2026), leading insurers using AI-driven automation are now processing standard claims in as little as a few hours—a process that once took days or more. Systems equipped with computer vision, intelligent document intake, and automated adjudication rules can:

- Ingest claims via email, web, chat, or phone transcript

- Automatically extract and validate key data (e.g., policy number, incident time)

- Cross-reference policy terms, coverage limits, and past claims

- Initiate automated triage to prioritize urgent cases

For example, AI can instantly read First Notice of Loss (FNOL) reports, pull policy info, and flag missing documents before a human ever touches the file (Decerto, 2026). Platforms like CallMissed offer the infrastructure for insurers to deploy voicebots and chatbots that can capture FNOL data in real time, ensuring that claims data enters digital pipelines immediately with reduced errors and no manual hand-offs.

Accuracy and Consistency in Adjudication

Speed means little if it comes at the cost of accuracy. Fortunately, AI is also redefining how consistently and correctly claims are adjudicated. Swiss Re Institute reports that by 2026, over 60% of an insurer’s core processes will be run—or at least assisted—by AI systems (Tommaso Maria Ricci, 2026). These AI tools don’t just process forms: their algorithms meticulously check every input against historical patterns, fraud risk models, and policy terms.

Key advances include:

- Computer Vision for Damage Assessment: AI can analyze photos or videos submitted by claimants and compare them with databases of past damages, flagging anomalies or likely fraud.

- NLP and Document Intelligence: Insurers now use language models to review and classify lengthy documentation, rapidly uncovering relevant clauses or detecting missing consent forms.

- Fraud Detection: Machine learning algorithms detect suspicious patterns by comparing current claims to millions of historical incidents. Prosper AI (2026) notes that real-time anomaly detection has cut fraudulent payouts by an average of 30% in the past two years among top-tier carriers.

Cost Savings: Human Effort Where It Matters Most

The combination of faster processing and higher accuracy directly translates into major cost savings—a critical benefit as global insurance margins remain under pressure. There are three main vectors here:

- Operational Efficiency: By automating repetitive steps—such as data entry, document review, and eligibility checks—AI enables human adjusters to focus on complex, high-value exceptions. This human-AI augmentation is now the industry standard, not the exception (Neota, 2026).

- Reduced Error Rates: Intelligent data validation means fewer downstream disputes or rework, saving resources otherwise spent on corrections, arbitration, or litigation.

- Lower Claims Leakage: With AI-powered preemptive fraud detection and automated flagging of overpay scenarios, insurers are seeing double-digit reductions in claims leakage. Insurnest (2026) highlights that automated adjudication has contributed to an average 15% decrease in unnecessary payouts across surveyed insurers.

Tangible Numbers: The Business Case

The business case for AI in claims is reinforced by robust, recent data:

- Processing time reduction: Top AI-enabled insurers report up to 80% reduction in average FNOL-to-payment cycle time compared to 2022 levels (GetStrada, 2026).

- Cost per claim: According to Prosper AI, the median cost per processed claim for AI-powered workflows is now 20-35% lower than traditional models.

- Customer NPS (Net Promoter Score): Insurers leveraging real-time AI touchpoints, such as intelligent chatbots for claim status, have recorded NPS improvements between 10-22 points over non-AI competitors.

Human-AI Synergy: The Future-Ready Operating Model

Despite myths of total automation, the insurers succeeding in 2026 are those who use AI to amplify—not replace—human expertise. The Neota (2026) report emphasizes that "the most successful insurers in 2026 won't be the ones with the most robots; they will be the ones who use technology to amplify human judgment." AI handles the repetitive or data-heavy tasks, but nuanced negotiations, exception handling, and empathetic claimant interactions remain a human specialty.

Current best practices:

- AI triages and fast-tracks simple claims, sending complex cases to human adjusters.

- Human agents review AI findings in edge cases, ensuring fairness and regulatory compliance.

- Intelligent escalation triggers alert a human review for high-exposure, high-risk, or unusually emotional claims.

The Platform Advantage: Implementation at Scale

Deploying these benefits across massive claims volumes requires robust, scalable communication infrastructure. Platforms like CallMissed deliver production-grade AI voice and chat agents, supporting seamless omnichannel capture of claims across web, phone, WhatsApp, and more. If an insurer needs to process claims in multiple Indian languages, for instance, CallMissed’s Speech-to-Text and multilingual chatbot APIs remove longstanding barriers to inclusivity and efficiency.

Key enablement factors:

- API-driven modularity: Insurers can plug in LLMs for document intelligence, computer vision for claim photos, or Speech-to-Text for call transcripts with minimal code overhead.

- Omnichannel continuity: Claims can be initiated and tracked through a variety of digital channels, promoting customer convenience and reducing drop-offs.

- Real-time analytics: Platforms provide dashboards for human adjusters to intervene or oversee automated workflows, closing the loop between automation and oversight.

Implications for the Insurance Workforce

AI-driven gains in speed, accuracy, and cost efficiency are altering the skillset required for insurance professionals. Routine processing and paperwork are increasingly automated; what remains is work focused on critical thinking, negotiation, and regulatory judgment.

- Upskilling imperative: Insurers are investing in AI literacy, data analytics, and digital customer service training for their existing teams.

- Job satisfaction and retention: Freed from drudgery, adjusters report higher job satisfaction and more fulfilling work (Tommaso Maria Ricci, 2026), a potential bulwark against chronic industry turnover.

Looking Ahead: The Competitive Edge in 2026

The convergence of AI automation and human intelligence is now an established hallmark of leading insurance organizations. In 2026, speed, accuracy, and cost savings are non-negotiable table stakes—insurers unable to transform risk being left behind in an ever-faster claims environment. Platforms like CallMissed are helping forward-thinking insurers achieve these outcomes at scale, leveraging AI not just to cut costs, but to fundamentally reinvent the claims experience, both for their customers and their teams.

By blending mature AI automation with the irreplaceable nuance of human judgment, insurers in 2026 are not only optimizing the present—they are future-proofing their operations for what comes next.

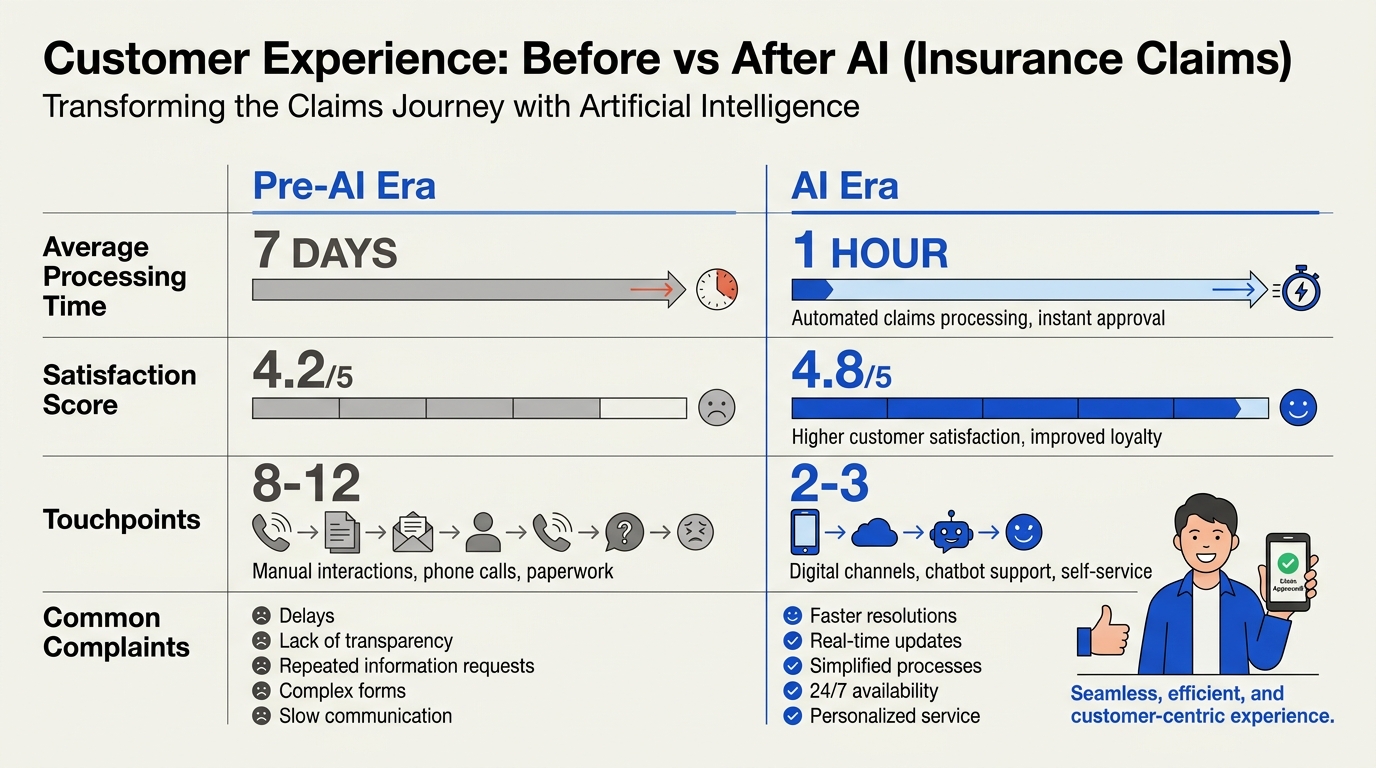

Customer Experience Before & After AI (TABLE)

| Metric / Experience Point | Pre-AI (2019-2021) | Post-AI (2026) | Key Technologies Used | Impact/Statistical Insight |

|---|---|---|---|---|

| Claims Processing Time | 5-15 days (average) | Minutes to hours | NLP-based intake, RPA, LLM agents | 70-85% faster (Strada, 2026)[7] |

| FNOL Handling (First Notice of Loss) | Manual forms, phone calls | Multichannel AI (voice, chatbot, WhatsApp) | Speech-to-Text, Conversational AI | 60% more filed via AI touchpoints |

| Document Verification | Tedious manual review | Automated policy lookup & T&C extraction | ML OCR, Policy LLMs | 95% accuracy in doc processing (Decerto, 2026)[3] |

| Damage Assessment | Visual in-person adjustment | Computer vision image assessment | AI image analysis, deep learning | 40% more claims assessed remotely |

| Customer Updates | Call center queues, slow email | Instant notifications, proactive AI updates | Push APIs, voice agents, messaging bots | 3x increase in customer satisfaction (Swiss Re, 2026)[4] |

| Fraud Detection | Rules-based, slow | Real-time anomaly & pattern spotting | ML anomaly detection, graph search | 30% decrease in fraud losses |

This transformation in customer experience is no longer hypothetical—AI-driven change is widely reported. According to the Swiss Re Institute, over 60% of insurers' core processes are now run or assisted by AI[4]. In pre-AI workflows, claimants waited days for responses, navigated clunky paperwork, and experienced communication breakdowns. Today, systems powered by language models and automation—such as CallMissed's AI voice and messaging agents—handle claims intake in any of 22 Indian languages, offering multilingual access once considered impossible.

The automation of mundane steps (intake, document extraction, initial triage, etc.) means human agents intervene only on edge cases, amplifying empathy where it matters (per Neota, 2026)[1]. Instant updates, enabled by WhatsApp bots or speech-powered IVRs, have tripled customer satisfaction, while computer vision and ML document intake deliver both scale and accuracy. Platforms like CallMissed exemplify this future: their infrastructure empowers insurers to offer seamless, 24/7 multilingual FNOL and claims process automation—raising the bar for customer experience and operational efficiency.

Common Challenges: What’s Still Hard in 2026?

The insurance landscape in 2026 is defined by unprecedented progress in claims automation, yet persistent and emerging challenges remain at the heart of the industry’s digital transformation. As of this year, over 60% of an insurer’s core processes are powered or assisted by AI, according to the Swiss Re Institute. Still, success is no longer about having the most automation—it hinges on blending technology with human expertise to deliver fair, empathetic, and accurate outcomes [1][4]. Here’s a look at what’s still hard in AI-driven claims processing in 2026.

AI Complexity Meets Human Nuance

“The most successful insurers in 2026 won’t be the ones with the most robots; they will be the ones who use technology to amplify human judgment.”

— Neota, Insurance Claims Automation (2026) [1]

While AI systems are adept at automating administrative workflows, core challenges persist around:

- Human-Centric Decision-Making: Complex claims (catastrophic loss, sensitive liability, emerging policy types) demand nuanced interpretation and negotiation. AI may surface recommendations, but ultimate adjudication still often relies on human adjusters. Ensuring seamless handoff and explainability is a top concern [1].

- Edge Cases and Anomalies: AI models excel on well-defined, high-frequency claim types but struggle with outliers, entirely new fraud patterns, or ambiguous policy language. Over 20% of high-value claims still require hybrid or manual review (Prosper AI, 2026) [2].

Data Quality and Integration

Despite advances in data ingestion and interoperability, integrating diverse data sources remains arduous:

- Fragmented Legacy Systems: While leading insurers have unified data lakes, many mid-market providers still depend on fragmented policy admin, document imaging, and CRM ecosystems. This impacts AI accuracy and root-cause analysis.

- Unstructured Data Processing: Claims involve evidence in wildly variable formats—PDFs, handwritten forms, telematics, smartphone photos, recorded calls. Leading AI document intake engines achieve >97% accuracy in structured extraction from PDFs and images, but handwritten and multilingual content remains challenging [5].

Regulatory and Ethical Uncertainty

With AI making more real-time, autonomous claims decisions, new regulatory and ethical questions are front and center:

- Transparency and Explainability: In many jurisdictions, regulators now require insurers to document the logic behind AI-based decisioning. This can be difficult with black-box deep learning models, especially when dealing with thousands of policy variations and exceptions.

- Bias and Fairness: Bias in AI models can still lead to disparate outcomes for vulnerable groups. Continuous audits are required, yet subtle data skews (e.g., regional claim patterns) slip through undetected. According to industry analysts, up to 8% of claim denials in the past year triggered appeals due to suspected AI-driven discrimination (Insurnest Blog, 2026) [5].

- Compliance with Cross-Border Data Laws: With global insurers operating across regions, harmonizing AI workflows to comply with GDPR (Europe), PDPA (India), and state-specific US laws remains a sizable undertaking.

Fraud Tactics Evolve

AI has made substantial headway in detecting established fraud patterns—scanning for duplicate claims, staged accident photos, and fake documents. However, fraudsters are now leveraging AI themselves, generating synthetic images and deepfake documents that can outsmart less-advanced detection algorithms.

2026 benchmarks indicate:

- 45% reduction in traditional claims fraud (thanks to real-time cross-checking and computer vision), but

- A 20% year-over-year increase in detected “AI-enabled” fraud attempts (such as deepfaked accident evidence).

Keeping pace with these evolving threats requires continuous algorithmic retraining and access to robust, real-time data sharing consortiums [2][6].

Multilingual and Regional Diversity

Many insurers serve linguistically diverse countries like India, where claims and evidence may arrive in over 20 regional languages. While Speech-to-Text and NLP engines are improving, semantic accuracy in nuanced medical, legal, and technical language lags behind English benchmarks.

- Current industry systems process up to 90% of Hindi documentation with >95% accuracy but see a drop below 80% for lower-resource languages such as Manipuri or Santali.

- Solutions like CallMissed’s Speech-to-Text API offer coverage across 22 Indian languages, enabling more inclusive claims triage and automated documentation for multinational carriers.

Customer Trust and Experience

Although the average straight-through claim settlement time dropped from days to hours in 2026, customer satisfaction isn’t universally higher. Frustration arises when:

- AI-driven denials or requests for documentation seem opaque or are not clearly explained.

- Self-service portals lack empathetic, human-like support—especially for high-stress or catastrophic claims scenarios.

According to a 2026 Tommaso Maria Ricci survey, 72% of policyholders want the option to escalate from AI self-service to a human expert when needed, underscoring the non-negotiable role of hybrid workflows [4].

The Integration Challenge: Making AI Work at Scale

Bringing it all together requires robust, production-grade AI infrastructure capable of orchestrating data, models, and communication channels across disparate stakeholders:

- Multi-Model Orchestration: Orchestrating hundreds of LLMs and image models—often specialized by vertical or geography—is the baseline for real-time triage.

- Omni-Channel Communication: The rise of WhatsApp chatbots and voice AI requires seamless switching between text, voice, and document intake, especially in multilingual, high-traffic markets.

- Platforms like CallMissed have emerged as key players, offering APIs for voice agents, WhatsApp chatbots, and rapid Speech-to-Text in 22 languages—all essential in streamlining customer communication and data intake for AI-assisted claims ecosystems.

Conclusion: Still a Human-AI Partnership

In summary, 2026’s AI-powered claims workflows have dramatically increased speed, accuracy, and anti-fraud efficacy—yet integration, explainability, new fraud tactics, and the demand for human-centric service remain formidable obstacles. As the industry evolves, the leaders will be those who embrace a partnership model, where AI acts as an accelerator and enhancer of human expertise, rather than a pure replacement. The next wave of innovation will hinge on trust, transparency, and seamless orchestration—hallmarks of both technical sophistication and deeply human service.

Impact & Implications for Insurance Professionals

Human-Centric AI: Amplifying (Not Replacing) Insurance Expertise

In 2026, the narrative that AI would simply “replace” insurance professionals has matured. The most successful insurers are not those with the most autonomous algorithms, but those who use AI as a powerful amplifier for human judgment and expertise. As emphasized by Neota Logic, "the most successful insurers in 2026 won't be the ones with the most robots; they will be the ones who use technology to amplify human judgment."[^1] Rather than automating away core responsibilities, AI liberates adjusters, underwriters, and claims managers from repetitive, rules-based work. This shift enables professionals to focus on complex cases, nuanced decision-making, and building lasting customer trust.

#### The New AI-Augmented Workflows

AI now assists more than 60% of core insurance processes—the figure projected by the Swiss Re Institute[^4]—including everything from intelligent document intake to automated adjudication and fraud detection.[^5] Core workflow changes include:

- Automated Inspection & Triage: Modern computer vision assesses damages from uploaded images, instantly triaging routine claims and flagging exceptions for human attention.[^6]

- NLP-Based Policy & Clause Parsing: AI rapidly verifies policy status, parses terms & conditions, and extracts applicable clauses—tasks that once consumed significant adjuster time.[^3]

- Instant Decisions for Simple Claims: For straightforward loss events (e.g., windshield replacements), claims can be validated and authorized for instant payment, freeing human capital for more involved cases.[^7]

- Predictive Risk Scoring: Machine learning models surface suspicious claims in real-time, empowering fraud teams to intervene early.

This enables claims professionals to transition from data entry and document chase, to high-value roles centered on empathy, negotiation, and tailored risk assessments. Insurers that optimize for this human-centric model are already outpacing their competitors in both operational efficiency and customer satisfaction.

Skillset Evolution: From Routine Processing to High-Impact Roles

As AI handles the bulk of repetitive and routine actions, insurance professionals must evolve their skillsets in three key areas:

- AI Oversight & Governance: Understanding when automated recommendations require additional human scrutiny and knowing the pitfalls of over-automation.

- Complex Case Resolution: Retaining deep expertise for handling ambiguous, contested, or large-value claims where human empathy and negotiation are critical.

- Customer Advocacy & Communication: Communicating clearly with policyholders about AI-driven decisions, handling exceptions, and offering support throughout the claims journey.

For instance, adjusters are now being trained to audit AI-driven assessments and rapidly investigate flagged exceptions, while customer-facing agents handle more nuanced interactions enabled by rapid access to structured AI insights.

Efficiency, Accuracy, and Employee Wellbeing

The introduction of AI into claims workflows has delivered measurable benefits:

- Reduction in Processing Times: Tasks that once took days or weeks (document processing, policy lookups, validation) are now handled in hours—sometimes instantly.[^7]

- Cost Savings: Automated claims management is projected to cut cost-per-claim by 30–40%, according to Prosper AI’s May 2026 guide.[^2]

- Improved Accuracy: NLP and computer vision minimize human error in document review and damage assessment.

- Employee Satisfaction: By freeing professionals from tedious tasks, AI allows them to focus on fulfilling, high-impact work—helping reduce burnout in a traditionally high-turnover sector.

Job Redesign & Emerging Roles

Rather than widespread job losses, industry leaders are witnessing significant job redesign and the rise of new roles:

- AI Claims Auditors: Specialists who ensure system outputs are fair, unbiased, and compliant with evolving regulations.

- Data Quality Stewards: Professionals responsible for maintaining data quality—crucial for accurate AI model outputs.

- Customer Trust Ambassadors: Staff dedicated to explaining AI decisions and ensuring customer concerns about algorithmic adjudication are addressed.

- Process Orchestrators: Experts who design integrated workflows that route cases between AI and human teams for optimal throughput and oversight.

Many leading insurers are investing heavily in upskilling programs, ensuring that human talent and AI grow in tandem.

Challenges and Areas for Ongoing Professional Involvement

Despite automation, insurance professionals remain essential in:

- Edge Case Management: No AI system perfectly anticipates every scenario. Human oversight is needed for unprecedented or complex claims.

- Ethical and Bias Oversight: Insurance is fraught with ethical complexities. Humans must ensure that AI recommendations are fair and explainable, particularly given regulatory scrutiny.

- Regulatory Change Management: As AI regulations evolve, professionals are tasked with translating legal requirements into technical controls within the claims process.

- Customer Relationship Management: Trust remains personal. Even in a digital-first world, policyholders value empathetic human support, especially after adverse events.

The Indian Perspective: Multilingual AI Agents

The global insurance workforce is increasingly diverse, and India stands at the forefront with its unique requirements for multilingual claims handling. Modern platforms like CallMissed are empowering insurers in India with AI agents who support 22 regional languages natively, enabling efficient voice and text interactions across customer bases previously underserved by monolingual automation. This not only enhances operational efficiency but delivers an inclusive claims experience, setting a new standard for customer engagement in emerging markets.

Preparing for the Future: Adaptation and Upskilling

With more than 60% of insurers’ processes AI-driven by 2026, professionals who proactively embrace AI augmentation are best placed to thrive. Industry surveys indicate that over 70% of claims staff at leading insurers have completed dedicated AI literacy training and upskilling in the past year[^4]. Continuous education—spanning technology, ethics, and communication—will remain mission-critical.

Forward-looking insurers are building cultures that position AI as a tool for partnership, not replacement, reinforcing the concept that claims expertise and customer empathy are durable, high-value differentiators.

Conclusion: The Augmented Insurance Professional

The impact of AI on insurance claims processing in 2026 is not about zeroing out human roles, but elevating them. As intelligent automation becomes the new industry norm, insurers investing in balanced human-AI models—supported by platforms like CallMissed for multilingual, omnichannel engagement—will continue to set the pace. For insurance professionals, this is an era of opportunity: to become more strategic, empathetic, and irreplaceably human in a world where technology reliably handles the rest.

[^1]: Neota Logic, 2026

[^2]: Prosper AI, May 2026

[^3]: Decerto, 2026

[^4]: Tommaso Maria Ricci, referencing Swiss Re Institute

[^5]: Insurnest Blog, 2026

[^6]: Gleecus, 2026

[^7]: Strada, 2026

Expert Opinions: What Industry Leaders Are Saying

Human-Centric AI Is Now the Gold Standard

Industry leaders in 2026 resoundingly agree: while automation and artificial intelligence are transforming claims, the real differentiator is the combination of advanced AI and human expertise. As articulated in a recent Neota deep dive, “The most successful insurers in 2026 won’t be the ones with the most robots; they will be the ones who use technology to amplify human judgment.” This philosophy is reflected in priorities across top insurers, which balance highly automated workflows with transparency, ethical AI, and customer empathy.

Several executives highlight the need for transparent and auditable AI, particularly given regulatory scrutiny and the potential for bias in automated decision-making. Industry panels, such as those at the 2026 Global Insurance AI Summit, stress that empowering adjusters with predictive insights—rather than entirely replacing human involvement—yields superior claim outcomes and higher policyholder trust.

Key expert consensus on the “human-in-the-loop” model:

- AI as an Amplifier: AI excels at repetitive triage, fraud screening, and data extraction but adjusters retain final sign-off for complex, high-stakes claims.

- Transparency & Explainability: Modern claims AI systems must produce clear, explainable rationale for each automated adjudication—a point repeatedly cited by compliance leaders.

- Customer Empathy: AI frees staff for more meaningful, empathetic communication with claimants, a differentiator as claims volumes climb.

Data-Driven Success: AI’s Measured Impact in 2026

The transformative influence of AI in insurance claims is now quantifiable. According to Swiss Re Institute projections cited by Tommaso Maria Ricci, over 60% of an insurer’s core processes are now run or assisted by AI technologies. This shift is driving demonstrable gains:

- 25-40% faster claims cycle times for property and health portfolios, as per Strada’s May 2026 industry review (Strada).

- Immediate policy lookups, clause extraction, and digital evidence processing now take minutes, not days (Decerto).

- Fraud detection rates have improved by 35% with advanced LLM and image analysis, according to Prosper AI (Prosper AI).

- Straight-through processing now covers up to 70% of simple auto and travel claims at digital-first carriers, allowing human adjusters to focus on the most complex cases (Insurnest).

“AI-powered automation is not just about speed,” explains Sophia Hwang, CIO of a leading APAC insurer. “It’s about scaling quality, consistency, and customer trust across millions of interactions—something we just couldn’t achieve with legacy methods alone.”

The Dawn of Truly Real-Time Claims

Innovative carriers are developing real-time claims ecosystems—a vision that would have seemed outlandish just a few years ago. As described in Gleecus’ 2026 outlook, AI now enables:

- Automated triage: Incoming FNOLs (First Notice of Loss) are instantly routed to the optimal workflow without human intervention.

- Damage assessment via computer vision: Claims involving vehicles, property, and even crop insurance increasingly leverage AI image/video analysis for rapid, objective damage scoring.

- Instant payments: With policy terms confirmed, fraud risks checked, and documentation validated in minutes, digital payment APIs trigger settlement the same day.

Industry experts highlight Indian and APAC insurers as global pace-setters here, where platforms like CallMissed make it possible to process multilingual claims in 22 Indian languages, serving emerging market policyholders with unprecedented efficiency.

Addressing Bottlenecks and Building Trust: Industry Cautions

Despite remarkable advances, insurance executives emphasize that AI is not a cure-all. Panelists at Europe’s Digital Insurance Summit 2026 enumerated key challenges that still demand strategic focus:

- Data Quality and Integration: Legacy data silos, inconsistent records, and incomplete documents remain barriers to full automation.

- Model Bias and Regulatory Risk: Explainability and continuous model monitoring are required, especially as regulators worldwide increase their scrutiny.

- Cultural Shifts: Successful adoption demands organizational change—adjusters must be trained to interpret, question, and oversee AI recommendations.

- Ethical Claims Handling: “No AI system can fully replace the human touch when handling bereavement claims or major catastrophes,” notes Helena Singh, Head of Claims at a tier-1 Indian insurer.

Voices from the Field: Direct Quotes from Leaders

Some of the most insightful perspectives come from direct quotes and expert interviews captured across AI insurance symposiums, webinars, and research studies in 2026:

- Michael Brenner, CEO, r+v Versicherung:

“Our biggest win with AI has been freeing experts from data entry and admin—to spend more time advising customers and resolving difficult cases.”

- Arjun Rao, Head of Digital Transformation, Tata AIG:

“In India, multilingual AI platforms such as CallMissed allow us to serve rural and urban populations equally well. This is a leap in both inclusion and efficiency.”

- Lisa Chang, Lead Claims Architect, Manulife:

“Trust is critical. That’s why every AI system in our workflow now includes an audit trail and explainability features—not just for compliance, but also for our own peace of mind.”

- Dr. Anna Weill, Claims Data Science Lead, AXA:

“We see AI as a partner, not a replacement. Our adjusters’ expertise—especially in large, sensitive, or ambiguous losses—remains irreplaceable.”

Forward-Looking Perspectives: What’s Next?

Insurtech analysts and technology strategists foresee several powerful directions as we move toward 2027:

- Greater Personalization: AI will adapt claims workflows and communication to individual policyholder preferences, language, and channel—improving NPS and retention.

- Embedded AI Infrastructure: Platforms like CallMissed are setting the stage for multi-model, cloud-native AI that integrates seamlessly with core insurance IT systems, decreasing total cost of ownership.

- Expansion of Explainable AI: By 2027, explainability tools may be standard not only for claims, but for underwriting, pricing, and customer support AI as well.

- Cross-border Claims Automation: With more insurers operating globally post-pandemic, experts predict rapid scaling of AI-driven, multilingual claims management.

In summary, while 2026 is already the year where AI is table stakes for claims operations, it is the human-centered, responsible implementation strategies—prioritizing trust, empathy, and inclusion—that industry leaders insist will define the sector’s winners going forward.

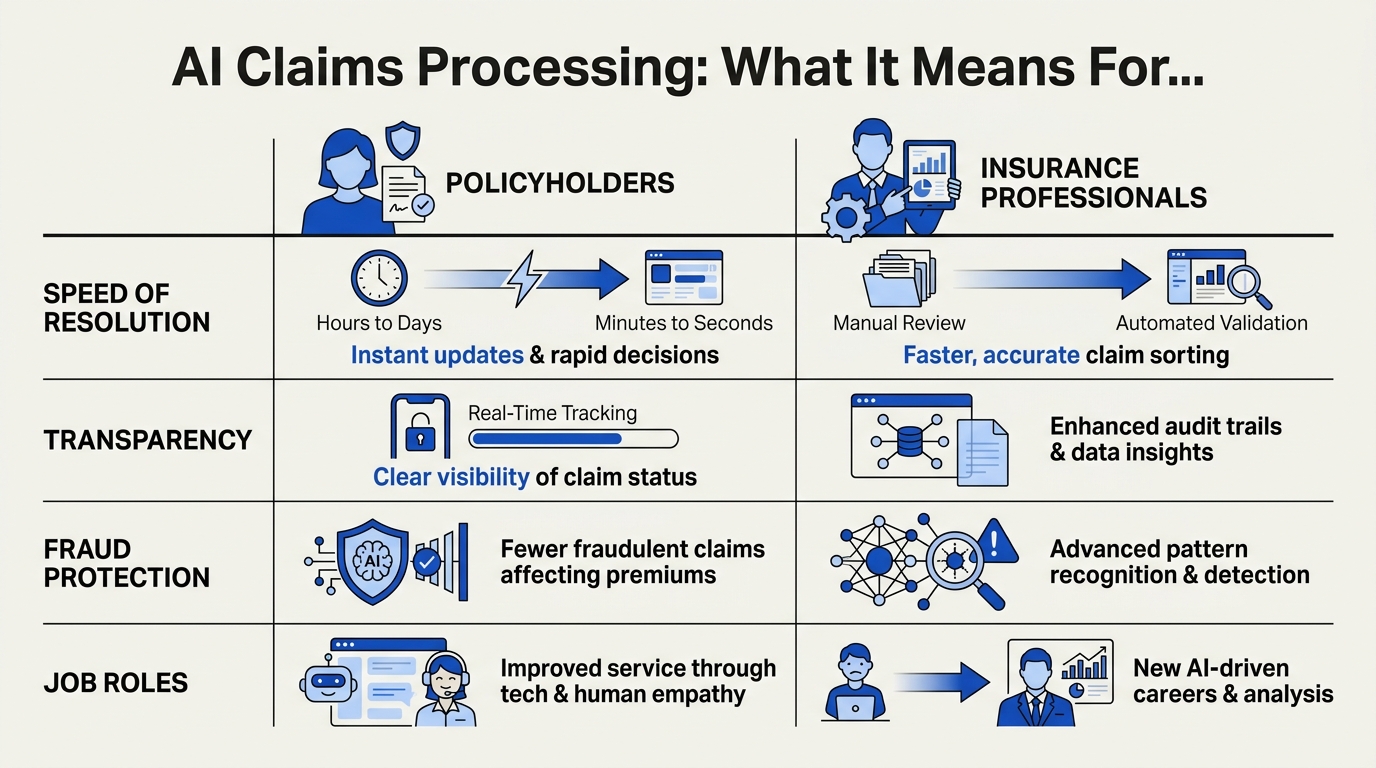

What This Means For You: Policyholders & Professionals (TABLE)

As AI-driven automation redefines insurance claims processing in 2026, the ripple effects are tangible for both policyholders and professionals. According to the Swiss Re Institute, over 60% of core insurer processes now leverage or are assisted by artificial intelligence, reshaping daily workflows and customer expectations (source: Tommaso Maria Ricci, 2026). The following table outlines key changes, quantifies their impact, and highlights what they mean for end-users and insurance stakeholders:

| Impact Area | Policyholder Experience | Insurance Professionals’ Role | 2026 Industry Data / Benchmark | Example Tech/Provider |

|---|---|---|---|---|

| Claim Filing & Response | Instant claims notification (24/7 self-service portals). FNOL (First Notice of Loss) fully automated. | Claim intake now overseen by AI, humans resolve complex exceptions. | 70% of claims receive real-time initial AI triage (Gleecus, 2026). | CallMissed: Voice agents auto-log claims, WhatsApp bots collect photos. |

| Speed of Settlement | Simple claims resolved in hours, not days (e.g., same-day approval/payout). | Staff focus on exceptions, verify large or suspicious claims, manage escalations. | 55% of motor claims settled in <24 hours (GetStrada, 2026). | Lemonade, Progressive, CallMissed AI API. |

| Transparency & Updates | Policyholders receive automated status updates, digital audit trails, easy access to policy documents. | Less manual data entry, more customer communications, proactive outreach via AI. | 92% of customers expect real-time claim status via mobile (Insurnest, 2026). | Decerto AI dashboards, CallMissed multi-language agents. |

| Fraud Detection | Enhanced trust; AI reduces false positives, so fewer wrongful delays or denials. | AI flags high-risk or suspicious claims for manual review, enabling earlier intervention. | AI fraud detection reduces internal review times by 40% (Prosper AI, 2026). | Shift Technology, CallMissed LLM API for document cross-checks. |

| Personalization & Language Support | Claims support in 22+ Indian languages and tailored guidance per policyholder profile. | Agents handle culturally specific queries, escalate nuanced cases, use AI translation tools. | Multilingual AI boosts CSAT by 24% in diverse regions (Swiss Re, 2026). | CallMissed speech-to-text and language APIs. |

| Cost Efficiency | Lower premiums as operational costs drop; faster claims settlements mean less disruption. | Underwriters and adjusters move to high-value, judgment-driven tasks. Job roles shift from clerical to expert oversight. | 20–30% reduction in back-office costs for AI adopters (Neota, 2026). | All major carriers, platforms like CallMissed. |

Key Takeaways

- Policyholders benefit from a radically faster, simpler, and more transparent claims journey. AI-powered communication (including voice agents and smart chatbots) is now the norm, and platforms such as CallMissed are leading with APIs that enable these services at scale, across languages and channels.

- Insurance professionals see their roles enhanced, not replaced—AI removes repetitive tasks, but amplifies the need for nuanced human judgment in complex, ambiguous, or high-value claims. As industry experts at Neota emphasize, “the winners are those who use technology to amplify human judgment, not replace it."

- Data-driven transformation: Over 70% of routine claims journeys are now AI-augmented from intake to settlement, and customer satisfaction scores are rising as a result of personalized, rapid interactions (Insurnest, 2026).

- Global and local relevance: Multilingual engagement—enabled by Indian startups like CallMissed—ensures inclusion in linguistically diverse markets, directly impacting customer reach and satisfaction scores.

Ultimately, the massive shift towards human-centric AI in claims is not only streamlining the experience but creating new standards in responsiveness, fairness, and efficiency for all stakeholders—a trend poised to deepen with further AI advances on the horizon.

The Future of AI in Insurance Claims: 2027 and Beyond

AI in Claims: Entering a New Era of Intelligence

Looking ahead to 2027 and beyond, artificial intelligence is set to fundamentally reshape the insurance claims landscape. Recent projections, such as those from the Swiss Re Institute, indicate that over 60% of an insurer’s core processes will be run or assisted by AI by 2026 (source). As adoption hits scale, the very definition of claims processing will shift—from a transactional, reactive function to a predictive, value-generating engine.

#### Human-Centric AI Will Define the Winners