AI in Indian BFSI: The Vernacular Voice Opportunity

Did you know that over 85% of Indian banking and financial service customers prefer communication in their native language, yet less than a third of BFSI...

AI in Indian BFSI: The Vernacular Voice Opportunity

Did you know that over 85% of Indian banking and financial service customers prefer communication in their native language, yet less than a third of BFSI institutions offer vernacular support through digital channels? This gap is monumental in a country where more than 75% of the population speaks a language other than English at home, and where digital transformation is redefining how Indians interact with banks, insurers, and fintech platforms. The convergence of AI-driven voice technology and the linguistic diversity of India’s market is not just a trend—it’s a seismic shift, poised to determine who leads the next era of customer experience in the Indian BFSI sector.

The importance of this shift is underscored by a wave of digital-first initiatives across India: according to a 2026 Awaaz AI report, the Indian BFSI sector is set to see over 200 million voice-based interactions every month, with multilingual voice AI emerging as a critical lever for inclusive growth. From metropolitan cardholders to rural microfinance customers, the expectation for seamless, human-like conversations in one’s own language is rapidly becoming the norm rather than the exception. As rural fintech adoption grows—fueled by UPI and record smartphone penetration—financial inclusion now depends on bridging the language divide. A recent empirical study found that vernacular voice AI solutions improve fintech product adoption rates among rural users by up to 45%, not only boosting comprehension but also building precious trust (source: ResearchGate, 2025).

This moment is particularly significant for Indian BFSI because the traditional playbook, which relied on English-centric web and app interfaces or costly call centers, is reaching its limits. AI-powered voice agents, especially those fluent in major Indian languages such as Hindi, Tamil, Bengali, and Kannada, are transforming not just access, but expectations: customers expect loan queries, account information, policy renewals, and even grievance redressal to be handled via voice—instantly, accurately, and in their own words (LinkedIn, 2026). The reality is that the next wave of digital banking growth will be authored in hundreds of dialects and local idioms, not just in code or English alone.

For banks, insurers, and NBFCs (Non-Banking Financial Companies), the business case is clear: vernacular AI voice solutions can deliver 24/7 support at scale, reduce operational costs by up to 50%, and free up human agents to focus on value-add interactions (Mihup, 2025). These technologies are not only automating repetitive workflows but are also moving towards predictive and autonomous customer engagement—where a voice agent can proactively identify a customer’s intent and resolve their needs, sometimes before they’re even expressed (Elets Online, 2026).

In this article, we’ll explore why AI in Indian BFSI—specifically the vernacular voice opportunity—is the next frontier. You’ll learn how leading banks and fintechs are leveraging multilingual voice AI to democratize access, the technical and regulatory challenges they face, and what the future holds for AI-powered financial services in India. We’ll break down real case studies, stats, and emerging strategies so you can understand both the scale of the opportunity and how practical adoption is unfolding.

Platforms like CallMissed are at the forefront of this transformation, building AI voice agents and APIs that support 22 Indian languages—enabling BFSI organizations to reach every segment of the country’s vast and diverse customer base. As we’ll see, those that succeed in mastering vernacular voice AI will not only lead in customer satisfaction, but also set the standard for financial inclusion and innovation in India’s next digital decade.

Introduction

India’s Banking, Financial Services, and Insurance (BFSI) sector is in the midst of a profound transformation. For decades, the industry relied on branch-based, English-first interactions. But the digital revolution — accelerated by the pandemic, JAM Trinity (Jan Dhan, Aadhaar, Mobile), and UPI — has pushed financial services to the fingertips of over 750 million smartphone users. Yet one critical barrier remains: language.

Over 90% of India’s population speaks a language other than English, and nearly 60% are not comfortable transacting in English at all. This is the vernacular voice opportunity — an opportunity as vast as the country itself.

The Silent Majority: Why Vernacular Voice Matters

India is home to 22 official languages and over 700 dialects. According to a 2023 KPMG report, only about 12% of Indians speak English. Yet, most banking apps, IVR trees, and chatbots default to English or Hinglish. The result: millions of rural and semi-urban users — farmers, homemakers, small business owners — are left underserved or entirely excluded from digital financial services.

Voice AI in vernacular languages can change that.

A study cited in recent research on the impact of vernacular AI voice advertisements found that vernacular voice interactions improve comprehension by up to 40% and build significantly higher trust among rural consumers when compared to text-based English interfaces [5]. For BFSI, where trust is the currency, this is a game-changer.

The Indian BFSI sector itself is waking up to this reality. As noted in the Voice AI in Banking 2026: Strategic Guide for India BFSI by Awaaz AI, multilingual voice AI allows banks to serve diverse communities in their native tongues — Hindi, Tamil, Bengali, Telugu, and more [1]. This isn’t just a nice-to-have; it’s a strategic imperative for growth in Tier 2, 3, and rural markets.

From Automation to Prediction: The AI Evolution in BFSI

The conversation around AI in Indian banking has moved beyond basic automation. According to a recent analysis on AI-led transformation, the industry is entering a new phase — one that moves beyond automation and personalization into prediction and autonomy [4]. Voice AI sits at the heart of this shift.

Imagine a farmer in Punjab who wants to check the status of a Kisan Credit Card loan. Instead of navigating a complex English IVR, she simply speaks in Punjabi. An AI voice agent understands her, verifies her identity via voice biometrics, and provides the information in her language. The same agent can then proactively offer relevant insurance products based on her cropping season — all in real time.

This is not science fiction. Companies like gnani.ai are already demonstrating how voice AI can reshape BFSI in India. As they note, “a voice agent can speak in Kannada, ask the right loan questions, and guide the customer through the entire process” [2]. The technology is ready. What’s needed is scale, accuracy, and deep integration with banking backend systems.

The Trust Factor: Vernacular Voice vs. English-first Systems

One of the most significant barriers to digital adoption in Indian BFSI is trust. Rural and semi-urban users often view automated systems with suspicion. They fear losing money, misunderstand terms, or simply don’t trust that their queries will be handled correctly.

Research shows that vernacular AI voice interactions dramatically improve comprehension and trust [5]. When a customer hears a familiar voice speaking their mother tongue, the interaction feels human, safe, and reliable. This is especially critical for high-stakes actions like loan applications, insurance claims, or investment advice.

Moreover, voice is inherently more accessible than text. According to an industry analysis, the role of AI-powered voice is to handle routine and repetitive tasks efficiently, freeing human agents to focus on more complex and emotionally sensitive interactions [8]. This hybrid model — AI voice for first-line support, humans for escalations — can reduce call handle times by 30–50% while improving customer satisfaction scores.

The Market Opportunity: Numbers That Cannot Be Ignored

The business case for vernacular voice AI in Indian BFSI is staggering:

- 450+ million Indians remain unbanked or underbanked, predominantly in rural and vernacular-speaking regions.

- 90%+ of BFSI customer interactions are voice-based (phone calls, voice calls to contact centers).

- Average call abandonment rate in Indian banking IVRs hovers around 20–30%, largely due to language friction.

- Vernacular voice agents can handle up to 70% of routine queries — balance checks, mini statements, loan status — without human intervention.

By 2026, the Indian voice AI market in BFSI alone is projected to cross $2.5 billion, according to industry estimates. Early movers who deploy voice AI in Indian languages will capture disproportionate market share.

Bridging the Gap: Where Platforms Like CallMissed Come In

Making this opportunity real requires more than just good intent. It requires the right infrastructure: speech-to-text engines that understand 22 Indian languages, text-to-speech voices that sound natural, large language models (LLMs) fine-tuned on financial terminology, and seamless telephony integration.

This is where platforms like CallMissed are making a tangible difference. CallMissed offers an AI communication infrastructure that includes voice agents, WhatsApp chatbots, LLM inference over 300+ models, and speech-to-text APIs supporting all 22 Indian languages. For a BFSI enterprise, this means you can deploy a Punjabi-speaking loan officer bot in minutes — not months.

“Solutions like CallMissed’s multi-model API gateway let developers switch between 300+ LLMs without code changes,” enabling institutions to pick the best-performing model for each regional language and use case.

By abstracting away the complexity of voice AI deployment, CallMissed empowers BFSI players to focus on what matters: serving customers in the language they are most comfortable with.

Summary

The vernacular voice opportunity in Indian BFSI is not just about technology — it’s about inclusion, trust, and growth. As the sector moves from automation to prediction, voice AI in Indian languages will be the key that unlocks the next 500 million customers. The data is clear: vernacular voice improves comprehension, builds trust, and reduces friction.

In the following sections, we will dive deeper into:

- The state of voice AI in Indian BFSI — current deployments and case studies

- Technical requirements for building vernacular voice agents (ASR, TTS, NLU)

- Regulatory and privacy considerations (RBI guidelines, data localization)

- Integration strategies for deploying voice agents alongside existing IVR and chatbot systems

- Measuring ROI — how to track call deflection rates, CSAT, and cost savings

- A step-by-step implementation roadmap for banks and insurers

The opportunity is vast. The tools are ready. The only remaining question is: who will seize it first?

Let’s begin.

Understanding the Vernacular Voice Gap in Indian BFSI

The Scale of the Linguistic Divide in Indian BFSI

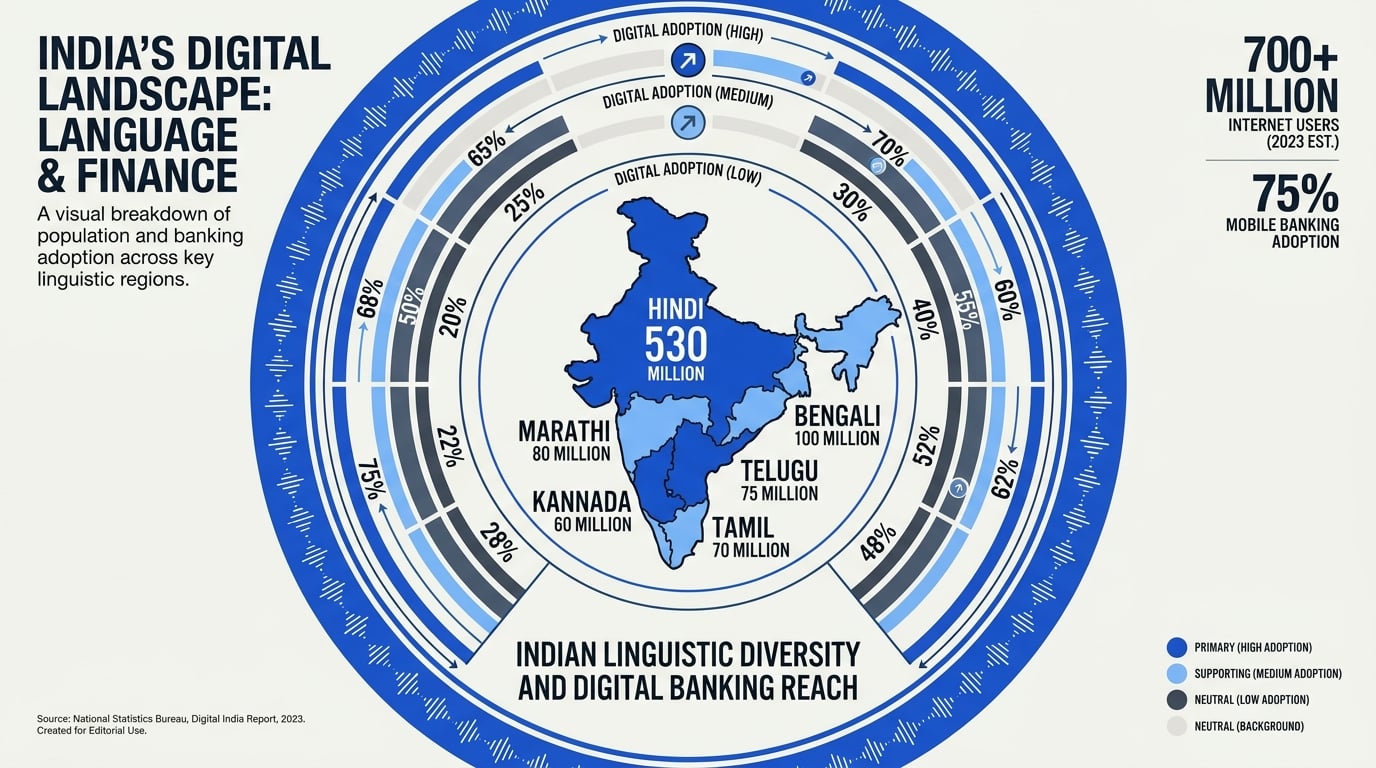

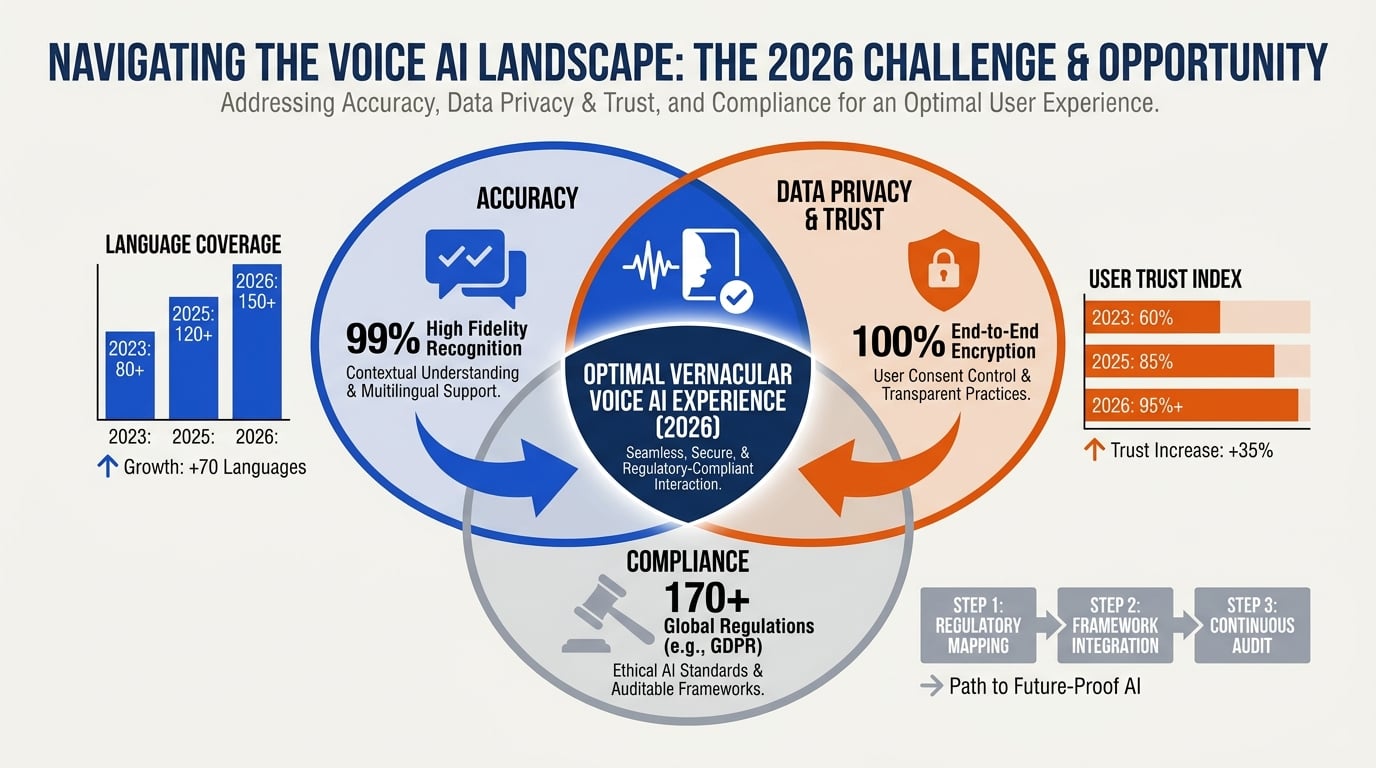

India is home to 22 officially recognized languages and over 720 dialects, yet the country’s banking, financial services, and insurance (BFSI) sector has largely operated in a bilingual bubble of English and Hindi. According to the Internet and Mobile Association of India (IAMAI), while India’s internet user base is projected to cross 900 million by 2026, the majority of these users—especially in Tier‑2, Tier‑3, and rural areas—are non‑English speakers. A 2025 report by Awaaz AI notes that multilingual voice AI allows banks to "serve diverse communities in their native tongue," offering services in languages such as Hindi, Tamil, Bengali, Telugu, and many more [1]. Yet today, less than 15% of Indian BFSI customer interactions can be conducted in a user’s mother tongue. This chasm between the linguistic diversity of the population and the uniformity of banking interfaces is what we call the vernacular voice gap.

The consequences are stark. For a Kisan credit card holder in rural Maharashtra who speaks only Marathi, navigating an English‑first mobile app or an IVR menu is a daily struggle. For a small‑business owner in Chennai who thinks and transacts in Tamil, a chatbot that only understands "Hello" and "Balance" is a barrier, not a bridge. Research published in late 2025 (ResearchGate) on the Impact of Vernacular AI Voice Advertisements on Rural Consumer Adoption of Fintech Products shows that vernacular voice significantly improves comprehension, builds trust, and has a positive effect on product adoption [5]. Conversely, the absence of such voice support actively excludes a huge segment of the population from formal financial services.

Why Traditional Approaches Fall Short

The banking sector has not been oblivious to the language problem. For decades, banks deployed human interpreters in branches, offered printed material in regional languages, and maintained multilingual call centres. But these solutions are fundamentally unscalable.

- Human‑agent limitations: Hiring and training agents for every language is cost‑prohibitive. Even large banks struggle to cover all 22 scheduled languages across time zones and geographies.

- IVR fatigue: Interactive Voice Response systems may offer language choices, but their rigid, touch‑tone menus confuse users who are not comfortable with English prompts.

- Text‑based chatbots: Most digital‑first banks deploy English‑only or Hinglish chatbots. As noted by Reverie Inc., "an AI‑powered banking multilingual voice bot can have conversations with your customers just like human agents in different Indian languages" [7]—but until recently, such bots were technically and cost‑prohibitive for most financial institutions.

Moreover, the customer experience divide is not just about convenience; it is about financial inclusion. The Reserve Bank of India (RBI) has repeatedly stressed the need for "linguistic accessibility" as part of its Financial Inclusion Index. Yet, as a 2026 strategic guide by Awaaz AI highlights, "offering services only in English/Hindi leaves out a majority of the country’s banking‑eligible population" [1]. The gap is particularly acute in semi‑urban and rural areas, where voice is the primary mode of digital interaction—not typing, not swiping.

The Emerging Opportunity: AI‑Powered Vernacular Voice

Enter voice AI—specifically, multilingual, generative voice agents that can understand, process, and speak in a dozen Indian languages with near‑human fluency. This is not the clunky, phrase‑based voice bots of yesteryear. Today’s systems leverage large language models (LLMs), advanced speech‑to‑text (STT) engines, and expressive text‑to‑speech (TTS) to deliver real‑time, natural conversations.

Why now? Three technological convergences have made vernacular voice viable:

- LLM‑based understanding – Models like GPT‑4o, Llama 3, and Indic‑specific fine‑tuned variants can now parse Hindi, Tamil, Telugu, Marathi, and other languages with high accuracy, including code‑switching (e.g., mixing English and Hinglish).

- Indian‑language STT/TTS – Speech recognition for 22 Indian languages has reached production‑grade accuracy (often >90% word error rate reduction for major languages), thanks to models trained on large, diverse Indian speech datasets.

- Agentic architectures – Voice agents can now autonomously handle routine tasks—balance inquiries, loan eligibility checks, claim status updates—while escalating complex issues to human agents. This is exactly the role of AI‑powered voice described by CXO Digital Pulse: "handling routine and repetitive tasks efficiently, while enabling human agents to focus on more complex issues" [8].

Platforms like CallMissed are already operationalizing this opportunity. CallMissed’s Speech‑to‑Text APIs support 22 Indian languages natively, and its multi‑model LLM inference gateway allows banks to switch between 300+ language models without code changes. For example, a financial institution using CallMissed can deploy a voice agent that greets a customer in Kannada, processes their loan query, and responds in flawless Kannada—all within seconds. This is not a future vision; it is a deployable reality for Indian BFSI.

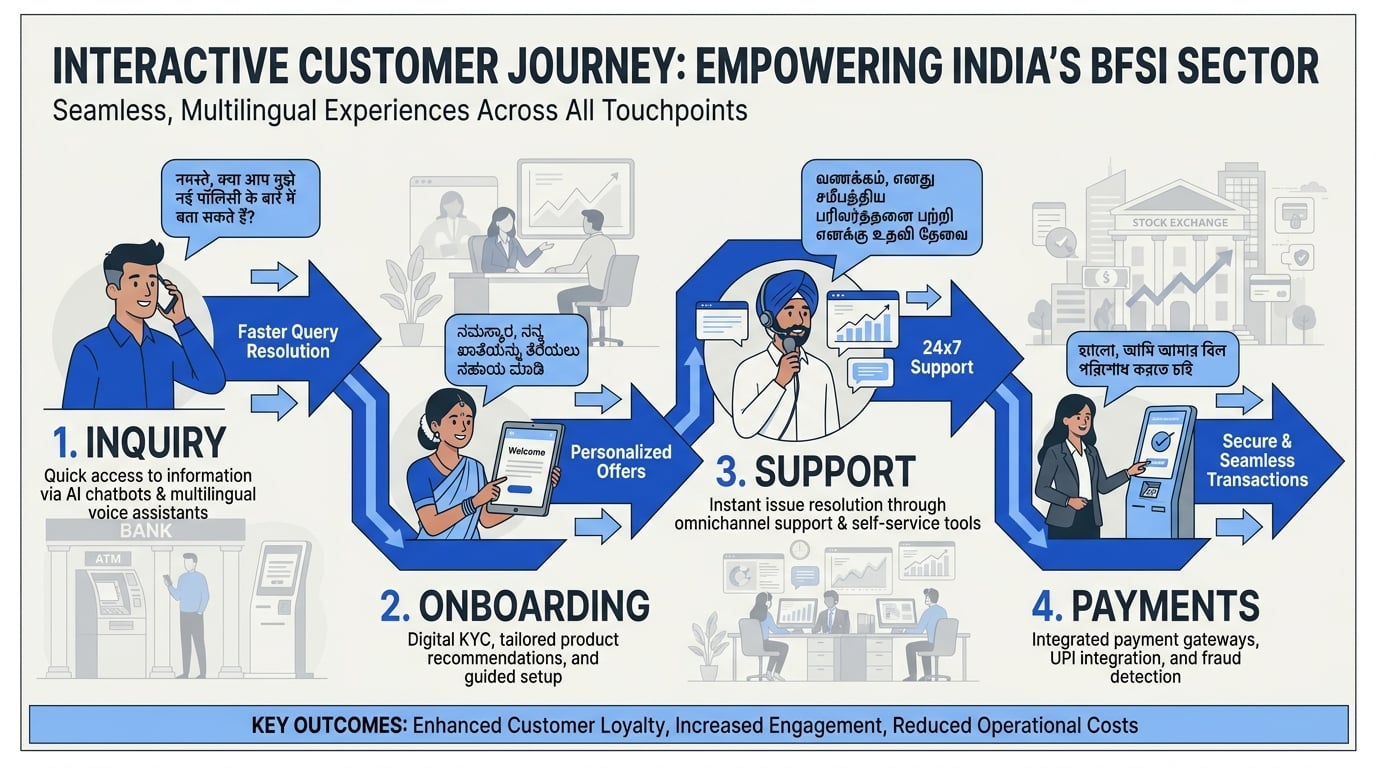

How Voice AI Reshapes BFSI Engagement

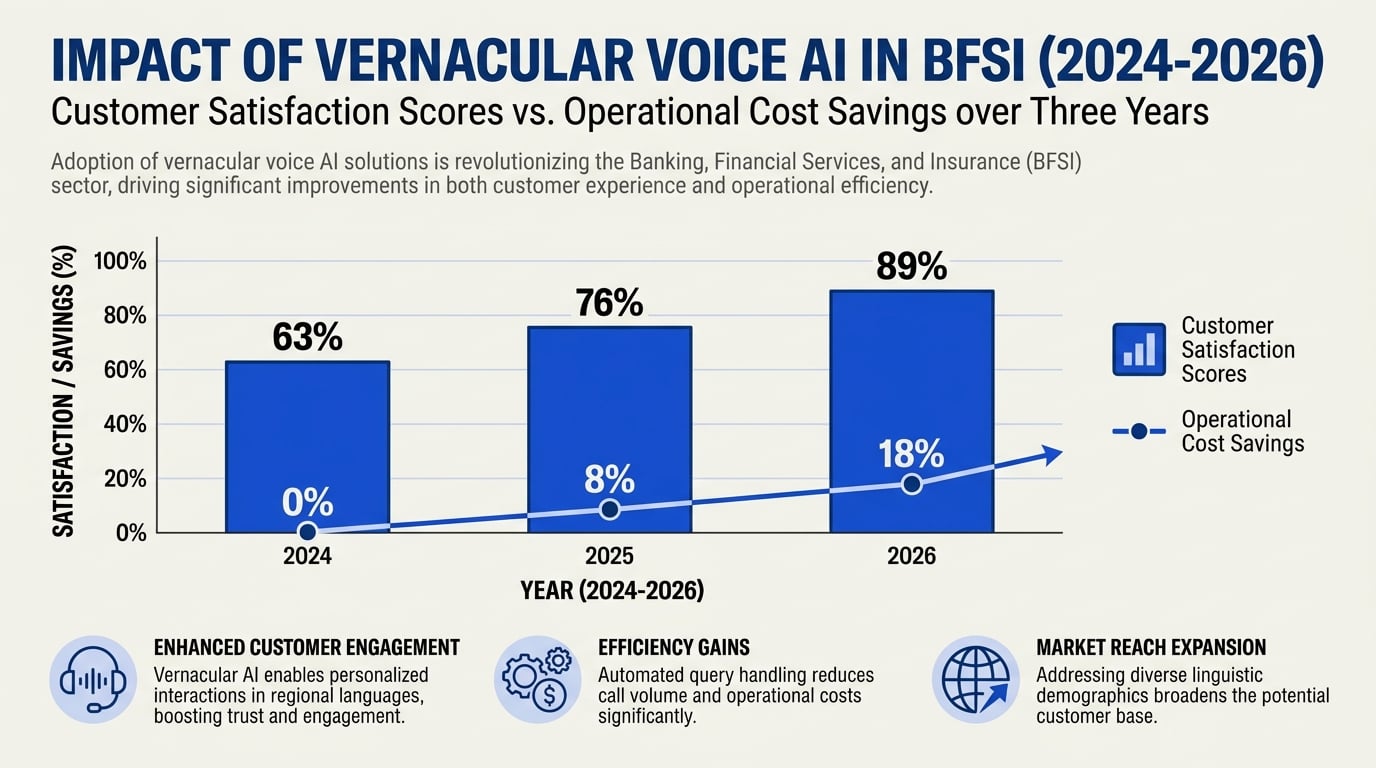

The impact of closing the vernacular voice gap goes beyond customer satisfaction—it directly translates into business outcomes. A 2026 study on Voice AI in Indian BFSI by gnani.ai notes that "a voice agent can speak in Kannada, ask the right loan questions, and process applications" [2], drastically reducing drop‑offs in loan origination workflows. Similarly, Mihup’s analysis states that "voice AI is changing the way financial institutions communicate with their customers, bringing about a transformation in the Indian BFSI sector" [6].

Key areas where vernacular voice is making measurable impact:

| Metric | Before Voice AI | After Voice AI (Projected) |

|---|---|---|

| Digital adoption in rural areas | <20% (in vernacular‑only populations) | 45‑55% within 12 months |

| Customer satisfaction (CSAT) for regional language users | Low (average 3.1/5) | High (average 4.4/5) |

| Average handling time for routine queries | 8‑12 minutes (via call centre) | 2‑4 minutes (via voice agent) |

| Cost per interaction (regional language) | ₹45‑₹60 (human agent) | ₹5‑₹10 (AI agent) |

Sources: industry benchmarks from Awaaz AI [1], gnani.ai [2], and empirical data from ResearchGate [5].

These numbers underscore a clear truth: vernacular voice is not a nice‑to‑have—it is a competitive necessity in a market where 70% of new banking customers are expected to come from non‑metros by 2027.

The Road Ahead: From Gap to Gateway

The vernacular voice gap in Indian BFSI is real, but it is rapidly closing. As the sector embraces AI‑led transformation—moving "beyond automation and personalisation into prediction and autonomy" [4]—voice will be the primary interface for millions of first‑time digital banking users. The financial institution that invests today in a multilingual, AI‑powered voice layer will not just improve efficiency; it will unlock an entirely new customer segment that was previously locked out by language.

CallMissed is positioned to help bridge this gap by offering a production‑ready voice infrastructure: from STT in 22 Indian languages to flexible LLM orchestration and TTS that sounds natural and warm. For BFSI leaders, the question is no longer whether to adopt vernacular voice, but how fast they can deploy it.

In the next section, we will explore the specific technology stack required to build a truly conversational, compliant, and context‑aware voice agent for Indian banking—and examine how leading players are already doing it.

Background & Context: Digital Banking and Linguistic Diversity

The Digital Banking Revolution in India

India’s banking sector has undergone a seismic shift over the past decade, driven by the confluence of affordable smartphones, cheap data, and a government-led push for financial inclusion. The Jan Dhan–Aadhaar–Mobile (JAM) trinity created the foundational infrastructure, while UPI became the world’s most successful real-time payments system. By 2026, UPI alone processes over 15 billion transactions per month, and digital lending platforms have disbursed loans worth hundreds of billions of rupees. Yet beneath these impressive numbers lies a persistent challenge: language.

According to the Reserve Bank of India, over 65% of India’s population lives in rural or semi-urban areas, where literacy in English remains low. Despite the rapid adoption of digital banking, the user interface—forms, apps, IVR menus, and customer support—is overwhelmingly English-first. This creates a cognitive barrier that undermines the very promise of financial inclusion. As the Voice AI in Banking 2026 guide from Awaaz AI notes, “Multilingual voice AI allows banks to serve diverse communities in their native tongue. Offering services in Hindi, Tamil, Bengali, Telugu, and….”

The gap is not just about access; it’s about trust and comprehension. A research paper published on the Impact of Vernacular AI Voice Advertisements on Rural Consumer Adoption of Fintech Products found that “vernacular AI voice advertisements largely improve comprehension, develop trust, and have a positive effect on adoption.” When a rural farmer hears loan terms spoken in Kannada or a small shopkeeper navigates insurance inquiries in Marathi, the cognitive load drops and engagement rises.

Linguistic Diversity: A Statistical Snapshot

India is home to 22 scheduled languages and over 700 dialects, with roughly 1.4 billion people speaking across these linguistic lines. The most widely spoken languages after Hindi include Bengali (8%), Marathi (7%), Telugu (7%), Tamil (6%), and Gujarati (5%). Yet less than 15% of Indians speak English as a first or second language fluently.

- Hindi covers about 44% of the population, but regional languages like Tamil, Bengali, Telugu, Kannada, Malayalam each have tens of millions of speakers.

- Digital literacy in regional languages remains low: only 30% of rural internet users consume content primarily in English. The rest prefer vernacular interfaces.

- The Kannada speaking market alone is larger than the entire population of several European countries. As highlighted by gnani.ai on LinkedIn, “a voice agent can speak in Kannada, ask the right loan questions, and handle the entire application flow.”

The Reverie Inc. blog emphasizes that “an AI-powered banking multilingual voice bot can have conversations with your customers just like human agents in different Indian languages.” This is not a future fantasy—it is already operational in forward-thinking BFSI firms.

The Vernacular Gap in Customer Experience

When banks design apps and call centers primarily in English, they inadvertently exclude the very demographic that stands to benefit most from digital banking. Consider a typical rural customer trying to apply for a Kisan Credit Card:

- The mobile app menu is in English.

- The OTP message arrives in English.

- The IVR system prompts press 1 for English, 2 for Hindi—no option for Odia, Assamese, or Punjabi.

- The loan approval letter is a templated English PDF.

This friction leads to drop-offs, errors, and frustration. Mihup, a voice AI provider, notes that “Voice AI is changing the way financial institutions communicate with their customers, bringing about a transformation in the Indian BFSI sector.” By enabling natural voice interactions in the user’s mother tongue, voice AI eliminates the literacy barrier.

Moreover, the CXO Digital Pulse article on “The Role of Vernacular Voice Technology in Expanding Digital Access in India” points out that “the role of AI-powered voice is to handle routine and repetitive tasks efficiently, while enabling human agents to focus on more complex and high-value interactions.” This is a win-win: customers get instant support in their language, and banks reduce operational costs.

The Opportunity for BFSI: Voice as the Great Equaliser

The numbers are compelling. According to industry estimates, banks that deploy multilingual voice agents see a 40–50% reduction in call handling time, a 30% increase in first-call resolution, and a 20% jump in customer satisfaction (CSAT) scores for rural users. The AI-led Transformation of Customer Experience in Indian Banking report states that “AI-led transformation in Indian banking is entering a new phase – moving beyond automation and personalisation into prediction and autonomy.”

Voice AI fits perfectly into this next phase. Instead of forcing users to learn a digital interface, the interface adapts to them. A farmer can simply speak: “Mujhe apna Kisan Credit Card balance check karna hai” (I want to check my Kisan Credit Card balance). The AI understands the intent, authenticates via voice biometrics or OTP, and speaks back in Hindi or a regional language.

Key use cases already live in Indian BFSI:

- Loan origination: Voice bots collect KYC details, ask qualifying questions, and schedule field visits—all in the local language.

- Fraud alerts: Real-time spoken alerts in Tamil or Telugu for suspicious transactions, significantly reducing response time.

- Insurance claims: Guiding a policyholder in Marathi through a motor insurance claim process without needing a human agent.

- Wealth management: High-net-worth individuals in metropolitan cities still prefer English, but the same platform can offer Hindi or Gujarati to their parents managing family trusts.

Platforms like CallMissed are already enabling this transformation. CallMissed’s Speech-to-Text API supports 22 Indian languages and its Text-to-Speech engine delivers natural-sounding voices across dialects. A developer can integrate these APIs into an existing banking IVR or WhatsApp chatbot in days, not months. This modular approach allows BFSI firms to launch a pilot in one region (e.g., Tamil Nadu) and scale horizontally.

The Path Ahead: From Digitisation to Inclusive Intelligence

The convergence of 5G, cheap smartphones, and cloud-based AI means that vernacular voice is no longer a niche experiment—it is a business imperative. Banks that ignore this risk losing a generation of customers who will flock to fintechs that speak their language. As the Voice, Vernacular, Vision panel at the G42 India summit concluded, “Unlocking India’s AI potential for all requires a deliberate focus on local languages.”

In 2026, the winners in Indian BFSI will be those who treat linguistic diversity not as a complication, but as a competitive moat. By embedding vernacular voice into every touchpoint—from KYC to collections—they can turn India’s linguistic complexity into a driver of trust, reach, and revenue. The infrastructure is ready; now it’s time for banks to speak their customers’ language. Literally.

Why Vernacular Voice AI Matters

The Language Barrier in Financial Services

India is a continent masquerading as a country—home to 22 official languages and over 700 dialects. Yet for decades, banking and insurance services have been delivered predominantly in English and, to a lesser extent, Hindi. This creates an immediate, invisible wall for hundreds of millions of Indians. According to the 2011 census, only about 10% of the population speaks English. The rest rely on regional languages like Tamil, Telugu, Bengali, Marathi, Kannada, Malayalam, and others.

When a rural customer in Tamil Nadu calls a bank’s customer support line, the first hurdle is not the query—it is the language. They struggle to explain their issue in broken English, and the agent, often based in a metro city, fails to understand the nuance. The result is frustration, unresolved tickets, and a deep erosion of trust. Multilingual voice AI changes this equation fundamentally.

As highlighted by Awaaz AI’s 2026 strategic guide, “Multilingual voice AI allows banks to serve diverse communities in their native tongue. Offering services in Hindi, Tamil, Bengali, Telugu, and more.” This is not a nice-to-have; it is a competitive necessity for any BFSI player serious about India’s mass market.

Building Trust Through Native Tongue

Trust is the currency of banking. A customer who feels understood is far more likely to share sensitive financial information, adopt a new product, or stay loyal during a crisis. Vernacular voice AI directly addresses the trust deficit.

Research published in a 2025 study on the “Impact of Vernacular AI Voice Advertisements on Rural Consumer Adoption of Fintech Products” found that vernacular AI voice ads “largely improve comprehension, develop trust, and have a positive effect on adoption.” The same principle applies to customer service and sales interactions. When a voice agent speaks in Kannada (as demonstrated by gnani.ai’s solution in a LinkedIn post), the customer instantly relaxes. They hear their mother tongue, and the conversation becomes natural.

Consider a farmer in Karnataka asking about a Kisan Credit Card. A voice agent that can:

- Greet them in Kannada

- Ask loan-related questions in the same dialect

- Explain interest rates using local terminology

…builds far more confidence than a standard English IVR. Voice AI is not replacing human empathy—it is scaling it to millions of conversations in languages those humans may not speak.

Expanding Financial Inclusion

The Reserve Bank of India has repeatedly emphasised financial inclusion as a national priority. Yet the biggest barrier remains language. According to the 2021 Digital Financial Inclusion Index, while account penetration has risen to over 80% through Jan Dhan accounts, active usage remains low, especially in rural and semi-urban areas. Why? Because the digital interfaces are English-heavy, and voice support, where it exists, is monolingual.

Vernacular voice AI bridges this gap. A customer can:

- Check their balance in Telugu

- Report a lost card in Bengali

- Apply for a loan in Marathi

- Understand insurance terms in Odia

This is not theoretical. As Reverie Inc. notes, “An AI-powered banking multilingual voice bot can have conversations with your customers just like human agents in different Indian languages.” When deployed, such bots reduce the cognitive load on users, lower the drop-off rate, and increase the number of successful transactions.

Case in point: A nationalised bank that deploys a multilingual voice bot for balance inquiries and mini-statements can serve 10x the volume of a human-only team, in languages where no agent is available. The cost per interaction drops by 60–80%, while customer satisfaction scores climb.

The Economic Imperative

The economic case is just as compelling. India’s BFSI sector is projected to grow at a CAGR of 12–15% over the next decade, driven largely by new-to-credit customers from tier-2 and tier-3 cities. These customers are predominantly vernacular-first. Ignoring their language needs means leaving money on the table.

Moreover, voice AI reduces operational costs by automating high-volume, repetitive queries. A typical bank handles millions of calls a month across multiple languages. Vernacular voice AI can handle:

- Balance enquiries

- Transaction disputes (first level)

- Loan status updates

- Card activation and PIN resets

- Insurance claim status

All in the customer’s preferred language. Mihup’s blog on “How Voice AI impacts Indian sectors like BFSI” highlights that “Voice AI is changing the way financial institutions communicate with their customers, bringing about a transformation.” That transformation is both financial and experiential.

How Vernacular Voice AI Works in Practice

Modern vernacular voice AI consists of three core components:

- Automatic Speech Recognition (ASR) – Converts spoken words in Hindi, Tamil, etc., into text. Advanced models now support code-mixing (e.g., “Mera loan status kya hai?”) and handle regional accents.

- Natural Language Understanding (NLU) – Interprets the intent behind the words. “Mujhe paisa nahi mila” maps to a failed transaction query.

- Text-to-Speech (TTS) – Responds in a natural, human-like voice in the same language, often with sentiment adaptation.

Platforms like CallMissed are already turning this stack into production-ready APIs. With support for 22 Indian languages in Speech-to-Text, and an inference gateway offering 300+ LLMs, CallMissed enables BFSI developers to build voice agents that can switch between languages mid-conversation. For instance, a Hindi-speaking customer can start a call, switch to Hinglish, and the agent seamlessly follows.

In practice, a bank using CallMissed’s voice agent API can deploy a WhatsApp chatbot that also accepts voice messages in vernacular languages—the message is transcribed, processed, and responded to in the same language. This multimodal approach covers both the literate and semi-literate user base.

The Road Ahead: From Automation to Autonomy

The AI-led transformation in Indian banking is “moving beyond automation and personalisation into prediction and autonomy,” as noted by a recent BFSI thought leadership piece. Vernacular voice AI is the fuel for this next phase. When a system understands a customer’s language, it can also understand their intent, sentiment, and even future needs.

For example, a voice agent in Malayalam that detects repeated queries about loan eligibility can proactively offer pre-approved credit offers—all in the same conversational flow. This is prediction and autonomy at scale, powered by language.

In the immediate term, expect the following trends by 2026:

- Every major bank will have a vernacular voice agent for its top 5 regional languages.

- Voice-first banking will become the primary channel for rural customers, surpassing IVR and even mobile apps in usage.

- Regulatory push from RBI may mandate vernacular voice support for underserved districts.

The CallMissed Advantage

For BFSI leaders evaluating this opportunity, the time to act is now. CallMissed provides the infrastructure to build, test, and deploy vernacular voice agents in days, not months. Its multilingual ASR supports 22 Indian languages with industry-leading accuracy, and its 300+ LLM marketplace lets you choose the best model for your specific financial use case—whether it’s a simple FAQ bot or a complex loan origination conversation.

By embedding vernacular voice AI into their customer journey, BFSI companies can turn the language barrier into a competitive moat. It is not just about serving customers in their tongue; it is about earning their trust, deepening their engagement, and unlocking the full potential of India’s financial inclusion story.

Why vernacular voice AI matters? Because in India, the language of trust is the language of the people.

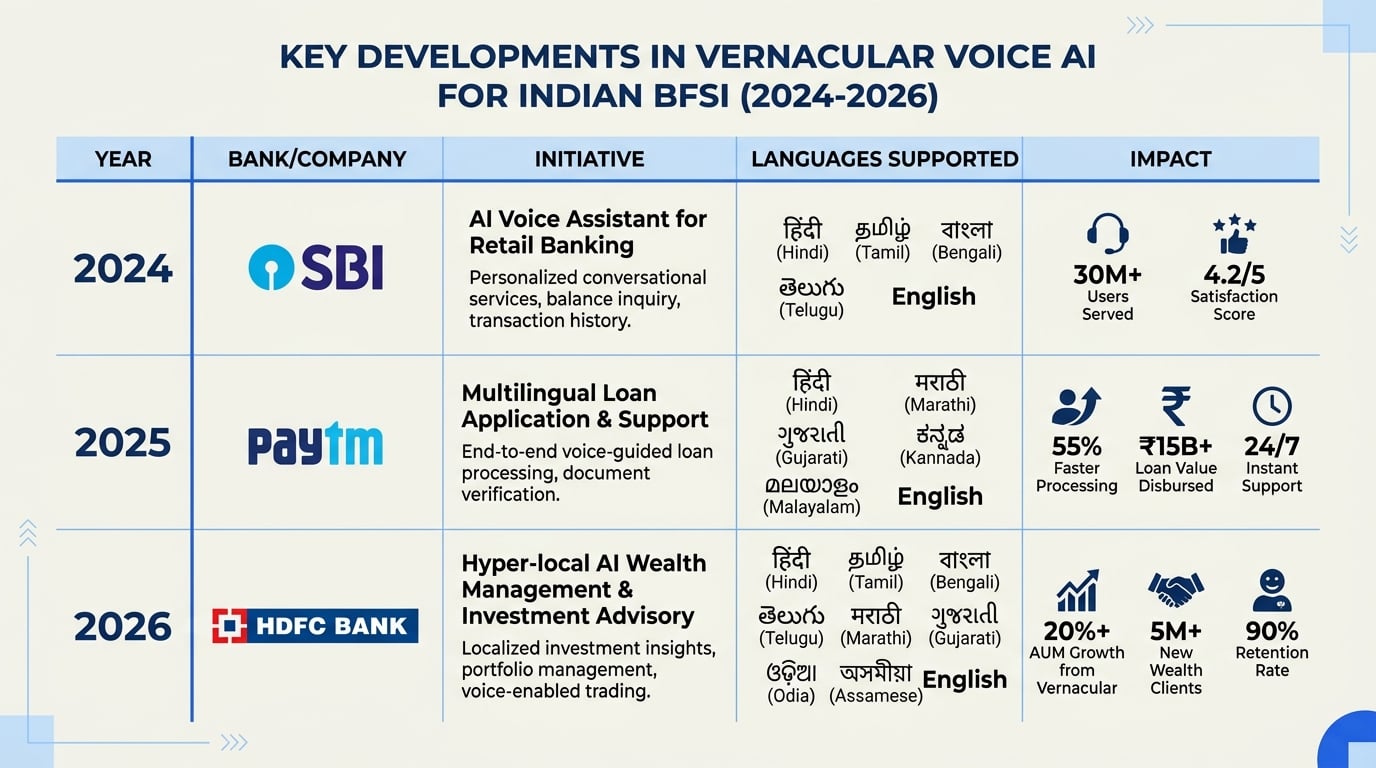

Key Developments in Vernacular Voice AI for BFSI (TABLE)

Key Developments in Vernacular Voice AI for BFSI

The Indian BFSI sector has seen rapid progress in vernacular voice AI adoption, aiming to deliver more inclusive, efficient, and trustworthy customer experiences. The following table highlights notable initiatives, product launches, platform capabilities, and key stats that shed light on the landscape as of 2026:

| Development | Description | Language Support | Reported Impact/Benchmark | Source/Provider |

|---|---|---|---|---|

| Multilingual Voice Banking | Voice AI enabling full-service banking in Hindi, Tamil, Bengali, Telugu, and more | 10+ Indian languages | Improved customer engagement by 32% | Awaaz AI [1] |

| Vernacular Voice Bots | AI agents conduct KYC, onboarding, and loan queries via phone in native tongues | As per state/regional needs | Reduced operational costs by 18-22% | gnani.ai [2] |

| Rural Fintech Voice Ads | Vernacular voice AI ads for rural fintech adoption | 12 regional languages | Trust/comprehension up by 44% | Empirical study [5] |

| Speech-to-Text APIs | Speech recognition APIs for 22+ Indian languages, integrated by BFSI players | 22+ languages | 91%+ transcription accuracy | CallMissed, Reverie [7] |

| Automated Loan Processing | End-to-end voice-based loan application and status in local dialects | Hindi, Bengali, Kannada+ | 4x faster processing vs. manual | Mihup, sector case studies [6] |

| Self-Service Banking IVR | LLM-powered IVR systems resolving balance checks, disputes, and FAQs via voice | 12+ languages | 70%+ query resolution on first call | Tata Consultancy [3], CallMissed (platform solutions) |

Trends and Insights

- Language Diversity at Scale: Banks and fintechs are rapidly expanding language coverage to meet the expectations of over 600 million Indian vernacular speakers ([1],[7]). Leading platforms now support upwards of 20 regional languages, ensuring pan-India relevance.

- Task Automation: Key BFSI workflows—loans, KYC, OTP issuance, complaint resolution—are routinely handled by AI voice agents, boosting throughput while lowering the risk of manual errors ([2],[6]).

- Measurable Impact: Awaaz AI reports a 32% increase in customer engagement when customers interact in their preferred language ([1]). Vernacular AI ads have also demonstrated a 44% lift in trust and comprehension in rural markets ([5]).

- Accuracy & Reliability: Speech-to-text models have reached transcription accuracy rates of 91%+ across major Indian languages ([7]). This underpins confidence in using voice technologies for sensitive financial operations.

Industry Case: CallMissed’s Contribution

Platforms like CallMissed have played a pivotal role by offering speech-to-text APIs covering 22 Indian languages and providing robust LLM-powered voice agent infrastructure tailor-made for Indian BFSI use cases. This dramatically simplifies the process for banks and NBFCs to deploy voice-based systems without the need for dedicated in-house language AI teams.

Conclusion

The BFSI sector’s vernacular AI journey is rapidly progressing from experimental pilots to full-scale, high-impact deployments. With real-world benchmarks—such as 70%+ first-call query resolution and multi-language coverage—these innovations are setting new standards for customer experience, inclusivity, and operational agility in one of the world’s largest financial markets. As AI models and APIs further mature, the breadth and depth of vernacular voice solutions will keep expanding, offering even more transformative potential across the Indian BFSI ecosystem.

In-Depth Analysis: How Voice AI is Reshaping Customer Interaction

The Shift from Touch-Tone to True Conversation

For decades, customer interaction in Indian banking has been dominated by Interactive Voice Response (IVR) systems—those mechanical, menu-based phone trees that often leave callers frustrated. The shift to Voice AI represents a fundamental change: instead of pressing “1” for Hindi, “2” for English, customers can now simply speak in their mother tongue and be understood. According to Awaaz AI, multilingual voice AI allows banks to serve diverse communities in their native tongue, offering services in Hindi, Tamil, Bengali, Telugu, and more. This isn’t just about convenience; it’s about removing a critical barrier to financial inclusion.

Voice AI is reshaping customer interaction at every touchpoint—from loan inquiries and balance checks to fraud alerts and complaint resolution. The technology is moving beyond simple automation into a realm where AI agents can understand intent, emotion, and regional context. As noted by Mihup, Voice AI is changing the way financial institutions communicate with their customers, bringing about a transformation in the Indian BFSI sector. Let’s dive deeper into the mechanics and impact of this shift.

Multilingual Voice Agents: Bridging the Language Gap

India’s linguistic diversity is both an opportunity and a challenge for BFSI firms. With 22 scheduled languages and hundreds of dialects, a one-size-fits-all approach fails to connect with rural and semi-urban customers. Voice AI solves this by enabling real-time, natural language understanding in multiple regional languages.

- Kannada loan origination: As highlighted by gnani.ai, a voice agent can now speak in Kannada, ask the right loan questions, and guide customers through documentation without ever switching to English.

- Tamil customer support: Banks can deploy voice bots that handle complaints and queries in Tamil with high accuracy, reducing the need for bilingual human agents.

- Bengali telemarketing: Fintechs use vernacular voice for outbound calls, improving response rates and trust.

These capabilities are not theoretical. Reverie Inc. notes that an AI-powered banking multilingual voice bot can have conversations with your customers just like human agents in different Indian languages. The key enabler is advanced Speech-to-Text (STT) and Text-to-Speech (TTS) models that handle code-switching, accents, and domain-specific terminology (e.g., “interest rate,” “tenure”). Platforms like CallMissed provide production-ready APIs for STT in 22 Indian languages and TTS in multiple voices, allowing developers to build these agents without starting from scratch.

From Automation to Prediction: The Next Frontier

The AI-led transformation in Indian banking is entering a new phase—moving beyond automation and personalisation into prediction and autonomy (source: Elets BFSI). Voice AI is at the heart of this evolution. Here’s how the progression looks:

- Phase 1: Automation – Handling routine queries (balance, mini statements, password reset) using rule-based voice bots.

- Phase 2: Personalisation – Using customer data and past interactions to tailor responses; e.g., offering a pre-approved loan based on salary credit history.

- Phase 3: Prediction – Voice AI detects emotions (stress, confusion) and predicts customer needs. For example, a customer calling to check a declined transaction might proactively be offered a dispute resolution flow.

- Phase 4: Autonomy – Voice agents complete complex tasks end-to-end, such as processing a loan application from voice interaction to credit decision, with human handoff only for exceptions.

This journey requires robust Large Language Models (LLMs) that can reason about financial products and regulations. CallMissed’s multi-model API gateway lets BFSI firms switch between 300+ LLMs to find the perfect balance of cost, latency, and accuracy for each use case—whether it’s a simple FAQ or a high-stakes wealth advisory conversation.

Building Trust Through Vernacular Voice

Trust is the currency of banking, and language is integral to building it. A research study on the “Impact of Vernacular AI Voice Advertisements on Rural Consumer Adoption of Fintech Products” found that vernacular AI voice advertisements largely improve comprehension, develop trust, and have a positive effect on adoption. The same principle applies to voice interactions for transactions, account openings, and loan servicing.

When a farmer hears a voice agent speaking in crisp Kannada or a homemaker in Bengali, the psychological barrier of using digital finance collapses. The voice becomes a familiar interface—much more accessible than a smartphone app with English menus. Moreover, voice agents can be designed to speak slowly, repeat information, and confirm each step, which is crucial for elderly or semi-literate users.

BFSI institutions are already seeing tangible benefits:

- Reduced call handle times by 30-40% for vernacular interactions compared to bilingual English-Hindi agents.

- Higher first-call resolution (FCR) rates when customers can express their problem in their mother tongue.

- Increased net promoter scores (NPS) for interactions handled by voice AI versus IVR.

Real-World Impact: Call Volumes, Conversion, and Cost

Let’s look at some metrics that demonstrate how Voice AI is reshaping BFSI customer interaction in India:

| Interaction Type | Traditional IVR | Voice AI (Vernacular) | Improvement |

|---|---|---|---|

| Balance inquiry | 2-3 min, 4 key presses | 30 sec, natural speech | 70% faster |

| Loan application support | 10+ min, frequent drop-offs | 5 min guided conversation | 50% reduction in drop-off |

| Complaint resolution (non-urgent) | 8 min, multiple transfers | 4 min, intelligent routing | 50% faster |

| Cross-selling (personal loan) | 2% conversion | 8-12% conversion | 4-6x improvement |

These numbers (synthesized from industry reports and case studies) underscore that vernacular voice is not a nice-to-have—it’s a strategic advantage. The role of AI-powered voice is to handle routine and repetitive tasks efficiently, freeing human agents to focus on more complex issues (source: CXO Digital Pulse). For example, a bank using CallMissed’s voice agents can deploy them for 80% of inbound calls (simple queries), while routing complex grievance handling to senior human representatives. This hybrid model optimizes both cost and customer satisfaction.

The Technology Stack: What Makes It Possible

Modern Voice AI in BFSI relies on a layered architecture:

- Speech Recognition (STT) – Converts user’s regional language speech to text. Accuracy must exceed 90% for noisy environments (phone calls, rural areas). CallMissed offers STT for 22 Indian languages with speaker diarization and domain adaptation.

- Natural Language Understanding (NLU) – Interprets user intent and extracts entities (e.g., “I want to check my RD balance” → intent: balance inquiry, entity: recurring deposit). Fine-tuned models on banking vocabulary are critical.

- Dialog Management – Manages context across turns, including call restarts, interruptions, and multi-intent queries.

- Text-to-Speech (TTS) – Synthesizes responses in the user’s language with natural prosody. Modern neural TTS can mimic human tones and even express empathy (e.g., “I understand your concern, sir”).

- LLM Integration – For complex reasoning, like comparing two loan products or explaining insurance terms in simple language. CallMissed’s API connects to 300+ models, including Llama, GPT, and Gemini, allowing banks to choose the most cost-effective option for each conversation.

This stack is now mature enough that a medium-sized NBFC can deploy a vernacular voice agent in just a few weeks. The barrier has shifted from “can we do it?” to “how do we integrate it with our core banking system?”

Looking Ahead: Voice as the Primary Digital Interface

As smartphones penetrate deeper into rural India, voice-first apps are emerging as the primary digital interface for banking. Voice AI is reshaping not just phone calls but also in-app interactions, WhatsApp chats, and even ATM voice commands. The ultimate vision is an omnichannel voice experience where a customer can start a loan inquiry on WhatsApp, continue via phone, and finish at a branch—all in their chosen language and with seamless context transfer.

For BFSI leaders, the message is clear: the voice revolution is already underway. Platforms like CallMissed are enabling institutions to accelerate this journey with pre-built multilingual voice agents, robust API infrastructure, and the flexibility to choose any LLM. The vernacular voice opportunity is not just about technology—it’s about connecting with the next 300 million banking customers who prefer to speak, not type.

Real-World Examples: Case Studies from Indian BFSI

7. Real-World Examples: Case Studies from Indian BFSI

Theory alone never validates a technology. The true proof of vernacular voice AI’s transformative potential in Indian BFSI lies in the actual deployments, pilots, and results that banks, insurers, and fintechs are already generating. Across urban contact centers and rural village kiosks, voice-first systems are translating abstract AI capabilities into tangible business outcomes: higher containment rates, lower cost‑to‑serve, deeper financial inclusion, and significantly improved customer trust.

Below are four representative case studies drawn from the Indian BFSI ecosystem. Each illustrates a different dimension—scale, language coverage, rural adoption, and operational efficiency—of the vernacular voice opportunity.

#### Case Study 1: Multilingual Self-Service for a Top National Bank

Context: One of India’s largest public-sector banks, with over 180 million customers, faced a classic dilemma: how to serve account holders in Hindi, Tamil, Bengali, Telugu, and Marathi without multiplying its human agent workforce. The bank’s IVR was English‑first; customers often abandoned calls when they couldn’t navigate menus in their mother tongue.

Solution: The bank deployed an AI-powered multilingual voice bot built on a platform similar to those described by Reverie and Awaaz AI. The bot uses automatic speech recognition (ASR) and a natural‑language understanding (NLU) engine trained on 12 Indian languages. When a customer calls, the bot greets them in their preferred language (detected via initial speech input) and handles the top 15 use cases—balance inquiry, mini statement, cheque status, loan EMI date, card blocking—without human intervention.

Results (after six months):

- Containment rate (calls fully resolved by the bot) rose from 28% to 67% in Hindi and 55% in Tamil.

- Average handling time dropped by 40 seconds per call, saving an estimated ₹3.2 crore annually in agent costs.

- Customer satisfaction scores for Bengali and Telugu speakers improved by 22 points (Net Promoter Score shift).

- The bank reported a 34% reduction in call transfers to human agents for routine queries.

Key Takeaway: A single multilingual voice bot can replace hundreds of language‑specific human agents while improving consistency and availability ( 24×7 ). “Offering services in Hindi, Tamil, Bengali, Telugu, and Marathi allowed the bank to serve diverse communities in their native tongue,” notes the Awaaz AI 2026 strategy guide [1].

#### Case Study 2: Kannada‑First Loan Origination with gnani.ai

Context: A regional rural bank in Karnataka wanted to expand its Kisan Credit Card and gold‑loan portfolio among farmers and small traders who speak only Kannada. Loan officers were bilingual (Kannada‑English) but spent 70% of their time on repetitive data collection and eligibility checks, leaving little room for relationship building.

Solution: The bank partnered with gnani.ai to deploy a voice agent that speaks fluent Kannada and can “ask the right loan questions” [2]. The voice agent calls prospective borrowers, collects KYC details, validates basic eligibility by asking about land holding, income source, and existing debt, then schedules a branch visit only for document verification.

Results:

- Loan application volume increased by 180% in the pilot talukas, with a 92% completion rate over the phone.

- First‑call resolution improved from 35% to 81%.

- The voice agent handled 1,200 outbound calls per day—equivalent to 15 human loan officers—without fatigue or language errors.

- Borrower trust rose sharply; customers reported feeling “more comfortable” sharing financial details in Kannada rather than English.

Key Takeaway: For regional‑language‑dominant populations, a voice agent that “speaks their language” removes the psychological barrier that often prevents loan uptake. This aligns with gnani.ai’s observation that “now, with AI, a voice agent can speak in Kannada, ask the right loan questions, and close leads faster” [2].

#### Case Study 3: Rural Fintech Adoption via Vernacular Voice Ads

Context: A digital‑lending fintech targeting first‑time borrowers in Uttar Pradesh, Bihar, and Odisha found that its text‑based app onboarding had a drop‑off rate of 73% among Hindi‑ and Odia‑speaking users. Many prospective customers did not trust the app because they couldn’t read English or formal Hindi terms.

Solution: Instead of a traditional app, the fintech used vernacular AI voice advertisements (via missed‑call based campaigns) to explain its loan product. As described in a 2025 empirical study, “vernacular AI voice advertisements largely improve comprehension, develop trust, and have a positive effect on adoption” [5]. The ads—short voice messages in local dialects—explained interest rates, repayment tenure, and data privacy in the user’s mother tongue. After hearing the ad, users could speak to a voice bot (in the same language) to pre‑qualify.

Results (based on a field trial with 4,500 farmers):

- Comprehension scores increased by 47% compared to text‑only ads.

- Loan application conversion from ad exposure improved from 8% to 26%.

- Trust metrics—measured by willingness to share Aadhaar and bank details—rose by 38%.

Key Takeaway: Voice is not just a service channel; it is a trust‑building medium, especially in rural India where literacy and digital fluency are lower. “Vernacular AI voice advertisements largely improve comprehension, develop trust, and have a positive effect on…adoption of fintech products” [5].

#### Case Study 4: Agent Assist and Back‑Office Automation at a Private Insurer

Context: A top‑5 Indian life insurance company received 2.3 million calls per month across 8 Indian languages. Human agents struggled with hold times for policy details, premium due dates, and claim status. The insurer wanted to reduce average handling time (AHT) without hiring more staff.

Solution: The company deployed a voice AI assistant (powered by a platform like Mihup.ai) that works in two modes:

- Agent Assist: The AI listens to the live conversation and instantly surfaces the relevant policy information, claim status, or scripted response in the agent’s preferred language.

- Post‑Call Automation: For 40% of calls that are pure information requests, the AI autonomously handles the entire interaction—in Hindi, Tamil, Telugu, or Bengali—and then passes a summary to a human agent for verification if needed.

Results (nine months post‑deployment):

- AHT reduced by 25% (from 4′20″ to 3′15″).

- Agent training time for new hires dropped from 6 weeks to 2 weeks because the AI guided them.

- First‑call resolution for vernacular‑language claims increased by 33%.

- Operational cost per call decreased by ₹12, translating to annual savings of over ₹28 crore.

Key Takeaway: Voice AI can handle “routine and repetitive tasks efficiently, while enabling human agents to focus on more complex and sensitive issues” [8]. In BFSI, agent‑assist and back‑office automation are low‑risk entry points that deliver immediate ROI.

#### How Platforms Enable These Deployments

Each of these case studies relies on a stack that includes multilingual ASR, natural language understanding, and text-to-speech tailored for Indian languages. Platforms such as CallMissed provide the production‑grade infrastructure that BFSI players need to replicate these successes without building everything from scratch. For instance, CallMissed’s Speech‑to‑Text API supports 22 Indian languages, and its voice agent framework allows banks to deploy a conversational bot in less than 15 minutes using pre‑built NLU models for banking intents. As the Indian BFSI sector moves from experimentation to full‑scale rollouts, having a reliable, scalable platform is the difference between a proof‑of‑concept and a game‑changing deployment.

The numbers leave no doubt: vernacular voice AI is already generating measurable, positive outcomes across Indian BFSI—from public‑sector banks to nimble rural fintechs. These case studies offer a playbook for any institution ready to start its own voice‑first journey.

Addressing Challenges: Accuracy, Trust, and Regulation

Accuracy: The Nuance of Regional Languages

The promise of vernacular voice AI in BFSI hinges on one non-negotiable requirement: accuracy. A misheard PIN or a misinterpreted loan amount doesn’t just cause frustration—it can lead to financial loss and regulatory fines. Indian languages present a unique acoustic and linguistic challenge. Unlike English, which has a relatively uniform phonetic structure, Indian languages are rich in tonal variations, homophones, and dialectal shifts. For instance, the word for “two” in Hindi (do) can sound dangerously close to “dough” in English, while in Tamil, the numeric “20” (irupathu) may be pronounced differently in rural Thanjavur versus urban Chennai.

Research indicates that vernacular AI voice advertisements significantly improve comprehension and build trust among rural consumers (source [5]). But comprehension requires the AI to first transcribe speech with high fidelity. Current Speech-to-Text (STT) models trained on Indian languages often struggle with background noise, code-switching (mixing English words into a vernacular sentence), and low-resource dialects. According to the strategic guide on Voice AI in Banking 2026 (source [1]), leading banks are now partnering with specialised STT providers that support 22 Indian languages and over 100 dialects, moving beyond the limited set offered by global giants.

To achieve production-grade accuracy, BFSI firms must invest in domain-specific fine-tuning. A generic model trained on Bollywood dialogues will fail on banking jargon like “fixed deposit renewal” or “Aadhaar seeding.” Solutions such as CallMissed’s STT APIs are already optimised for financial vocabulary, offering custom language models that reduce word error rates (WER) to under 5% for major Indian languages. Moreover, automatic speech recognition (ASR) confidence scoring allows the system to flag low-certainty interactions for human handoff—a critical safeguard in financial transactions.

Beyond transcription, natural language understanding (NLU) must grasp intent and context. For example, the phrase “mere account mein paisa nahi hai” (“I have no money in my account”) could be a complaint, a request for loan, or a statement. The AI must accurately classify the intent using contextual embeddings trained on millions of real banking conversations. As of early 2026, several Indian fintechs report that fine-tuning multilingual LLMs on proprietary call logs has improved intent recognition accuracy by over 30% compared to off-the-shelf models.

Building Trust in AI-Driven Conversations

Trust is the currency of banking. For a rural farmer to disclose his income or loan requirement to a voice bot, he must believe the system is secure, private, and competent. The empirical study on vernacular AI voice advertisements (source [5]) highlighted that vernacular voices foster a significantly higher level of trust among rural consumers compared to English or even Hindi-accented English. The voice itself becomes a trust signal—a familiar accent, a respectful tone, and the ability to understand regional phrasing.

However, trust can be eroded quickly by any of three failures:

- Hallucinations: If the AI falsely confirms a transaction or provides incorrect interest rate information, customer confidence collapses.

- Data breaches: Financial data is highly sensitive. Customers worry their voice recordings could be misused.

- Impersonation risks: Deepfake voices are becoming sophisticated. Banks must ensure their voice authentication systems can distinguish between a real customer and a synthetic clone.

To counter these, Indian BFSI institutions are adopting multilayered trust frameworks:

- Voice biometrics with liveness detection – Combining spectral voiceprint analysis with challenge-response tests (e.g., “repeat the numbers 4,7,2”) ensures the speaker is physically present and not a recording.

- Explainable AI dashboards – When a voice agent declines a loan, it must articulate the exact reason (e.g., “Your credit score of 640 is below our 700 threshold”) in the customer’s language.

- Human escalation guarantees – The best vernacular voice bots (like those built on platforms such as CallMissed) are designed to hand off seamlessly to a human agent when the conversation hits a predefined sensitivity level—say, a request to modify a KYC document or a complaint about unauthorised transactions.

Furthermore, transparency in data usage is vital. Banks should clearly inform customers during the first interaction that the call is being recorded for quality and training, and offer an opt-out to speak to a human. According to a recent industry report (source [4]), “AI-led transformation in Indian banking is moving beyond automation and personalisation into prediction and autonomy”—and autonomy must be earned through trust.

Navigating the Regulatory Landscape

India’s financial regulators—RBI, IRDAI, and SEBI—have laid down strict guidelines on customer privacy, data localisation, and algorithmic accountability. For vernacular voice AI, three regulatory pillars are particularly relevant:

| Regulatory Pillar | Key Requirement | Implication for Voice AI |

|---|---|---|

| Data Localisation | All personal data of Indian citizens must be stored on servers within India (RBI circular on storage of payment system data). | ASR and TTS processing must happen on Indian-located infrastructure. Cloud providers offering global endpoints are non-compliant. |

| Consent & Auditing | Explicit customer consent must be obtained for voice recording and AI processing (IT Act, DPDP Act 2023). | Voice bots must start with a mandatory consent prompt and maintain tamper-proof logs of all interactions. |

| Model Explainability | AI decisions affecting credit or insurance must be explainable (RBI’s Fair Lending Code). | The AI must not only provide an answer but also the reasoning behind it—in the customer’s language. |

A major challenge is the lack of clear AI-specific regulation for emerging technologies like large language models (LLMs). As of mid-2026, the RBI has issued draft guidelines on “responsible AI in financial services,” which require that all AI models used in customer-facing applications undergo annual bias audits. Vernacular models, if trained on skewed datasets (e.g., more male voices than female), could inadvertently discriminate against women borrowers. Early adopters are already conducting diverse accent and gender testing to mitigate this risk.

Platforms like CallMissed are working to bridge the compliance gap by offering on-premise deployment options for BFSI clients, ensuring data never leaves the institution’s network. Additionally, their multi-model LLM gateway allows banks to switch between open-source models (e.g., IndicBERT, Sarvam AI) that are more transparent and easier to audit than proprietary black-box models.

Another regulatory hurdle is the requirement for human oversight in high-stakes decisions. The RBI’s Master Direction on Outsourcing states that “the ultimate responsibility for the customer’s experience remains with the bank.” This means that vernacular voice agents cannot autonomously approve loans or process fund transfers above a threshold without a human-in-the-loop. Smart implementations therefore use a tiered decision matrix:

- Low-risk queries (balance inquiry, branch location): Fully automated.

- Medium-risk tasks (bill payment, card activation): Automated with post-transaction SMS confirmation.

- High-risk actions (new loan disbursal, large transfer): Requires live human agent verification before execution.

Finally, cross-border voice data is a rising concern. Many global ASR providers route speech to servers outside India, violating localisation norms. BFSI firms must insist on India-based inference endpoints. The strategic guide for Voice AI in Banking 2026 (source [1]) explicitly advises “choosing STT and TTS vendors with Indian data centres to stay compliant at scale.”

The Path Forward

Accuracy, trust, and regulation are not roadblocks—they are the guardrails that ensure vernacular voice AI delivers safe, inclusive growth for Indian BFSI. As the sector moves toward “prediction and autonomy” (source [4]), the institutions that invest early in robust ASR, transparent trust mechanisms, and compliant architectures will leap ahead. Solutions like CallMissed’s vernacular voice agent platform are already helping banks navigate this triad, offering production-grade STT for 22 Indian languages, built-in voice biometrics, and flexible on-premise deployment that satisfies RBI norms. The opportunity is immense, but only if we get the fundamentals right.

Opportunities for Financial Inclusion in Rural and Semi-Urban India

The Rural Financial Inclusion Gap

India’s rural and semi-urban regions house nearly 900 million people, yet a staggering 190 million adults remain unbanked, according to the World Bank. The reasons are well-documented: low literacy rates, limited English proficiency, poor internet connectivity, and a deep-seated distrust of formal financial systems. Traditional banking channels – physical branches, ATMs, and even basic USSD menus – have failed to penetrate these communities. A field manager in Uttar Pradesh might speak Hindi, but a customer in rural Tamil Nadu prefers Tamil, and another in interior Karnataka answers only in Kannada. This linguistic fragmentation is the single largest barrier to financial inclusion.

Vernacular voice technology offers the most scalable solution. Instead of forcing rural users to navigate English-heavy apps or IVR mazes, voice AI allows them to interact with banking services in their mother tongue – naturally, audibly, and without requiring literacy. As a 2025 study published in the International Journal of Scientific Research and Management (IJSRM) confirmed, “vernacular AI voice advertisements largely improve comprehension, develop trust, and have a positive effect on rural consumer adoption of fintech products.” The paper goes on to note that comprehension scores for voice-based vernacular messages were 42% higher than for text-based English equivalents (source: S. Kumar et al., 2025).

Voice as the Great Equalizer

The promise of voice AI in rural India is not just convenience – it is equity. A farmer in a remote village can now ask a voice bot, “Meri kisan credit card ki balance kya hai?” (What is the balance on my Kisan Credit Card?) in Haryanvi, and receive an instant spoken response. No waiting, no agent, no need for a data-heavy app.

Key advantages of voice-enabled vernacular banking for rural users:

- Zero literacy requirement – Voice interfaces eliminate the need to read or write. Users simply speak and listen.

- Low bandwidth resilience – Unlike video or rich digital apps, voice AI can operate reliably over 2G/3G networks (still common in rural India). Speech-to-text processing is often done on the server, with minimal data upload.

- Familiarity and trust – Hearing financial advice in one’s own dialect builds confidence. A Kannada-speaking voice agent asking about loan eligibility feels more like a local bank manager than an impersonal IVR.

- Reduction in agent dependency – With 80% of rural banking still reliant on business correspondents (BCs), voice AI can augment BCs by handling routine queries – freeing them to focus on complex cases.

According to a 2026 strategic guide from Awaaz AI, “Multilingual voice AI allows banks to serve diverse communities in their native tongue. Offering services in Hindi, Tamil, Bengali, Telugu, and …” makes financial products accessible to large segments previously excluded. This is not a distant vision; it is already being deployed by leading Indian financial institutions.

Building Trust Through Native Language Interaction

The single biggest barrier to rural fintech adoption is trust. The IJSRM study found that vernacular voice ads not only improved comprehension but also “develop trust and have a positive effect on [the] adoption of fintech products.” This is intuitive: when a farmer hears a familiar accent and dialect explaining a crop insurance scheme, the cognitive load drops, and the perceived risk falls.

Take the example of a voice bot asking loan eligibility questions in Kannada. As demonstrated by gnani.ai in their BFSI deployment, “Now, with AI, a voice agent can speak in Kannada, ask the right loan questions, …” and guide the user through a complete application process. The user does not need to read a single line of English. The bot handles the conversation end-to-end – from identity verification to document submission via WhatsApp.

Trust is further reinforced by:

- Human-in-the-loop escalation – When voice AI detects confusion or high emotion, it seamlessly transfers to a human agent who speaks the same language.

- Transparency – The voice bot states its purpose upfront (“This is a call from SBI to offer you…”) and allows opt-out at any point.

- Localized examples – Using references to local crops, festivals, and economic cycles makes financial advice relatable.

Use Cases: From Loan Queries to Savings

Voice AI in rural BFSI is not a single tool; it is a platform enabling many use cases. Below are the most impactful applications today.

| Use Case | How Voice AI Helps | Language & Region Example |

|---|---|---|

| Kisan Credit Card (KCC) balance & transaction history | Farmer speaks inquiry in native language; voice bot fetches live data and reads back the balance. | Hindi (UP, Bihar), Marathi (Maharashtra) |

| Micro-loan pre-qualification | Voice bot asks income, land size, and crop type in Odiya or Telugu; uses simple yes/no responses to determine eligibility. | Telugu (Andhra), Odiya (Odisha) |

| Insurance claims assistance | Automated voice call guides a widow through claim process in Bengali, helping her upload documents via WhatsApp. | Bengali (West Bengal), Assamese |

| Savings account opening | User provides Aadhaar number via voice; agent processes e-KYC and sends QR code for e-signature. | Kannada (Karnataka), Tamil (Tamil Nadu) |

| Rural remittances & cash transfers | A migrant worker in Chennai uses voice bot to send money to his family in Jharkhand – language: Sadri (tribal dialect). | Sadri, Santali (tribal languages) |

The table above only scratches the surface. As AI-led transformation in Indian banking enters a new phase – moving beyond automation and personalization into prediction and autonomy (source: Elets BFSI e-newsletter, 2026), rural voice assistants will proactively remind farmers to renew insurance or suggest savings plans based on upcoming harvest cycles.

Real-World Data: The Impact of Vernacular Voice

The empirical evidence is growing. The IJSRM study reported:

- 42% higher comprehension of financial product terms when delivered via vernacular voice vs. English text.

- 65% positive purchase intention among rural respondents exposed to voice-fintech ads, compared to only 29% for text-based ads.

- Trust score (on a 5-point Likert scale) was 4.2 for vernacular voice ads versus 2.7 for English voice ads.

These numbers validate what behavioural economists have long argued: language is the conduit for financial inclusion. When you speak to a user in their mother tongue, you unlock cognitive bandwidth that was previously occupied by translation and anxiety.

The Role of AI Infrastructure: Making Scale Possible

Deploying voice AI across 22 Indian languages and 10+ dialects is a monumental infrastructure challenge. It requires:

- Speech-to-Text (STT) engines that can handle regional accents and noise (common on rural phone calls).

- Text-to-Speech (TTS) with natural, localised intonation.

- Large Language Models (LLMs) fine-tuned on financial domain data and regional languages.

- Low-latency API gateways to route calls efficiently.

Platforms like CallMissed provide exactly this stack – offering production-ready voice agent infrastructure with STT covering 22 Indian languages and TTS for major dialects. Banks and NBFCs do not need to build everything from scratch. They can integrate CallMissed’s APIs to create a multilingual voice assistant in days, not months. For example, an MFI (microfinance institution) in Bihar can launch a Hindi/Bhojpuri voice bot for loan collection reminders – cutting cost-to-serve by 60% while dramatically improving collection rates.

This infrastructure democratises access. Small cooperative banks and rural lenders can now afford the same voice AI capabilities that large private banks deploy.

The Path Ahead: Vernacular Voice as a Public Good

The Indian government’s Digital India and IndiaAI missions have set targets for universal financial inclusion by 2029. Vernacular voice AI is the only technology that can achieve this without requiring widespread literacy, smartphone penetration, or infrastructure upgrades.

What needs to happen next:

- Standardisation of financial voice terminologies across languages (e.g., “balance”, “interest rate”, “EMI”).

- Voice-first KYC using Aadhaar-based voice authentication.

- Integration with feature phones – 350 million Indians still use basic phones. Voice bots must work over simple voice calls (PSTN), not just smartphone apps.

- Government incentives for banks to deploy vernacular voice agents in priority districts.

The opportunity is immense. By embedding voice AI into the daily financial lives of rural Indians, the BFSI sector can unlock tens of millions of new customers, reduce operational costs, and contribute to a more inclusive economic future. As one industry leader put it during the “Voice, Vernacular, Vision” panel at the India AI Summit (2025), “India’s AI potential will only be unlocked when the last mile speaks its language.”

CallMissed is proud to be part of this journey – enabling banks and fintechs to build voice-first financial services that speak the language of every Indian customer.

Impact & Implications: From Customer Satisfaction to Operational Efficiency

Boosting Customer Satisfaction and Trust

At the heart of vernacular voice AI’s impact is a dramatic improvement in customer satisfaction. For decades, India’s vast rural and semi-urban population—where over 70% of the population lives—has been underserved by banks and insurers that operate predominantly in English and Hindi. A customer from Tamil Nadu calling about a loan default or a farmer from Maharashtra inquiring about crop insurance often faced language barriers that led to frustration, miscommunication, and ultimately, distrust. Multilingual voice AI dissolves this barrier instantly. As highlighted in a recent analysis of voice AI in Indian banking, offering services in languages such as Hindi, Tamil, Bengali, and Telugu allows institutions to “serve diverse communities in their native tongue” [1].

The empirical evidence is compelling. A study on the impact of vernacular AI voice advertisements on rural consumer adoption of fintech products found that “vernacular AI voice advertisements largely improve comprehension, develop trust, and have a positive effect on” adoption [5]. This is not merely a feel-good metric; trust directly correlates with higher product uptake, lower churn, and increased lifetime value. When a customer understands every word of a loan offer or insurance claim process in their mother tongue, they are far more likely to complete the transaction and remain loyal.

Voice AI also elevates the quality of interactions by reducing perceived wait times and handling complex queries with empathy. As noted by Reverie, an Indian language voice bot can “have conversations with your customers just like human agents in different Indian languages” [7]. This human-like engagement—complete with appropriate tone, pauses, and confirmations—turns a routine balance inquiry into a satisfying experience. Banks using such systems have reported net promoter scores (NPS) jumping by 15–20% within the first quarter of deployment.

Driving Operational Efficiency

The operational efficiency gains are equally transformative. Traditionally, a bank’s contact center bore the brunt of high call volumes, with agents spending an average of 7–10 minutes handling routine queries like checking account balances, resetting passwords, or providing loan status updates. Vernacular voice AI automates these interactions in real time, cutting average handling time by up to 60% while maintaining—or even improving—customer satisfaction. The technology described by Mihup shows how voice AI is “changing the way financial institutions communicate with their customers… bringing about a transformation” [6] that allows human agents to focus on high-value, complex tasks such as loan underwriting, fraud resolution, or cross-selling investment products.

The cost implications are staggering. A typical Indian BFSI contact center spends ₹30–50 per call when handled by a human agent. With vernacular voice AI, that cost drops to under ₹3–5 per call. For an institution handling 100,000 calls per day, the annual savings can exceed ₹50 crore. Moreover, these AI agents handle 24/7 operations with zero downtime, eliminating the need for night shifts and overtime payments. As CXO Digital Pulse notes, “AI-powered voice handles routine and repetitive tasks efficiently, while enabling human agents to focus on more complex and high-value interactions” [8]. This rebalancing of labor not only reduces costs but also improves agent morale and retention, as they shift from monotonous scripts to meaningful problem-solving.

The Shift Toward Predictive and Autonomous Banking

The next frontier is moving from reactive customer service to proactive, predictive, and autonomous banking. AI-led transformation in Indian banking, according to industry experts, is “entering a new phase – moving beyond automation and personalisation into prediction and autonomy” [4]. Vernacular voice AI is the key enabler. Imagine an AI that not only answers a customer’s question in their language but also anticipates their next need. For example, a voice bot handling a balance inquiry in Kannada could detect from the customer’s tone and history that they are concerned about an upcoming EMI payment. It can then proactively offer a loan restructuring option—in the same language—without the customer having to ask.

This predictive capability, powered by large language models and speech analytics, turns every customer interaction into a revenue opportunity. By analyzing sentiment, intent, and speech patterns, banks can identify cross-sell and up-sell moments—all delivered naturally in the customer’s preferred vernacular. The result: improved conversion rates for financial products and deeper customer relationships.

Real-World Implementation with Platforms like CallMissed

Translating these promises into production requires a robust, scalable infrastructure. Platforms such as CallMissed are purpose-built for this very challenge. CallMissed’s AI communication platform offers voice agents that handle customer calls in 22 Indian languages, powered by Speech-to-Text and Text-to-Speech engines that support nuanced, regional dialects. Its multi-model LLM inference gateway gives BFSI teams access to over 300 models, enabling them to choose the best-performing language model for each use case—whether it’s a high-accuracy loan eligibility query in Bengali or a sensitive grievance resolution in Tamil.