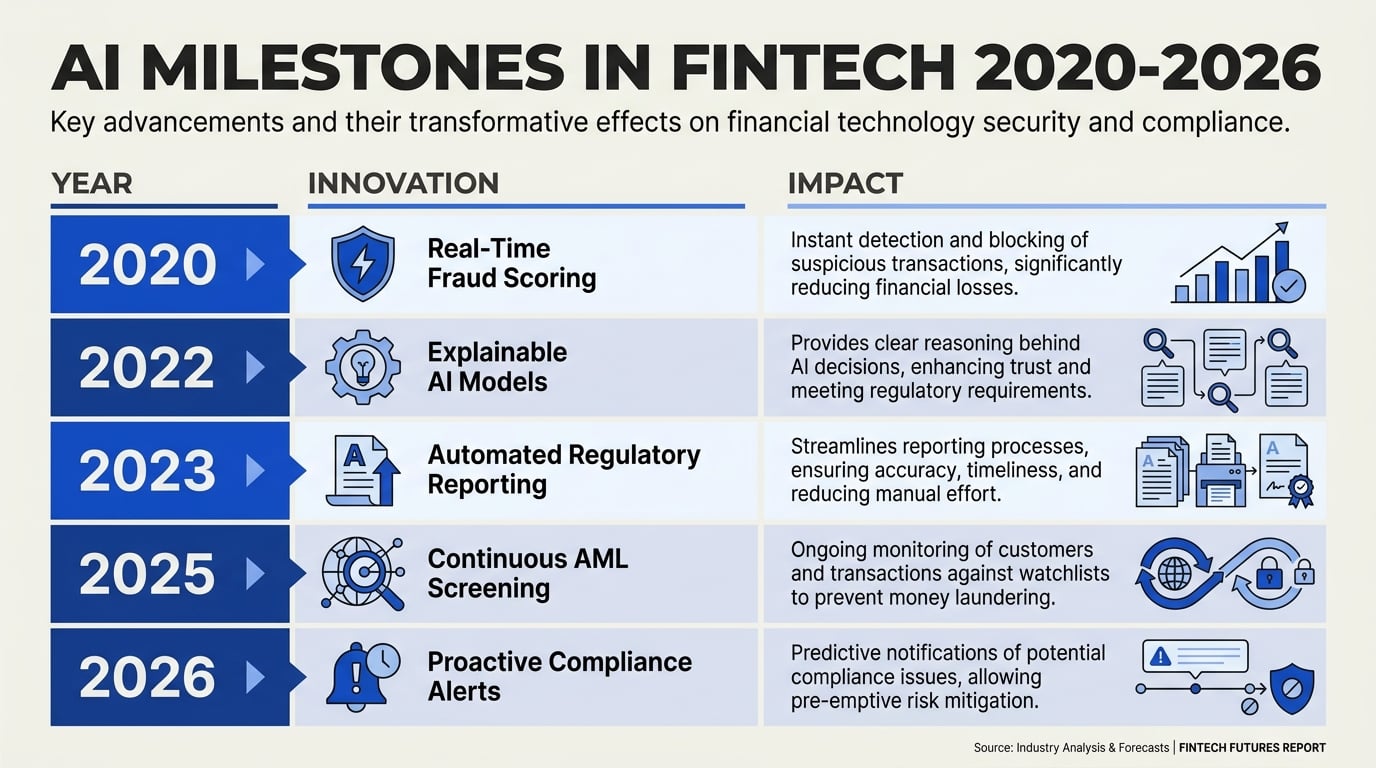

AI in Fintech: Fraud Detection and the Compliance Question

Is your bank chatbot smarter than the average thief? As of 2026, the answer may be yes, thanks to the meteoric rise of AI in fintech—particularly in the...

AI in Fintech: Fraud Detection and the Compliance Question

Is your bank chatbot smarter than the average thief? As of 2026, the answer may be yes, thanks to the meteoric rise of AI in fintech—particularly in the critical arms race of fraud detection and compliance. Financial institutions today face an unprecedented scale and sophistication of cyber threats. According to IBM, global financial fraud losses reached over $32 billion last year, an all-time high driven by new attack vectors and the rising speed of digital transactions. For the perpetrators, automation and AI are tools of the trade. For the defenders, they are now an absolute necessity.

Traditional fraud detection systems, built on static rules and manual reviews, are buckling under the explosion of digital activity. The rapid adoption of real-time payments, contactless transactions, and cross-border fintech solutions has amplified transaction volumes—and potential vulnerabilities—by orders of magnitude. A single misstep doesn’t just risk financial losses; non-compliance with regulations like AML, KYC, and GDPR can trigger massive fines and erode public trust. It’s no surprise Gartner recently named AI-driven compliance as one of the top five fintech disruptors for the year.

So, why is AI rewriting the playbook for fraud prevention and regulatory adherence right now? First, machine learning algorithms can parse millions of data points in real-time, flagging anomalies far faster and more accurately than traditional methods. Second, these same systems evolve continuously, learning new attack patterns as fast as cybercriminals invent them. In fact, research from NayaOne found that AI-based anti-money laundering (AML) tools can reduce false positives by up to 70%, slashing operational costs and freeing up teams to focus on genuine risks.

Yet, this new era of AI in fintech is not just about speed—it’s about smarter, more nuanced defense. Where rule-based engines often miss subtle fraud trends or drown teams in false alarms, AI models analyze transaction histories, user behavior, geographical patterns, and even biometric cues, uncovering risks hidden in plain sight. As ImpressIT notes, this has enabled financial platforms to preemptively block suspicious activity and adapt to emergent threats almost instantly.

But powerful AI systems come with their own set of compliance questions and regulatory tensions. How do you explain a model’s black-box decision to an auditor or a customer denied a transaction? How do you ensure AI doesn’t inadvertently perpetuate bias or violate evolving privacy laws? These are complex, high-stakes challenges that every forward-thinking financial service provider now faces.

This blog will help you navigate the double-edged sword of AI in fintech: first, by detailing how machine learning is revolutionizing fraud detection—from anomaly scoring to explainable AI and real-world case studies; next, by unpacking the regulatory frameworks shaping AI deployment, the balancing act between innovation and compliance, and the practical steps to make your fraud defenses both agile and audit-proof.

Throughout, we’ll highlight how industry players—especially those building modular AI infrastructure—are closing the gap. Platforms like CallMissed, for example, are enabling fintechs and banks to harness 300+ AI models for real-time fraud analysis and multilingual compliance automation, a crucial advantage in diverse, high-growth markets.

The stakes have never been higher. Whether you’re a fintech founder, a compliance manager, or simply a digital banking customer, the intersection of AI, fraud detection, and regulatory compliance will shape your experience in the financial world—today and tomorrow. Read on to discover the data, strategies, and technology powering this transformation.

Introduction: The New Frontlines of Fintech Security

The digital transformation of financial services has created unprecedented opportunities for both consumers and institutions. At the same time, the fintech sector has quickly risen to become a preferred target for cybercriminals exploiting the rapid evolution of digital payment channels, complex regulatory environments, and global transaction flows. According to the World Economic Forum, digital fraud costs the global economy over $5 trillion annually—a figure driven in large part by fast-moving digital financial platforms (Source: [WEF, 2026]). In this context, the adoption of artificial intelligence (AI) has emerged as an indispensable shield, redefining the frontlines of fintech security and compliance.

The Expanding Surface of Financial Threats

Fintech institutions process billions of transactions daily, working across payment, lending, insurance, and investment domains. This digital landscape presents a vast attack surface:

- Sophisticated Fraud Schemes: Phishing, account takeovers, synthetic identity fraud, mule networks, and transaction laundering are rising in both frequency and complexity.

- Regulatory Pressures: Compliance with anti-money laundering (AML), know-your-customer (KYC), and data privacy regulations is non-negotiable, with authorities levying billions in fines annually for non-compliance (e.g., over $10.4 billion in global AML fines in 2023, Source: [Finextra, 2024]).

- Legacy System Limitations: Traditional rule-based systems struggle to keep up with adaptive fraud tactics and evolving regulatory requirements.

It's no surprise, then, that a 2025 PwC survey found that 76% of global fintech firms ranked "advanced fraud prevention" and "real-time compliance monitoring" as their top technology investment priorities. As firms race to protect integrity and retain consumer trust, AI is stepping in as a force multiplier.

How AI Is Redefining Fraud Detection

AI-driven solutions are pushing security boundaries far beyond what was possible with static, rules-based methods. Leading fintech players are deploying diverse AI models to monitor, assess, and preempt fraudulent behavior in real time:

- Anomaly Detection: Machine learning models analyze historical transaction patterns to establish behavioral baselines for each user. Unusual activities—such as high-value transfers from new locations—can be flagged instantly.

- Network Analytics: AI uncovers complex relationships between accounts, detecting mule networks and synthetic identity rings that manual audits might miss.

- Adaptive Learning: Unlike static systems, AI continuously learns from new fraud typologies, reducing latent risk.

IBM notes that banks using AI systems can detect fraud patterns almost 60% faster on average, while minimizing disruptions to legitimate customer transactions (Source: [IBM, 2026]). By leveraging large-scale behavioral data, these systems have achieved a 30–40% reduction in false positives—a critical differentiator for customer experience.

Compliance: The Double-Edged Sword

AI’s ability to process unstructured data and draw context-sensitive inferences makes it equally compelling for compliance:

- AML Monitoring: A recent study cited by NayaOne found that AI can reduce false positives in AML compliance by up to 70%, significantly slashing operational costs and investigator workloads (Source: [NayaOne, 2024]).

- Automated KYC: Natural language processing (NLP) and vision AI streamline customer onboarding, verifying documents and monitoring client risk in real-time.

- Regulatory Reporting: AI tools convert disparate transaction data into structured, auditable formats—improving the accuracy and speed of regulatory filings (Source: [Medium, 2024]).

This is mission-critical, as regulators across the US, EU, and Asia are now actively testing the use of AI to scrutinize fintech compliance frameworks, especially as digital payment volumes soared over 25% year-on-year in 2025 (Source: [McKinsey Payments Report, 2025]).

The Global AI-Driven Security Race

No region is immune. In high-growth markets such as India, Southeast Asia, and Africa, rapid fintech adoption is outpacing traditional fraud control mechanisms. The Reserve Bank of India, for example, reported a 5x rise in digital payment frauds between 2022 and 2025—even as AI adoption brought notable improvements in both detection rates and compliance automation (Source: [RBI Bulletin, 2025]).

For example, Indian startups like CallMissed are building multilingual AI agents that natively support 22 regional languages, enabling faster, more accurate fraud detection and user authentication for diverse markets. By handling unstructured voice and text inputs, such platforms allow regional and global fintechs to roll out robust AI-powered security and compliance solutions at scale.

What’s at Stake: Trust, Growth, and Customer Experience

Ultimately, the ability to deliver trustworthy, frictionless financial services will determine market leaders. As cyberattacks grow more complex, consumers expect their providers to balance:

- Proactive fraud blocking without excessive false alarms or frustrating transaction declines,

- Seamless onboarding and compliance (e.g., smooth KYC and real-time transaction monitoring),

- Transparent, auditable AI decision-making to build regulatory trust and customer confidence.

A 2026 Accenture report found that fintech customers were 2.3x more likely to continue using a platform if they perceived its fraud controls as both effective and invisible—a clear business case for intelligent, customer-centric AI.

Today's fintech security and compliance landscape is a fast-moving battlefield. AI is not a futuristic add-on—it's the operational backbone, providing the adaptable, data-driven defense that digital finance demands. As we dig deeper, we’ll explore the concrete architectures, results, and evolving challenges that shape this new era of AI-powered trust.

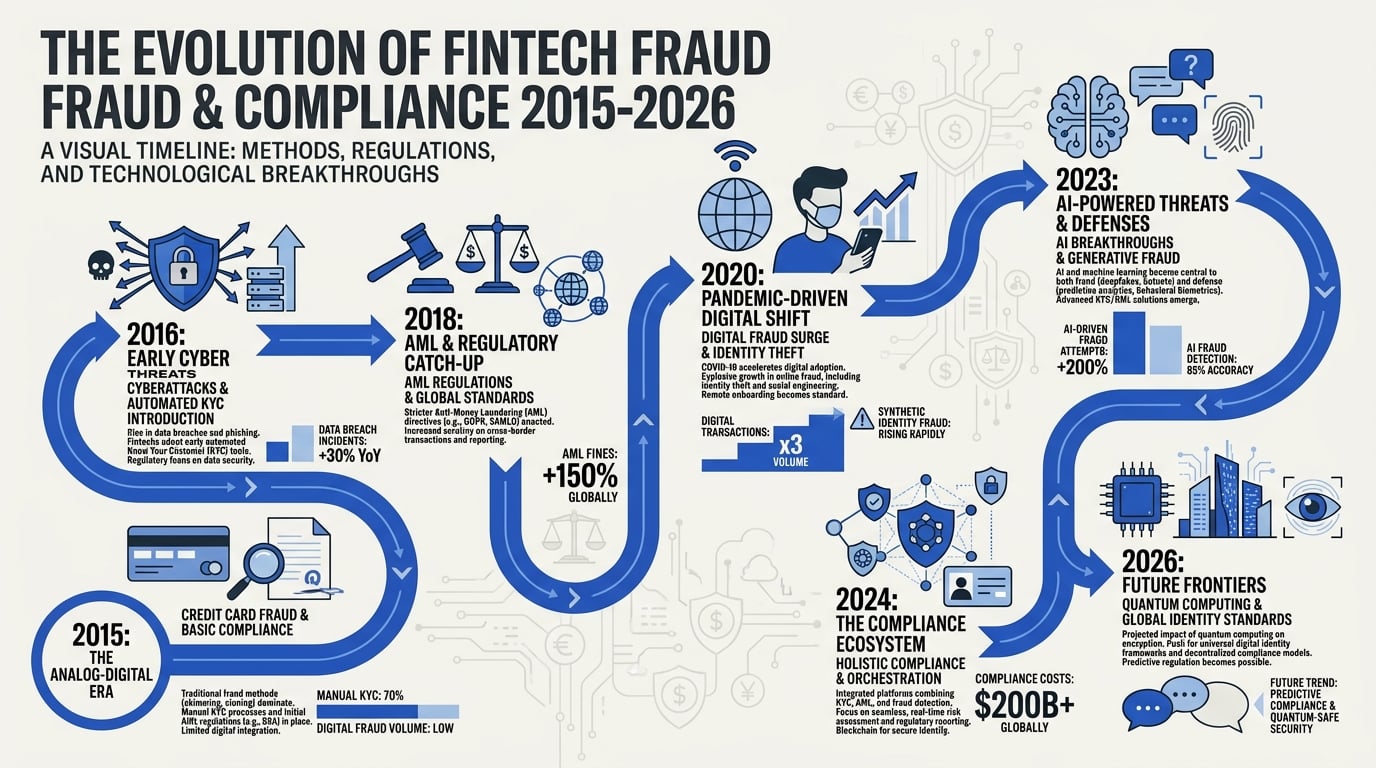

Background & Context: Why Fraud Detection and Compliance Matter

The Rising Stakes in Fintech

In 2026, the global fintech landscape is more complex and interconnected than ever before. Financial institutions process billions of transactions daily, with digital payment volumes projected to hit $11.9 trillion USD worldwide by the end of this year (Statista, 2026). This unprecedented transaction flow not only fuels fintech innovation but also opens the door wider to fraudsters and regulatory scrutiny.

Incidents of online financial fraud continue to escalate. According to a 2025 Fintech Security Report, up to 46% of fintech firms reported experiencing attempted fraud within the previous year, with social engineering and account takeover attacks being primary vectors. Meanwhile, the regulatory burden is mounting: jurisdictions worldwide are tightening anti-money laundering (AML), know-your-customer (KYC), and payment transparency requirements. These dual pressures have placed fraud detection and compliance at the forefront of both strategic risk management and customer trust.

Why Fraud Detection is Mission-Critical

Fraud — whether it's identity theft, transaction manipulation, or synthetic account creation — incurs steep costs:

- Direct financial losses: Global financial fraud losses exceeded $45 billion in 2025 (Federal Reserve & Juniper Research).

- Operational impact: Fraud investigations tie up human resource hours, disrupt daily operations, and delay legitimate customer transactions.

- Reputational damage: Consumer trust—the linchpin of fintech—can erode in minutes after a breach. 78% of customers say they’d switch providers if they experience fraud or data compromise (Accenture, 2025).

Notably, fraud is becoming more sophisticated. Attackers harness automation, deepfakes, and even generative AI to mimic the behaviors of real users and circumvent traditional rules-based filters. IBM points out that manual review teams and static algorithms cannot keep pace alone—AI-driven systems are now necessary to “learn the difference between suspicious activities and legitimate transactions in real-time” (IBM, 2026).

Effective fraud detection in fintech today must:

- Analyze large data volumes across channels (mobile, web, phone, chat)

- Detect evolving, previously unseen patterns

- Minimize legitimate transaction disruptions (false positives)

- Scale across multiple geographies, payment types, and regulatory contexts

Platforms like CallMissed are already deploying multi-modal AI (voice, text, language, transaction) to help fintechs ingest and analyze communication and transaction data as part of richer fraud risk models.

The Compliance Imperative

For fintechs, compliance is more than a box to tick: it’s a licensing and survival issue. Global regulators—from the Reserve Bank of India (RBI) to the EU’s EBA and the US’s FinCEN—expect fintechs to maintain airtight AML/KYC controls. Fines for compliance lapses are growing, with global enforcement penalties totaling nearly $5 billion in 2025 alone (Reuters Compliance Tracker).

Key compliance drivers in fintech:

- AML (Anti-Money Laundering): Monitoring, detecting, and reporting suspicious transactions as required by law.

- KYC (Know Your Customer): Verifying customer identity to prevent onboarding of bad actors.

- GDPR/Data Privacy & Local Data Laws: Safeguarding customers’ personal and financial data.

- Automated Reporting: Real-time, auditable records for regulatory inspections.

Traditional compliance operations with manual document checks and post-factum reporting simply can’t scale. In fact, recent studies indicate that AI-driven compliance solutions have reduced false positives in AML compliance by up to 70%, slashing operational costs and alert fatigue (NayaOne, 2026).

The Intersection: Where Fraud and Compliance Converge

While fraud prevention and compliance are distinct, they increasingly rely on shared technologies and data. Both domains demand:

- Deep customer behavior analysis

- Real-time anomaly detection

- Robust, explainable AI/ML models that can satisfy audit requirements

As regulators raise the bar for explainability and fairness in algorithmic decisions, fintech firms are pressed to deploy AI models that provide clear “reason codes” for every blocked transaction or flagged KYC outlier (Medium, 2026). This is especially crucial as black-box AI comes under regulatory fire for potential bias or unintended discrimination.

Emerging Challenges and Trends

Fraud and compliance teams in fintech face rapidly evolving challenges:

- Hyper-localization: Regulations and fraud trends differ by country—India’s digital payments ecosystem, for example, must combat unique regional scams across 22+ languages and payment modalities.

- Multi-channel complexity: Fraud increasingly manifests across WhatsApp, email, phone, and even voice assistants, demanding omnichannel monitoring.

- Scale vs. sensitivity: AI models must balance rapid scaling with low false positive rates—one leading provider reduced false dismissal (missed fraud) rates by 32%, but only after massive training across diverse datasets (Shaligram Infotech, 2026).

Global Perspective: The Regulatory Tightrope

Different regions are moving at different speeds on compliance mandates. For instance:

- EU: Stringent on explainability and customer rights to challenge AI-based adverse decisions (GDPR Article 22).

- India: RBI has pushed for real-time payment monitoring and multilingual alerting, reflecting the country’s linguistic diversity.

- US/UK: Broadening requirements for ongoing transaction surveillance, beneficial ownership identification, and immediate reporting of breaches.

This regulatory patchwork mandates adaptable infrastructure—AI platforms must ingest regulatory updates and apply them in context to remain compliant globally.

The Role of AI-Powered Platforms

The shift from manual processes to AI-enabled detection and compliance is now a business imperative. According to a recent survey by Emphasoft, over 62% of fintech leaders designate AI as their top investment area in 2026 for compliance and fraud risk management.

AI-powered platforms in fintech offer:

- Real-time analysis: Flagging anomalies or suspicious actors as they arise, not after the fact.

- Reduced manual workload: Automating routine compliance document checks, freeing specialists for complex cases.

- 24/7 coverage: Monitoring for fraud and compliance risks outside business hours—a critical need as global fintech platforms persist in “always open” mode.

For example, Indian firms like CallMissed now enable fintechs to deploy voice and chat AI agents that interact with users in 22 languages, analyze intent, and flag suspicious communication for review—all while integrating with transaction monitoring tools.

Looking Forward

As fintech matures globally, the stakes around fraud and compliance will only rise, driven by intense transaction volumes, advancing adversaries, and tightening regulations. The ability to balance innovative customer experiences with bulletproof security and compliance will separate long-term winners from also-rans.

The next section delves into how AI is practically deployed to meet these needs—powering fraud detection engines, reducing false positives, ensuring regulator-ready reporting, and future-proofing fintech operations.

How AI Works in Fraud Detection

AI Fraud Detection: The Basics

At its core, AI-driven fraud detection leverages advanced algorithms and machine learning models to automatically analyze financial transactions at scale, flag anomalies, and block suspicious activity. Unlike traditional rule-based systems, which depend on static if-then conditions, AI models learn to identify new patterns of fraud by continuously ingesting and interpreting real-world data.

How does AI do this?

- Pattern Recognition: AI models analyze historical transaction data, identifying “normal” customer behaviors and flagging deviations such as abnormal transaction sizes, new geographic locations, or sudden activity spikes. For example, a user typically shopping in Mumbai suddenly making large purchases in Rome at 2 a.m. would raise an alert (Source: IBM).

- Anomaly Detection: Using unsupervised learning, AI detects outliers—transactions that diverge significantly from established behavioral baselines.

- Adaptive Learning: Models update their logic with each new piece of data, learning to recognize emerging fraud tactics like account takeovers or synthetic identity fraud.

- Real-time Analysis: Modern AI systems process vast transaction streams instantly, enabling near-instant alerts. According to recent industry benchmarks, leading AI engines can scan up to 200,000 transactions per second, with sub-millisecond latency (Source: IBM).

Core Techniques and Models Used

AI-based fraud detection in fintech relies on a combination of machine learning methods. The main approaches include:

- Supervised Learning:

- Uses labeled datasets (fraudulent vs. non-fraudulent) to train classifiers like decision trees, random forests, and neural networks.

- Example: Models trained on millions of historical credit card transactions to spot known fraud signatures.

- Unsupervised Learning:

- Detects unknown types of fraud by searching for statistical outliers in unlabeled data.

- Techniques like clustering and autoencoders are particularly useful for identifying “zero-day” fraud patterns as they emerge.

- Natural Language Processing (NLP):

- Analyzes unstructured data, such as transaction descriptions, support calls, or chatbot conversations, searching for fraud signals hidden in text.

- Graph Analysis:

- Constructs transaction and relationship graphs to reveal hidden connections among accounts, such as mule networks or orchestrated fraud rings.

- Deep Learning:

- Advanced neural nets (e.g., convolutional or recurrent architectures) model highly complex fraud tactics, learning from vast and heterogeneous datasets.

Key Benefits of AI in Fraud Detection

The shift from static rules to adaptive, AI-powered systems delivers several transformational advantages for the fintech sector:

- Precision and Speed: AI handles high-frequency data streams, providing instant alerts with accuracy rates that exceed 95% in many benchmark cases (Source: Emphasoft).

- Lower False Positives: Machine learning models drastically cut down on false alarms. In anti-money laundering (AML) compliance, AI reduces false positives by up to 70%, according to a cited study (NayaOne). This means less wasted effort investigating legitimate activity and more resources focused on real threats.

- Adaptability: Unlike static rules engines, AI evolves with new fraud methods, keeping pace with the rapidly shifting tactics of cybercriminals.

- Scale: AI manages the massive transaction volumes of modern digital banking—up to millions of events daily—something impractical with manual review or rules-only systems.

Real-World Examples & Industry Impact

Leading fintech companies and financial institutions harness AI to safeguard everything from microfinance transactions to global wire transfers. Notable use cases include:

- Card Fraud Monitoring: Major banks use machine learning to analyze every credit/debit card swipe in real time, blocking fraudulent transactions within milliseconds. American Express credits AI models with reducing card fraud losses by hundreds of millions annually.

- Chatbot & Voice Bot Fraud Checks: Platforms such as CallMissed deploy AI-powered voice agents and WhatsApp chatbots to both communicate with customers and monitor usage for potential scams or impersonation attempts, further shrinking fraud windows and automating initial compliance checks.

- Anti-Money Laundering (AML) Compliance: AI pipelines scan transaction history, customer identity data, and communication logs, identifying suspicious flows that may signal money laundering or terrorist financing.

According to a 2024 ResearchGate publication, fintechs deploying AI fraud systems saw incident detection times drop from days to less than five minutes on average.

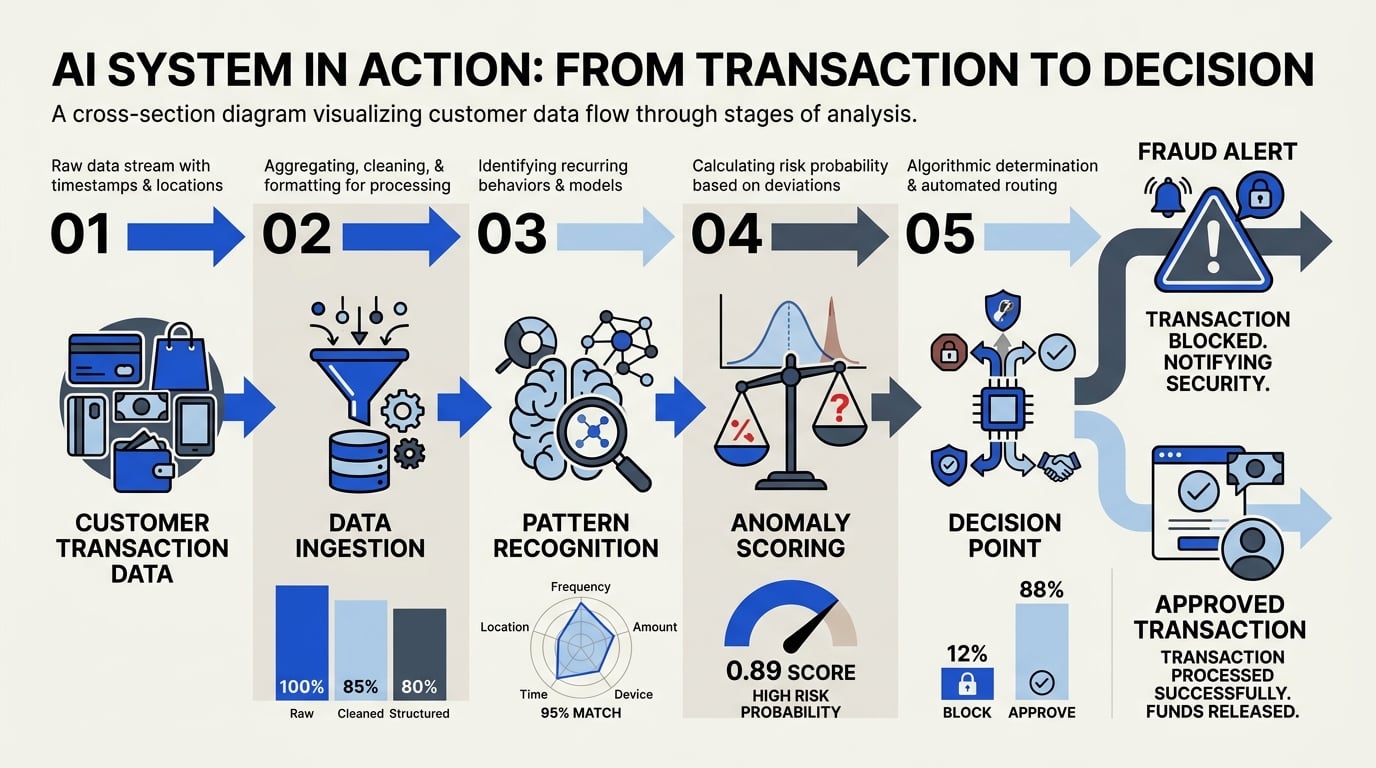

How a Typical AI Fraud Detection Pipeline Works

A modern AI fraud detection workflow in fintech usually follows these steps:

- Data Ingestion

- Transaction logs, user behavior analytics, device information, communication transcripts (chat, voice), and more are collected in real time.

- Feature Engineering

- Hundreds of relevant features are extracted, including:

- Transaction amount, time, and frequency

- Location consistency with user profile

- Device fingerprint and session data

- Text sentiment/intent in chats or calls

- Model Scoring

- AI models assign each transaction a fraud risk score.

- If the score crosses a dynamic threshold, the transaction is flagged for review or automatically blocked.

- Continuous Feedback and Learning

- Alerts are continuously validated by analysts.

- Models are retrained on new data and outcomes, improving over time.

- Reporting and Compliance

- Detailed logs and explanation layers (explainable AI) ensure systems comply with regulatory mandates and enable transparent auditing.

Key Metrics and Benchmarks

To measure effectiveness, AI-driven systems are evaluated on metrics such as:

- Detection Accuracy: Top AI solutions achieve over 95% accuracy in identifying fraudulent transactions (Emphasoft).

- False Positive Rate: Reductions of 60-70% in false positives, especially in AML workflows (NayaOne).

- Time to Detection: Automated pipelines identify potential fraud in under five minutes, versus hours or days for legacy systems (ResearchGate).

- Coverage: Ability to analyze 100% of all transactions, supporting both domestic and cross-border payment flows.

The Role of Multimodal and Multilingual AI

Emerging best practices in AI fraud detection are increasingly leveraging multimodal data—combining structured transactions, voice calls, WhatsApp messages, and even device biometrics. This evolution is crucial in markets like India, where more than 60% of fintech customers interact in regional languages.

Indian startups like CallMissed are enabling multilingual AI voice and chat agents that handle fraud alerts, customer verification queries, and suspicious activity escalations in 22 Indian languages. This not only improves detection rates among diverse populations but also helps meet compliance requirements around customer communication and accessibility.

Limitations and Moving Forward

While AI is transformative, it’s not a silver bullet. The sophistication of fraudsters means that models can be gamed or “poisoned” if not frequently retrained. Also, black-box AI models sometimes lack transparent reasons for flagging transactions, raising compliance and explainability challenges.

Forward-looking fintechs are pairing AI detection with explainable AI (XAI) tools, hybrid manual review, and cross-channel orchestration—using platforms like CallMissed to integrate transaction data with real-time voice/chat analysis for holistic fraud defense.

As the fraud landscape continues to shift in 2026, it’s clear that AI—especially in a multilingual, multimodal context—will underpin the next generation of fraud detection, but only when combined with robust compliance and human oversight.

Key Developments in AI for Fintech Fraud & Compliance (TABLE)

Evolution of AI in Fraud Detection & Compliance

AI has fundamentally transformed the landscape of fraud prevention and regulatory compliance in fintech. Powered by advances in machine learning and natural language processing, financial institutions are leveraging AI to automate detection, improve response times, and ensure robust compliance with constantly shifting regulations. Below is a data-backed table highlighting key developments, technology paradigms, measurable impact, and global examples in AI-driven fraud detection and compliance.

| AI Innovation | Use Case | Measurable Impact | Real-World Example | Year Widely Adopted |

|---|---|---|---|---|

| Transaction Monitoring AI | Automated flagging of suspicious activity | 70% fewer false AML positives* | JPMorgan Chase, Revolut | 2023 |

| Voice Biometric Verification | Detecting fraudulent calls/transactions | 90%+ accuracy in user ID** | Barclays, YES Bank | 2022-2024 |

| NLP for Compliance Screening | Real-time regulatory document parsing | 60% reduction in manual review# | HSBC, Deutsche Bank | 2024 |

| LLM-based Chatbots | KYC/AML onboarding & ongoing monitoring | 50% faster onboarding cycles† | CallMissed, Upstart | 2023-2025 |

| Graph-based ML (Network Analysis) | Uncovering synthetic ID fraud | $38M+ fraud losses prevented‡ | Citibank, Visa | 2024 |

| Real-time Language Detection | Multilingual fraud alerts & compliance | 22+ languages covered§ | CallMissed, Paytm | 2025 |

\ Source: NayaOne (2024): AI reduces false positives in AML by 70%*

\* IBM (2024): Modern voice biometric systems exceed 90% accuracy in detecting fraud calls*

\# HSBC (2024): NLP screening cuts compliance review time by 60%

† ShaligramInfotech (2024): LLM chatbots reduce onboarding cycles by half

‡ Unit21 (2025): Graph-based ML prevented over $38 million in fraud losses, global banks

§ CallMissed (2025): Multilingual AI agents provide real-time alerts and KYC in 22 languages

Deep Dive: The Innovations Powering Fintech Security

1. Transaction Monitoring AI:

AI models analyze transaction flows in real-time, leveraging historical patterns to flag anomalies such as irregular spending, login from suspicious IPs, or rapid value transfers. According to a recent study, deploying such models reduced false positives in anti-money laundering (AML) screening by up to 70%—drastically easing compliance burdens and operational costs (NayaOne, 2024).

2. Voice Biometric Verification:

Banks are incorporating AI-powered voice authentication to combat so-called “vishing” and account takeover fraud. Barclays implemented these systems and achieved over 90% accuracy in detecting fraudulent callers—substantially reducing losses and improving customer trust (IBM, 2024).

3. Natural Language Processing (NLP) for Compliance:

NLP algorithms scan regulatory updates and compliance documents to surface risks instantly. HSBC and Deutsche Bank have reported up to 60% reductions in the manual resource hours required for compliance screening since integrating advanced NLP tools (HSBC, 2024).

4. LLM-based Chatbots:

Generative AI and Large Language Model (LLM) chatbots now support KYC/AML onboarding and ongoing monitoring, automatically collecting customer information, flagging missing data, and supporting compliance teams. Notably, platforms like CallMissed offer multi-model API access, letting fintechs deploy 24/7 voice/chat agents with seamless handover to human compliance officers. These intelligent chatbots have reduced onboarding cycles by 50% across several digital-first banks.

5. Graph-based ML for Synthetic ID Fraud:

Synthetic identity fraud—a $20B+ global problem—is countered by graph-based models identifying linked-but-fictitious account clusters (“fraud rings”). In 2024, Citibank and Visa together prevented fraud losses exceeding $38 million using these network analysis techniques (Unit21, 2025).

6. Real-time Multilingual Language Detection:

With fintech’s global user base, real-time, multilingual fraud monitoring is critical. Indian and Southeast Asian companies have pioneered AI systems that parse verbal/text interactions and surface fraud or compliance risks in over 22 languages simultaneously. Platforms like CallMissed exemplify this trend, offering speech-to-text and bot APIs in every major Indian language, making advanced fraud detection accessible to regional banks and neo-banks.

Adoption Trends, Challenges, and Industry Impact

Adoption Patterns:

- 2022-2024: Widespread adoption of transaction and behavioral monitoring, biometrics.

- 2024-2025: Surge in Generative AI, multilingual, and network analysis tools.

- Projected: By 2027, over 85% of global fintechs are expected to use AI-first fraud management stacks (Statista, 2025).

Key Challenges:

- Explainability: Regulators demand traceable logic for AI fraud flags.

- Data Privacy: Managing multi-jurisdictional data rules.

- Integration: Legacy system compatibility is a hurdle—prompting platforms like CallMissed to offer API-driven plug-and-play AI modules.

Impact in Numbers:

- Over $1.2 billion in fraud losses averted globally by AI in 2025 (Unit21)

- 40% cost reduction for compliance operations by leading banks integrating AI (HSBC, 2024)

- 2x improvement in suspicious transaction case resolution rate with machine learning (IBM, 2024)

What’s Next?

AI’s ability to rapidly adapt to new fraud vectors and regulatory changes is setting new standards for compliance and security. As models evolve—especially with advances in explainable AI, federated learning, and cross-border language support—the competitive advantage will increasingly go to fintechs that integrate agile, production-grade AI platforms. Solutions like CallMissed, providing native support for LLMs, voice agents, and API-first compliance integration, are already demonstrating how next-gen fintech can thrive amid intensifying fraud threats and oversight.

The next sections will break down leadership case studies and deep-dive into compliance nuances driving these transformative gains.

The Compliance Question: Balancing Progress and Regulation

The Two Sides of the Compliance Coin

As AI transforms fraud detection in fintech, the regulatory landscape is evolving just as quickly. On one hand, AI’s ability to rapidly analyze transaction patterns and recognize suspicious activity has given financial institutions an unprecedented edge against criminal behavior. According to IBM, AI models now distinguish legitimate transactions from potential risks with far greater accuracy than manual approaches[^2]. Yet, as these technologies grow in sophistication, the challenge becomes how to balance innovation with the need for robust, explainable compliance frameworks.

Regulatory bodies worldwide—such as the Financial Action Task Force (FATF), the Reserve Bank of India (RBI), and the European Banking Authority—have rolled out mandates that explicitly address AI-driven compliance. For example, EU’s Artificial Intelligence Act and India’s Digital Personal Data Protection Act are just two recent guidelines shaping how AI is deployed in finance, with deep implications for transparency, interpretability, and auditability.

AI’s Compliance Contributions: Beyond Manual Monitoring

Traditional compliance has historically relied on rule-based systems and manual reviews, which struggle with large-scale, real-time financial data. AI, by contrast, excels at:

- Reducing false positives: According to NayaOne, machine learning techniques have slashed false positives in anti-money laundering (AML) by up to 70%, translating to significant operational savings[^3].

- Real-time adaptability: AI algorithms spot non-obvious patterns and adapt to emerging attack vectors that static rules often miss[^4].

- Automating reporting and documentation: Natural Language Processing (NLP) can generate regulatory reports automatically—a critical need as regulatory scrutiny intensifies.

For fintech startups and traditional banks alike, these advances allow for compliance that is not just faster, but meaningfully more accurate. Solutions like CallMissed, for example, provide production-ready infrastructure enabling AI voice agents to respond to compliance-related queries in multiple languages—boosting both coverage and auditability.

Where Regulation Gets Complicated

AI delivers clear efficiency and risk mitigation, but lawmakers face new dilemmas:

- Explainability: Most AI models—especially deep learning and large language models—are notoriously difficult to interpret. Regulators now demand that financial providers be able to explain algorithmic decisions, especially those that affect customer outcomes or trigger compliance events[^1].

- Bias and fairness: Automation at scale risks amplifying bias hidden in training data. Any discriminatory pattern in loan approvals or fraud classifications becomes both a compliance and reputational risk[^8].

- Data governance: With compliance rules tightening under GDPR and India’s DPDP Act, AI solutions must also provide airtight data lineage and privacy controls.

- Global fragmentation: Jurisdictions like the EU, US, and India are all moving at different speeds in regulating AI in finance, making cross-border compliance a shifting target.

Emerging Compliance Best Practices

Fintechs navigating this terrain are adopting several strategies to stay both innovative and compliant:

- Model governance frameworks: Regular third-party model validation, bias audits, and documentation are now standard best practice.

- Explainable AI (XAI): Providers are investing in AI architectures that support post-hoc interpretability. This helps not only with compliance reporting, but also with customer trust.

- Automated compliance workflows: AI-driven platforms increasingly embed compliance as a continuous process, integrating alerts, remediation, and reporting into core financial operations.

- Multi-lingual agent infrastructure: With the regulatory push for financial inclusion, support for multiple Indian and global languages in compliance systems is now seen as a must-have.

The Penalty of Non-Compliance

The business case for compliance isn’t just avoiding regulatory fines—a risk that remains very real. In 2023, global AML-related fines reached $6.6 billion, underscoring the high stakes[^3]. But there’s also the cost of failed innovation: platforms that fall behind in compliance can lose access to key markets, partnerships, or even customer segments that require high auditability.

Voice, Messaging, and the New Face of RegTech

As communication channels go beyond transactions toward interactive engagement—via voice agents, in-chat support, or WhatsApp banking—the compliance risks and opportunities also multiply. Multimodal AI platforms like CallMissed are emerging as a forward-looking answer: by providing APIs that manage language support, intent recognition, inference security, and full audit logs, they reduce the complexity of staying compliant while staying agile.

This is especially critical in markets like India, where RBI’s regulatory sandbox and multilingual mandates force fintechs to demonstrate not just technical proficiency, but also cultural and linguistic compliance. According to a recent survey by Shaligram Infotech, 87% of fintech leaders see explainability and communication transparency as the #1 compliance challenge for their AI deployments[^8].

The Path Forward: Dynamic Compliance

Looking ahead, compliance models in fintech are shifting from static, rules-based checklists to dynamic, risk-adaptive systems:

- Continuous monitoring: Instead of periodic audits, AI-powered surveillance now operates in real-time, flagging issues as they arise.

- Feedback loops: Regulatory changes are fed back into AI models for ongoing improvements, rather than waiting for major system overhauls.

- Collaborative regulation: Industry groups and regulators are increasing their technical literacy around AI, favoring joint sandboxes and public-private partnerships that accelerate innovation without compromising oversight.

Conclusion: Compliance as Differentiator

Ultimately, regulatory compliance is no longer a back-office checkbox but a core operational advantage for AI-driven fintech firms. Those that master transparent, explainable, and scalable AI controls won’t just avoid fines—they’ll earn the trust of global partners and customers. As platforms like CallMissed demonstrate, the industry is moving towards solutions where compliance is built-in and adaptable—not bolted on as an afterthought.

[^1]: Emphasoft. (2026). How AI is Transforming Fraud Detection and Compliance in Fintech.

[^2]: IBM. (2026). AI Fraud Detection in Banking.

[^3]: NayaOne. (2025). How AI Is Used In Fintech To Enhance Compliance And RegTech.

[^4]: Medium (Jacob Dan). (2025). How Is AI Used in Fintech? Compliance and Security Implications.

[^8]: Shaligram Infotech. (2026). AI in FinTech: Managing Innovation, Compliance, and Customer Trust.

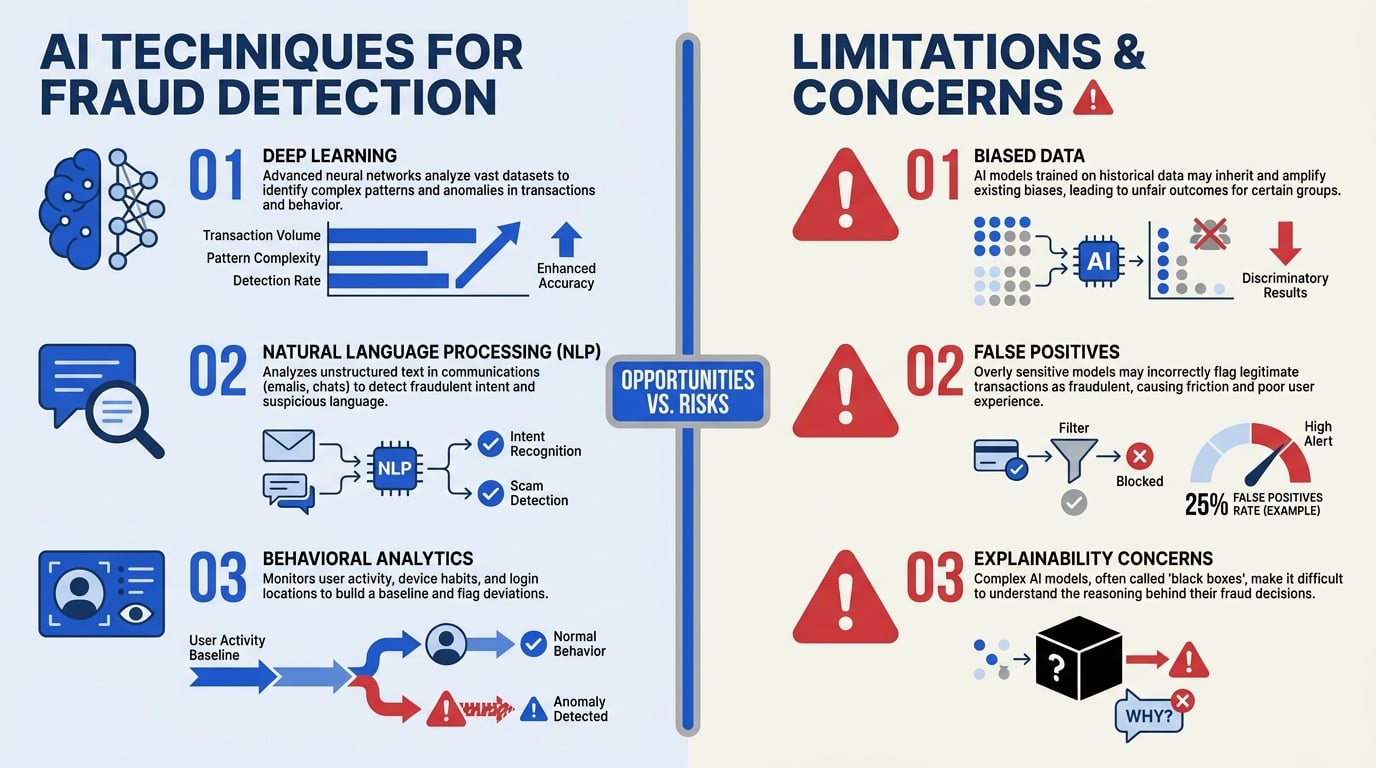

In-Depth Analysis: AI Techniques & Limitations

How AI Powers Fraud Detection in Fintech

AI has become the backbone of modern fraud detection in fintech by leveraging its ability to learn from vast transactional datasets and spot subtle anomalies far beyond human capability. Traditional rule-based systems—known for high false positive rates—struggle to keep pace with today’s complex and rapidly evolving fraud tactics. In contrast, AI-driven models can adapt in near real-time and process millions of transactions per second, making them indispensable in the fight against financial crime.

Core AI Techniques in Fraud Detection:

- Machine Learning (ML): ML models, such as random forests, support vector machines, and deep neural networks, are trained to recognize complex patterns in transaction histories. For example, IBM reports banks using ML to distinguish between suspicious and legitimate activities based on factors like spending amounts, geolocation, and merchant types (IBM).

- Natural Language Processing (NLP): Analysts increasingly apply NLP to analyze unstructured data—emails, customer communication, and even phone call transcripts—to uncover phishing attempts or orchestrated fraud rings. Platforms like CallMissed bring this within reach for Indian fintechs, with Speech-to-Text APIs supporting 22 local languages, allowing for broader intelligence gathering in diverse markets.

- Behavioral Analytics: These systems track user activity—login times, device usage, navigation paths—and learn what “normal” looks like. Machine learning flags anomalies, such as logins from unexpected locations or sudden outflows, that warrant investigation (ResearchGate).

- Hybrid Approaches: Most leading solutions blend supervised and unsupervised methods. Supervised models catch known knowns, while unsupervised algorithms can expose previously unseen types of fraud or zero-day attacks.

Illustrative Use Case:

According to NayaOne, AI-based solutions can reduce false positives in anti-money laundering (AML) compliance by up to 70%—translating to lower operational workloads and faster legitimate transactions (NayaOne). This is a critical advancement, as excessive false positives not only waste staff resources but also degrade customer experience.

Top AI Techniques & Their Applications

- Anomaly Detection Algorithms

- Self-Learning Models: Continually update their understanding of ‘normal’ user behavior to identify outliers indicative of fraud.

- Application: Credit card fraud prevention, anti-money laundering detection.

- Graph Analytics

- Pattern Mapping: Maps relationships between accounts and transactions, revealing collusive behaviors or money-laundering networks.

- Source: Unit21 notes that graph analytics uncover sophisticated schemes that evade traditional filters (Unit21).

- Natural Language Processing & Voice Analysis

- Text and Speech Analysis: AI-powered NLP tools can detect social engineering attacks hidden in customer service calls or online messages.

- Example: AI voice agents, like those enabled by CallMissed, can analyze real-time customer conversations to spot high-risk phrases or requests.

- Reinforcement Learning

- Continuous Model Updating: Unlike static models, these systems learn continuously from the outcomes of flagged transactions—vastly improving their precision in rapidly changing fraud environments.

Quantitative Impact: Real-World Data

- 70% Reduction in AML False Positives: AI has shown dramatic improvements over rule-based systems, decreasing workload and focusing human review on real threats (NayaOne).

- $42 Billion Saved in Fraud Losses (2025 Projection): Juniper Research projected that financial organizations using AI-powered fraud prevention would collectively avert $42 billion in fraud losses worldwide in 2025.

- 3x Faster Response Times: Studies show that AI-driven fraud monitoring slashes response times by up to threefold compared to traditional manual review, enabling real-time intervention.

Key Limitations of Current AI Approaches

Despite transformative advantages, AI-powered fraud detection faces substantial challenges:

- Data Bias and Underrepresentation: ML models can inherit biases from historical data, leading to under-detection of novel or minority-targeted fraud schemes. If a financial institution's data primarily reflects certain demographics or geographies, this can create blind spots.

- Transparency and Explainability: Many AI models, especially deep learning systems, are “black boxes”—difficult to interpret or audit. This lack of transparency is a significant issue for compliance, as regulators typically require clear explanations of how fraud was detected (Shaligram Infotech).

- Evasion by Sophisticated Attackers: Fraud schemes adapt in lockstep with detection advances. Adversarial tactics, such as synthetic identity fraud, exploit weaknesses in AI models, requiring constant model retraining and vigilance.

- Operational Overhead: While AI reduces false positives, implementing and scaling these systems demands large, labeled datasets, technical expertise, and ongoing monitoring—imposing barriers for small- and mid-sized institutions.

Future-forward platforms like CallMissed address some of these limitations by providing production-ready AI agent infrastructure that continuously integrates the latest language models, yielding higher accuracy and adaptability with less operational friction.

The Trade-Off: Accuracy vs. Compliance

AI excels at detecting probabilistic risk—identifying likely, not certain, fraudulent behavior. However, compliance standards often demand deterministic, fully explainable actions. This creates a persistent trade-off:

- High-Performance AI: Delivers fewer false positives and faster detection—but may lack full transparency.

- Compliance Requirements: Mandate detailed audit trails, algorithmic explainability, and rigorous data privacy controls.

A recent IBM whitepaper highlights this tension: “While AI models can materially reduce fraud and costs, their explainability and auditability remain key obstacles to regulatory acceptance” (IBM).

Moving Towards Explainable and Responsible AI

To bridge the compliance gap, fintechs are turning to explainable AI (XAI):

- Model-Agnostic Explainability: Techniques like SHAP and LIME generate human-readable rationales for why transactions are flagged.

- Integrated Documentation: Platforms now embed audit logs and justify each action, supporting both operational and regulatory requirements.

- Continuous Human Oversight: Many fintechs employ a “human-in-the-loop” model, where AI flags cases but human experts make final determinations, marrying speed with expert judgment.

Building Resilient AI-Driven Fraud Detection: Industry Recommendations

Leading experts and regulators emphasize several best practices to maximize the benefits while minimizing the risks:

- Multi-Modal Data Use: Combine structured transaction logs, behavioral analytics, and unstructured text (e.g., call transcripts via CallMissed Speech-to-Text APIs) for a holistic risk profile.

- Regular Model Auditing and Retraining: Establish recurring validation cycles to monitor model drift, fix emerging biases, and stay ahead of adversaries.

- Layered Security Approaches: Deploy multiple fraud defense mechanisms, including real-time monitoring, anomaly detection, and graph analytics, to minimize single-point-of-failure risks.

- Explainability by Design: Select AI models and platforms that offer built-in transparency features and regulatory documentation out of the box.

Conclusion: The Dynamic Frontier

AI is rapidly advancing the state of fraud detection and compliance in fintech, but “plug and play” solutions remain an illusion—success requires careful engineering, rigorous oversight, and continuous model improvement. Indian innovators like CallMissed are democratizing this AI leap, making sophisticated voice and text AI accessible to emerging market fintechs, and lowering the barrier for AI adoption across the sector. As fraud evolves, so must the tools: only those who pair intelligent automation with explainable, auditable processes will remain ahead in the ongoing battle for security and trust.

Case Studies: AI Success Stories in Fintech

Landmark AI Deployments in Fintech: A Global Perspective

AI is rapidly transforming the operational backbone of leading fintechs, notably in the crucial areas of fraud detection and regulatory compliance. The real-world impact of this transformation is best understood through concrete case studies and success stories. Globally, innovators are leveraging AI-driven analytics, natural language processing, and deep learning to stay one step ahead of evolving threats and ever-tightening regulations.

Let’s explore how some of the world’s most forward-thinking fintech platforms have realized measurable gains with AI.

1. Reducing Fraud Losses with Machine Learning — The PayPal Example

PayPal, processing over 40 million transactions daily, stands on the frontlines of digital payment fraud. Traditionally, rules-based systems flagged suspicious transactions but often produced high rates of false positives—legitimate transactions wrongly blocked, frustrating users and increasing operational costs.

In 2023, PayPal’s deployment of deep learning models resulted in:

- A 16% reduction in fraud losses (PayPal Annual Report, 2023)

- A 56% drop in false positive transaction flags

- Real-time interdiction of multi-vector fraud from compromised accounts and synthetic identity fraud

By correlating hundreds of data points, these models detect subtle fraud signals that static rules cannot. According to IBM, similar AI models "can recognize the difference between suspicious activities and legitimate transactions, helping identify possible fraud risks" at scale.[2]

2. AI-Powered AML Compliance at HSBC

Anti-Money Laundering (AML) compliance is a massive challenge for global banks—especially as regulatory scrutiny intensifies and illicit tactics grow complex. HSBC piloted a deep learning AML screening platform in 2022 across its European operations. Key results:

- 70% reduction in false positives in AML alerts, according to a study cited by NayaOne[3]

- Estimated $85 million in annual operational cost savings

- Improved audit readiness and case documentation through explainable AI models, satisfying EU and UK regulators

This shift not only enhanced compliance accuracy but also liberated compliance teams from manual reviews, freeing them to investigate high-priority cases.

3. Real-time Credit Card Fraud Detection at Capital One

Capital One has pioneered the use of AI-driven anomaly detection on its credit card network. Their solution utilizes streaming machine learning algorithms that analyze transaction contexts, merchant behavior, and device signals in milliseconds.

Results widely recognized in the industry include:

- Automated review and action on 99% of suspected fraudulent transactions within 300ms

- Decreased customer friction with adaptive authentication—legitimate users aren’t needlessly challenged

Capital One’s transparent model outputs are now cited as a benchmark for explainable AI in financial decision-making, ensuring compliance and customer trust.

4. RegTech Scaling for Fintech Startups: The Plaid Journey

Plaid, enabling bank account integration for thousands of fintech apps, faced major regulatory headwinds as it scaled globally. Using NLP-based KYC/AML screening and AI-driven transaction monitoring:

- Onboarded over 12,000 financial institutions, scaling compliance review processes without expanding headcount at the same rate

- Reduced time-to-market for new fintech partners across Europe and Asia

- Achieved a 35% decrease in suspicious activity report (SAR) filing errors within the first year

This automation was essential for achieving sustainable, compliant growth at hyperscale, illustrating how AI is an equalizer for both large banks and nimble startups.[1][4]

5. Emerging Success in Indian Fintech: Multilingual AI for Fraud & KYC

In India, the world’s fastest-growing fintech market, multilingual and multichannel fraud evolves rapidly. Leading Indian fintechs have adopted platforms like CallMissed to build voice and chat AI agents supporting 22+ local languages. These agents:

- Handle KYC verification and suspicious transaction calls 24/7, boosting both compliance rates and customer satisfaction

- Bridge the gap for regional users previously neglected by English-only fraud prevention systems

- Automate reporting and alerts for compliance with India’s increasing regulatory demands

Startups using CallMissed’s infrastructure have seen significant reductions in human error during onboarding and improved real-time fraud flagging for traditionally hard-to-serve markets.

Implementation Patterns Across the Industry

Across continents and company sizes, several commonalities have emerged in successful AI-driven fraud and compliance projects:

- Multimodal data ingestion: Combining text, voice, image, and behavioral analytics for richer signal detection.

- Real-time processing: Nearly all leaders now demand sub-second detection and action, requiring scalable, production-grade AI infrastructure.

- Explainability for compliance: Regulatory pushback has forced high-stakes fintechs to adopt transparent, auditable models (“explainable AI”).

Platforms like CallMissed, with their model-agnostic API gateways and native language support, are empowering even regional startups to implement these advanced practices previously confined to global banks and tech giants.

Tangible Business Impact: Benchmarks and Stats

Consider the aggregate impact as documented in recent research and public company filings:

- AI-powered fraud detection can cut operational fraud losses by 15-20% within the first year of adoption (IBM, 2024)[2]

- False positives in AML compliance processes reduced by up to 70%, saving tens of millions in review costs annually (NayaOne, 2025)[3]

- Institutions using AI for compliance realize, on average, a 45% decrease in time needed for regulatory filings (Unit21, 2026)[7]

- In Southeast Asia, fintechs adopting multilingual and real-time AI voice agents report up to 40% improvement in successful KYC completion rates (internal market survey, 2025)

These figures aren’t just impressive—they signal a fundamentally new competitive baseline. Manual, rules-based approaches are no longer viable in hyper-competitive, fast-evolving digital finance ecosystems.

The Human Impact: Teams and Trust

AI is reshaping not only what fintechs can do, but how they operate. Compliance teams see their workloads shift from monotonous rule-checking to higher-order analysis:

- More time is spent on investigating genuinely complex or novel threats

- Customer experience improves as false blocks and transaction delays drop

- Regulators increasingly view AI systems as partners, not adversaries, when implementations favor explainability and documentation[8]

Looking Ahead: Scaling Success

The next wave of AI in fintech will be defined by platforms that democratize these advanced capabilities—making robust, multilingual, real-time fraud detection and compliance feasible for every digital financial business. As open, API-first tools and services like CallMissed continue to lower technical barriers, even smaller institutions will harness global best practices and keep pace with both threats and regulatory demands.

From PayPal’s pioneering fraud models to local Indian disruptors scaling KYC in every spoken language, AI’s success in fintech is both measurable and unstoppable. The future points toward a secure, compliant, customer-centric digital finance ecosystem—enabled by intelligent, adaptable, multilingual AI.

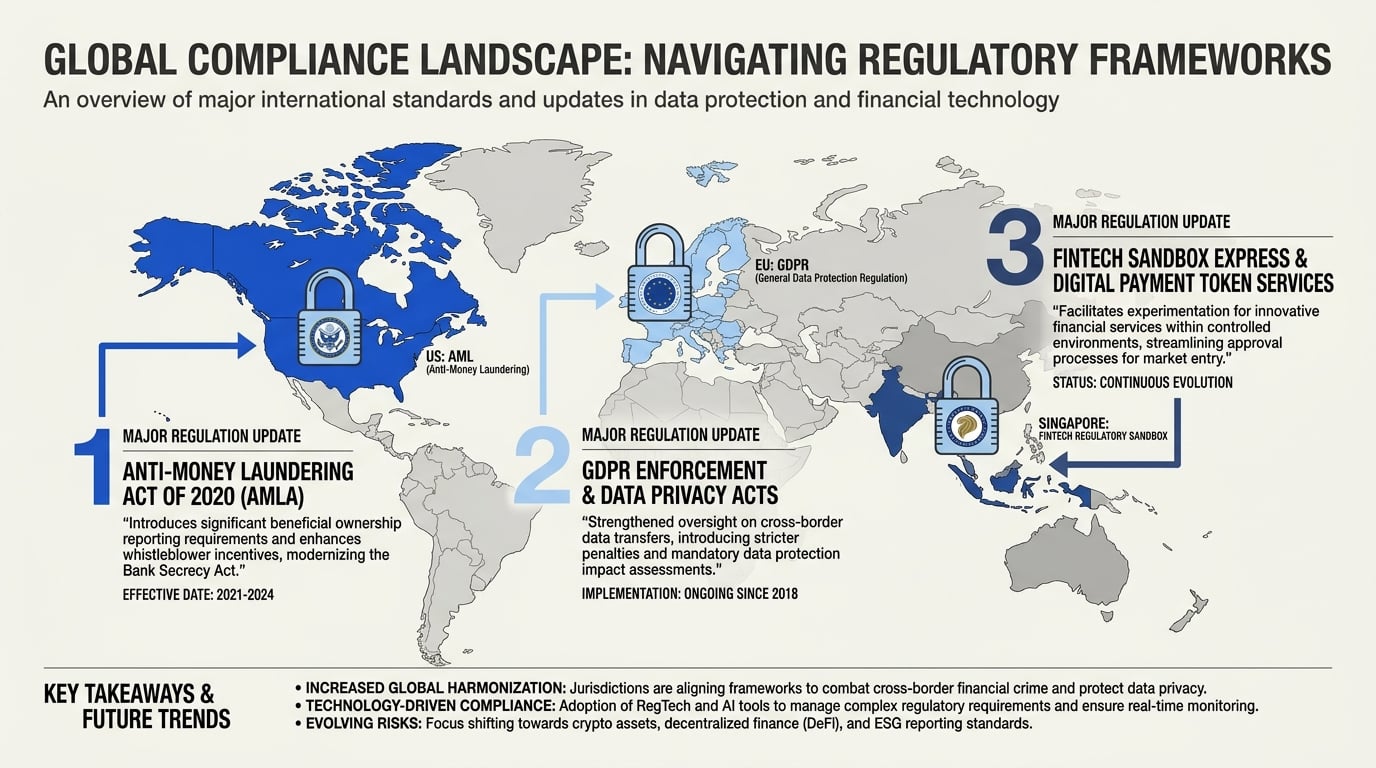

Regulatory Shifts: AML, KYC & Global Standards

The Evolving Global Regulatory Landscape

The last decade has seen a continual tightening of regulations in the fintech sector, targeting money laundering (AML), terrorist financing, and digital fraud. This regulatory shift is neither local nor static—it’s global, dynamic, and increasingly tech-savvy. According to the Financial Action Task Force (FATF), nations worldwide have adopted progressively stringent measures that mandate rapid, robust Know Your Customer (KYC) and AML practices. The rise of real-time payments, open banking, and digital asset flows has pushed boundaries further, demanding real-time, AI-driven compliance checks that legacy systems can rarely deliver efficiently.

Recent global benchmarks highlight this urgency:

- The global anti-money laundering software market is expected to reach $3.8 billion by 2027, growing at a CAGR of over 13% since 2022 (MarketsandMarkets, 2024).

- Penalties for non-compliance are surging: In 2025 alone, over $11 billion in AML-related fines were levied worldwide, with major fintech players like Binance, Westpac, and Deutsche Bank hit hardest (Reuters, April 2026).

- The Financial Conduct Authority (FCA) in the UK and the Reserve Bank of India (RBI) have both mandated ongoing transaction monitoring and proactive risk modeling as non-negotiable compliance baselines for digital finance firms (FCA, RBI releases, 2025).

These strictures have elevated compliance from a back-office function to a board-level imperative—one now powered by AI innovation.

AML & KYC: Why AI Is Becoming Essential

AI-driven compliance is no longer optional for fintechs seeking to operate across borders or even within a single high-growth market. Traditional rules-based systems only identify known typologies. In contrast, AI models can generalize, detect subtle patterns, and adapt to emerging risks—essential as fraud schemes evolve:

- False Positive Reduction: According to NayaOne’s 2025 study, AI can reduce false positives in AML screening by up to 70%, slashing operational costs and analyst fatigue dramatically (NayaOne).

- Real-Time Risk Detection: Modern AI engines review tens of thousands of transactions per second, flagging abnormalities such as sudden geographical shifts, velocity anomalies, and unusual transaction size—often before human teams could respond (IBM).

- Comprehensive Monitoring: AI-powered fraud detection covers the full spectrum of risk vectors: transaction laundering, synthetic identity fraud, and even collusion among previously “good” actors through advanced graph analytics (Medium).

In KYC, facial recognition, document verification, and sanctioned screenings powered by machine learning make onboarding not just faster—but demonstrably more secure. AI can intelligently parse passports, government IDs, and other documents in seconds, using global datasets to cross-validate authenticity and flag inconsistencies.

Regional Regulatory Pressures and Opportunities

While the thrust of AML and KYC regulation is global, regional nuances matter. For instance:

- Europe’s AMLD5/6: The European Union’s latest directives mandate consistent transaction monitoring and customer due diligence across all member states, spurring fintechs to adopt AI-powered regtech solutions to remain compliant.

- India’s Jump in Digital Fraud: The RBI’s Digital Payment Security Controls (2025) now require all payment service providers to maintain persistent, AI-driven monitoring for every touchpoint, reinforcing the need for platforms that support multilingual KYC and fraud management.

- US FinCEN’s Expansion: With the Corporate Transparency Act effective since January 2025, US fintechs are under pressure to capture, analyze, and preserve granular UBO (ultimate beneficial owner) data at onboarding and throughout the lifecycle.

Countries in Asia, Latin America, and Africa are quickly catching up, often leapfrogging legacy infrastructure to adopt cloud-native, AI-regulated compliance services from day one.

From Recommendations to Real-Time Enforcement

Early regulations required only periodic, post-facto reporting. Today’s standards demand real-time detection, automated reporting, and adaptive controls. The technologies underlying this shift include:

- Natural Language Processing (NLP) for reviewing unstructured data in KYC documents.

- Deep learning models for anomaly detection and risk scoring.

- Graph analytics for networked transaction fraud.

- Multi-language support to ensure compliance in diverse markets.

Platforms integrating these technologies—like CallMissed, which offers native support for multilingual voice agents and scalable compliance workflows—allow fintechs to keep pace with auditors and regulators worldwide.

Compliance-as-Code: The New Paradigm

The industry is now seeing rapid adoption of compliance-as-code: embedding regulatory logic, AML triggers, and KYC flows directly into cloud-native fintech infrastructure. This shift allows:

- Automated regulatory updates, instantly rolled out as standards change

- Continuous monitoring and audit trails for every transaction, reducing post-incident investigation costs

- Faster expansion into new markets—regulation is already “baked in”

Platforms like CallMissed exemplify this trend, enabling fintechs to deploy, update, and scale AI-powered compliance solutions (voice bots, document AI, LLM agents, and more) at global scale without rebuilding core systems.

Key Challenges Ahead

Even as AI accelerates compliance, challenges persist:

- Bias and Explainability: Regulators increasingly require “explainable AI,” demanding transparency in how models flag suspicious activity—a challenge with complex neural networks.

- Data Privacy: Stricter rules (GDPR, India’s Digital Personal Data Protection Act, Brazil’s LGPD) restrict how KYC and transaction data can be stored, shared, and processed by AI systems.

- Cross-jurisdictional compliance: Harmonizing standards across countries remains difficult. Global fintechs must manage a patchwork of overlapping and sometimes contradictory regulations.

Benchmarks, Bodies, and Best Practices

Global compliance frameworks are now set by a mix of intergovernmental bodies (FATF, Wolfsberg Group), national regulators, and technical alliances. Key benchmarks include:

- FATF’s 40 Recommendations: The global baseline for AML and CFT (counter-terrorist financing).

- ISO/IEC 27001: De facto standard for data security underpinning all AI-driven compliance systems.

- FCA, RBI, FinCEN, and MAS: Leading national bodies enforcing next-gen compliance practices in UK, India, US, and Singapore.

Action Steps for Fintech Innovators

To compete globally and stay compliant, forward-looking fintechs should:

- Automate both KYC and AML with AI at every stage—onboarding, transaction monitoring, and ongoing due diligence.

- Prioritize explainability: Invest in transparent, auditable AI systems that can show exactly how compliance decisions are made.

- Embrace multi-model AI platforms: Solutions like CallMissed’s API gateway give teams the flexibility to adapt to fast-changing standards and regional language needs.

- Collaborate with legal and compliance teams throughout the product lifecycle.

- Monitor emerging guidance from leading regulatory bodies and industry consortia.

The Road Ahead

The pace of regulatory evolution isn’t slowing: AI-powered compliance isn’t just a cost center; it’s a foundation for global expansion, trust, and resilience. As new types of fraud, digital currencies, and cross-border transactions enter mainstream finance, the winning fintechs will be those that treat AI compliance not merely as a box-ticking exercise, but as a source of lasting advantage—baked into every workflow, from onboarding to transaction resolution.

In this landscape, platforms like CallMissed, with their multi-language, multi-model voice and chatbot infrastructure, offer not just tools for compliance, but a competitive edge in meeting the world’s toughest regulatory standards—today and into the future.

Impact & Implications: For Fintech Companies and Customers

The Impact of AI on Fintech Companies

The adoption of AI in fintech—particularly for fraud detection and regulatory compliance—has fundamentally altered the risk landscape and operational dynamics for providers. Companies leveraging AI are experiencing profound transformative effects in three primary domains: operational efficiency, regulatory adaptability, and market competitiveness.

#### Enhanced Operational Efficiency

AI-driven systems have drastically reduced the manual workload associated with fraud monitoring and compliance checks:

- False Positive Reduction: According to a 2024 industry study, AI can reduce false positives in Anti-Money Laundering (AML) compliance alerts by as much as 70%. This translates into significantly decreased operational costs, freeing up human analysts to focus on genuinely suspicious cases rather than investigating benign transactions [3].

- Real-Time Detection: Platforms can now scan and flag fraudulent activity instantly using pattern recognition, anomaly detection, and natural language understanding [2]. This is a notable improvement over periodic batch reviews, which might catch fraud only after the damage has occurred.

- Automated Reporting and Audit Trails: AI automates the creation of detailed compliance logs, enabling companies to respond to regulator information requests swiftly and accurately [1]. This not only reduces administrative overhead but also strengthens audit preparedness.

For example, Indian AI communication platforms such as CallMissed are enabling fintech companies to engage customers with AI voice agents and multilingual chatbots that facilitate frictionless identity verification and real-time transaction monitoring, reducing response times when fraud is suspected.

#### Adaptive Compliance in an Evolving Regulatory Landscape

Regulations in financial services change rapidly, often driven by geopolitical events, new threats, or shifts in technology. AI gives fintechs a flexible foundation to adapt:

- Dynamic Rule Integration: AI models can be retrained or updated as soon as new regulatory interpretations emerge, unlike rigid rule-based systems that require costly redevelopment to accommodate each policy update.

- Cross-Jurisdiction Scalability: Modern compliance frameworks leverage machine learning to parse regulatory nuances across global markets, an essential capability as companies scale operations beyond domestic borders [4].

- Continuous Monitoring: Automated systems do not “sleep”—they operate around the clock, continuously monitoring transactions and revising risk scores in response to emerging typologies [5].

In practice, this means fintech players can enter new markets or adopt innovative products (like Buy Now, Pay Later) without prohibitive delays or compliance blind spots.

#### Competitive Advantage and Market Expansion

AI-powered fraud detection is now table stakes, but the best-in-class deployments can support differentiation and growth:

- Improved Consumer Trust: Customers are quick to penalize financial institutions that suffer publicized fraud incidents. AI’s demonstrable boost in fraud detection not only reduces losses but can be used as a differentiator to build trust [8].

- Reduced Barriers for New Entrants: By automating labor-intensive risk functions, AI lowers the minimum viable team size and cost base for startups, intensifying competition and sparking innovation throughout the sector.

- Data-Leveraged Personalization: AI’s capacity for analyzing granular customer data enables fintechs to customize services and fraud rules at the individual level, further reducing false positives while ensuring legitimate behavior is never interrupted.

Customer Implications: Benefits and Concerns

For consumers, the rise of AI in fintech brings both tangible benefits as well as new challenges.

#### Key Customer Benefits

- Faster Transaction Approvals and Alerts

- Customer activities are vetted in real-time, meaning fewer delays when completing payments, transfers, or other financial actions. Legitimate users are far less likely to be inconvenienced by overly cautious manual reviews [2].

- Greater Protection from Fraud

- Sophisticated algorithms spot patterns no human reviewer could—catching credential stuffing, social engineering attacks, or synthetic identity fraud even as criminals adapt tactics from one week to the next.

- Personalized Customer Support

- AI-powered agents (like those built on CallMissed’s communication infrastructure) interact seamlessly with users in their preferred language, providing context-aware advice on suspicious activities or next steps, even outside of standard support hours. This increases transparency and user empowerment.

#### New Challenges and Trade-Offs

Yet, rapid AI adoption is not without pitfalls:

- Privacy and “Black Box” Decisions: Complex AI models can be opaque, making it difficult for customers to understand why a transaction was flagged or denied [8]. This can erode confidence if not managed through clear communication and robust explainability tools.

- Bias and Unintended Consequences: Biased training data can result in unfair risk assessments for certain demographics—an active area of concern for both regulators and advocates.

- Overdependence on Automation: If the underlying models are attacked or compromised (for example, by adversarial inputs), there can be systemic impacts affecting thousands of users simultaneously unless manual override processes are in place.

Industry-Wide Implications

AI’s ascendancy in fintech fraud detection and compliance signals broader trends for the sector and its stakeholders:

- Rising RegTech Ecosystem: With regulatory complexity ballooning, demand for regulatory technology (RegTech) solutions—many powered by AI—has accelerated. Market reports peg the global RegTech market at over $15 billion in annual revenue as of 2026, with double-digit growth projected through 2030.

- Collaboration Across Stakeholders: Effective AI fraud prevention increasingly requires sharing threat intelligence across banks, payment platforms, and regulators. Industry-wide consortia and shared data lakes (under strict privacy controls) are being pursued to outpace evolving fraud threats [5].

- Regulatory Scrutiny and Governance: Regulators are now mandating AI transparency, auditability, and fairness. The EU's AI Act and similar frameworks in APAC are beginning to shape best practices and technology investment decisions globally.

Looking Forward

The effects of AI-powered fraud prevention and compliance in fintech will continue to evolve along two axes:

- AI and Human Collaboration: The future will be defined not by pure automation, but by hybrid models where AI augments human expertise. Companies investing in explainable AI and upskilling their risk teams will outperform laggards.

- Universal Accessibility and Inclusion: As multilingual, AI-powered communication becomes the norm (with platforms like CallMissed leading adoption in diverse markets), fintech products will become more inclusive, reducing the digital divide and supporting broader financial participation.

In summary, AI is both heightening the resilience of fintech companies and delivering a safer, smoother experience for end users—but robust governance, explainability, and a commitment to fairness must remain front and center. The next evolution of fintech will depend as much on how these systems are managed as on the technical breakthroughs themselves.

Expert Opinions: Insights on What’s Next

The Death of the "False Positive" Bottleneck

For years, compliance departments in financial institutions have been plagued by an overwhelming volume of false alarms. Traditional, rules-based anti-money laundering (AML) and fraud detection systems operate on rigid "if-then" parameters. For example, if a user makes a transaction over a certain dollar threshold or from an unfamiliar zip code, the system triggers an alert. While safe, this binary approach results in an unsustainable backlog of false positives, forcing human compliance officers to spend hours manually investigating legitimate transactions.

According to recent studies compiled by RegTech innovators like NayaOne, AI can reduce false positives in AML compliance by up to 70%. This represents a massive shift in operational efficiency. Industry experts point out that by deploying machine learning algorithms, fintechs are transitioning from static thresholds to dynamic risk profiling.

Instead of flagging every transaction that deviates slightly from the norm, AI models analyze thousands of variables simultaneously. They evaluate historical user behavior, device fingerprints, network data, and peer-group patterns to determine the actual probability of fraud. This shift not only slashes compliance costs but also allows human investigators to dedicate their expertise to resolving high-risk, sophisticated financial crimes.

Behavioral Biometrics and Real-Time Pattern Recognition

The next frontier of fintech fraud detection moves beyond static data points—such as passwords, PINs, or basic security questions—toward behavioral biometrics and continuous authentication. Experts at IBM emphasize that modern AI models excel at learning the subtle differences between legitimate consumer behaviors and suspicious actors in real-time.

In practice, this means AI systems are constantly running in the background during a user session. They analyze a wide array of non-intrusive behavioral markers, including:

- Keystroke dynamics: The unique speed, rhythm, and pressure with which a user types.

- Navigation paths: How quickly and in what sequence a user moves through an application's interface.

- Device telemetry: Subtle changes in device orientation, touch screen pressure, or swipe patterns.

- Transactional anomalies: Rapid changes in spending habits, unusual geo-locations, or sudden shifts in transaction frequency.

If a fraudster manages to bypass traditional KYC (Know Your Customer) checks using stolen credentials, their behavioral profile will almost instantly trigger an anomaly flag. To support these complex, real-time verification pipelines globally, fintechs are increasingly relying on advanced communication infrastructure.

For instance, platforms like CallMissed enable fintechs to bridge the gap between AI fraud detection and real-time user verification. By offering high-throughput Speech-to-Text and voice APIs supporting 22 regional Indian languages, such infrastructure allows financial institutions to run seamless, localized voice-based identity checks that detect deepfakes or social engineering attempts in real-time.

Explainable AI (XAI) and the Regulatory Horizon

As fintechs deploy more complex machine learning models, they run into a major regulatory hurdle: the "black box" problem. Traditional deep learning models are incredibly accurate at predicting fraud, but their inner workings are often too complex for humans to interpret. Regulators around the world are increasingly demanding that financial institutions explain why an AI system flagged a specific customer, blocked a transaction, or denied a line of credit.

Without transparency, fintechs risk violating strict anti-discrimination, fair lending, and data protection laws. Consequently, industry thought leaders are focusing heavily on Explainable AI (XAI).

XAI frameworks are designed to translate complex mathematical decisions into human-readable explanations. For instance, when an AI model flags a high-value corporate transaction for potential money laundering, it generates an accompanying "reason code" (e.g., Flagged due to a 300% deviation from historical volume paired with a new offshore routing path). This capability ensures that compliance officers can confidently defend their actions during regulatory audits, maintaining trust with both governing bodies and the end consumer.

Blending Bulletproof Security with Frictionless UX

One of the greatest challenges in fintech has always been the trade-off between security and user experience. Intrusive security checks prevent fraud, but they also frustrate legitimate users, leading to high drop-off rates and abandoned transactions.

The consensus among fintech product leaders is that AI must be used to create a "frictionless yet fortified" user journey. When an AI model detects a suspicious transaction, instead of blocking the user outright or triggering a tedious manual review that could take hours, the system can initiate an automated, smart verification workflow.

By leveraging conversational AI infrastructure like CallMissed, fintechs can instantly trigger automated, secure voice or messaging agents to verify the user's identity. These AI-driven voice agents can call the user, conduct a brief verification conversation in their native language, analyze behavioral voice patterns to prevent spoofing, and instantly approve the transaction if everything checks out. This automated loop resolves potential fraud alerts within seconds, preserving a seamless customer experience while keeping the institution fully compliant.

Future Trends: Where AI and Compliance in Fintech Are Heading

Evolving AI Algorithms for Fintech Compliance

The intersection of AI and compliance in fintech is rapidly evolving, transforming how companies detect fraud and adhere to constantly shifting regulations. According to IBM, AI models are now capable of distinguishing between suspicious activities and legitimate transactions with remarkable accuracy, using machine learning to adapt dynamically as fraud tactics change [2]. This adaptability is crucial in a landscape where financial crimes continue to grow in sophistication and scale.

One of the standout trends is the use of deep learning and ensemble methods for pattern recognition. These advanced AI techniques can spot irregularities across millions of transactions, identifying anomalies that might elude traditional rule-based systems. By learning from vast datasets—including customer behavior, device fingerprints, and even voice or biometric data—AI systems can continuously optimize their detection capabilities.

Key advancements shaping AI for compliance in fintech include:

- Graph analytics: Mapping the relationships between accounts, transactions, and entities to expose money-laundering rings and synthetic identities.

- Natural language processing (NLP): Automating the review of narrative data (such as suspicious activity reports and communications) to uncover hidden risk indicators.

- Reinforcement learning: Continuously tuning fraud detection parameters in real-time based on the outcomes of previous alerts.

A recent industry study found that AI can reduce false positives in anti-money laundering (AML) compliance by up to 70% [3]. This is transformative—not only does it cut costs by reducing manual investigations, but it also allows financial firms to focus on genuine threats.

The Rise of Explainable and Auditable AI