UPI & Digital Payments in India: 2026 Speed, Safety and Business Automation Opportunity

Learn how UPI’s 2026 scale, safety risks, QR habits and business automation workflows can help Indians pay faster and safer.

UPI & Digital Payments in India: 2026 Speed, Safety and Business Automation Opportunity

What if India’s fastest-growing payment habit is no longer just paying faster—but running entire businesses faster?

UPI & Digital Payments in India have moved far beyond QR codes at tea stalls and instant money transfers between friends. They are now becoming the operating layer for commerce, credit, fraud detection, customer support, subscriptions, refunds, and business automation. According to PwC’s Indian Payments Handbook 2023–2028, the next phase of India’s payments market is being shaped by conversational payments in UPI, frictionless credit, and digital public infrastructure—turning payments from a back-end transaction into a front-end customer experience.

The timing matters. In 2026, three forces are colliding: speed, safety, and automation. UPI’s real-time rails have made instant payments normal for consumers, but businesses now need the same instant responsiveness in reconciliation, invoicing, collections, support, and fraud checks. At the same time, security is becoming a boardroom issue. The Press Information Bureau notes that NPCI provides an AI/ML-based fraud-monitoring solution to banks for generating alerts and declining suspicious transactions, while the European Payments Council highlights NPCI’s role in securing UPI across the customer lifecycle. That focus is critical because research on UPI fraud points to growing risks from phishing, impersonation, scams, synthetic identities, and mule accounts.

New rule changes are also pushing the ecosystem forward. Reports around 2026 digital payment guidelines point to tighter security from April 1, 2026, including stronger authentication expectations, while earlier NPCI changes from April 2025 restricted saved or shared QR codes for international UPI payments. The message is clear: India’s payment infrastructure is becoming faster, but also more controlled, verified, and automation-ready.

In this article, we’ll unpack why UPI is still one of India’s most viral fintech stories, what the 2026 safety shift means for consumers and merchants, and where the biggest business automation opportunities are emerging—from QR payments and UPI Lite to payment-linked workflows, AI support, and WhatsApp-based commerce. Platforms like CallMissed are part of this broader shift, helping businesses connect payment journeys with AI voice agents, WhatsApp chatbots, and multilingual customer communication.

Introduction: Why UPI Has Become India’s Everyday Digital Habit

From Payment Method to Daily Infrastructure

UPI’s biggest achievement is not that it made payments digital—it made them habitual. In India, paying by scanning a QR code, sending money through a mobile number, or settling a bill instantly has become part of everyday behavior across metros, small towns, and informal retail. That shift matters because once a payment system becomes a habit, it stops being just a financial tool and starts becoming business infrastructure.

This is why UPI & Digital Payments in India are now moving into a new phase in 2026. Consumers expect speed by default. Merchants expect instant confirmation. Banks and regulators expect stronger fraud controls. And businesses increasingly want payments to trigger automated workflows—receipts, refunds, support tickets, delivery updates, reminders, and reconciliation.

PwC’s Indian Payments Handbook 2023–2028 points to the next wave clearly: India’s payments future will be shaped by digital public infrastructure, frictionless credit, and conversational payments in UPI. In simple terms, payments are becoming more embedded, more intelligent, and more connected to customer conversations.

Why UPI Became India’s Default Digital Reflex

UPI became viral because it solved three problems at once:

- Speed: Money moves in real time, making digital payments feel as immediate as cash.

- Access: QR codes and mobile-first interfaces lowered the barrier for small merchants and consumers.

- Trust: NPCI, RBI, banks, and payment apps created a nationwide interoperable system rather than isolated wallets.

The European Payments Council describes UPI as a system where NPCI secures the payment experience “throughout the customer lifecycle,” while India’s Press Information Bureau notes that NPCI provides an AI/ML-based fraud-monitoring solution to banks for generating alerts and declining suspicious transactions. That combination—instant usability plus layered security—is why UPI has become more than a checkout option.

But scale brings new risks. Research on UPI fraud highlights vulnerabilities including:

- Phishing

- Impersonation

- Scams

- Synthetic identities

- Mule accounts

This is the tension defining 2026: India wants payments to stay fast, but not careless; frictionless, but not vulnerable.

The 2026 Opportunity: Payments That Start Workflows

The most important shift is that UPI is no longer only about “pay and done.” For businesses, a successful payment can now become the starting point for automation:

- A paid invoice can trigger an order update.

- A failed payment can trigger a WhatsApp reminder.

- A refund request can open an AI support conversation.

- A subscription payment can update CRM records.

- A suspicious transaction can trigger verification.

This is where digital payments intersect with AI communication. Platforms like CallMissed are part of this broader movement, helping businesses connect payment journeys with AI voice agents, WhatsApp chatbots, multilingual support, and LLM-powered automation. For a merchant, the opportunity is not just receiving money faster—it is responding faster after the payment happens.

Why This Moment Is Bigger Than QR Codes

Regulation is also pushing the ecosystem forward. Reports around new digital payment guidelines indicate tighter security expectations from April 1, 2026, while earlier NPCI changes from April 2025 restricted saved or shared QR codes for international UPI payments. These shifts show that India’s payment rails are maturing from growth-first to growth-with-control.

That makes 2026 a defining year. UPI has already won consumer behavior. The next viral opportunity is business automation: using instant payments as the trigger for instant service, instant verification, and instant customer communication.

Background & Context: From Real-Time Payments Rail to Mass Digital Infrastructure

The Rail: UPI as India’s Real-Time Settlement Layer

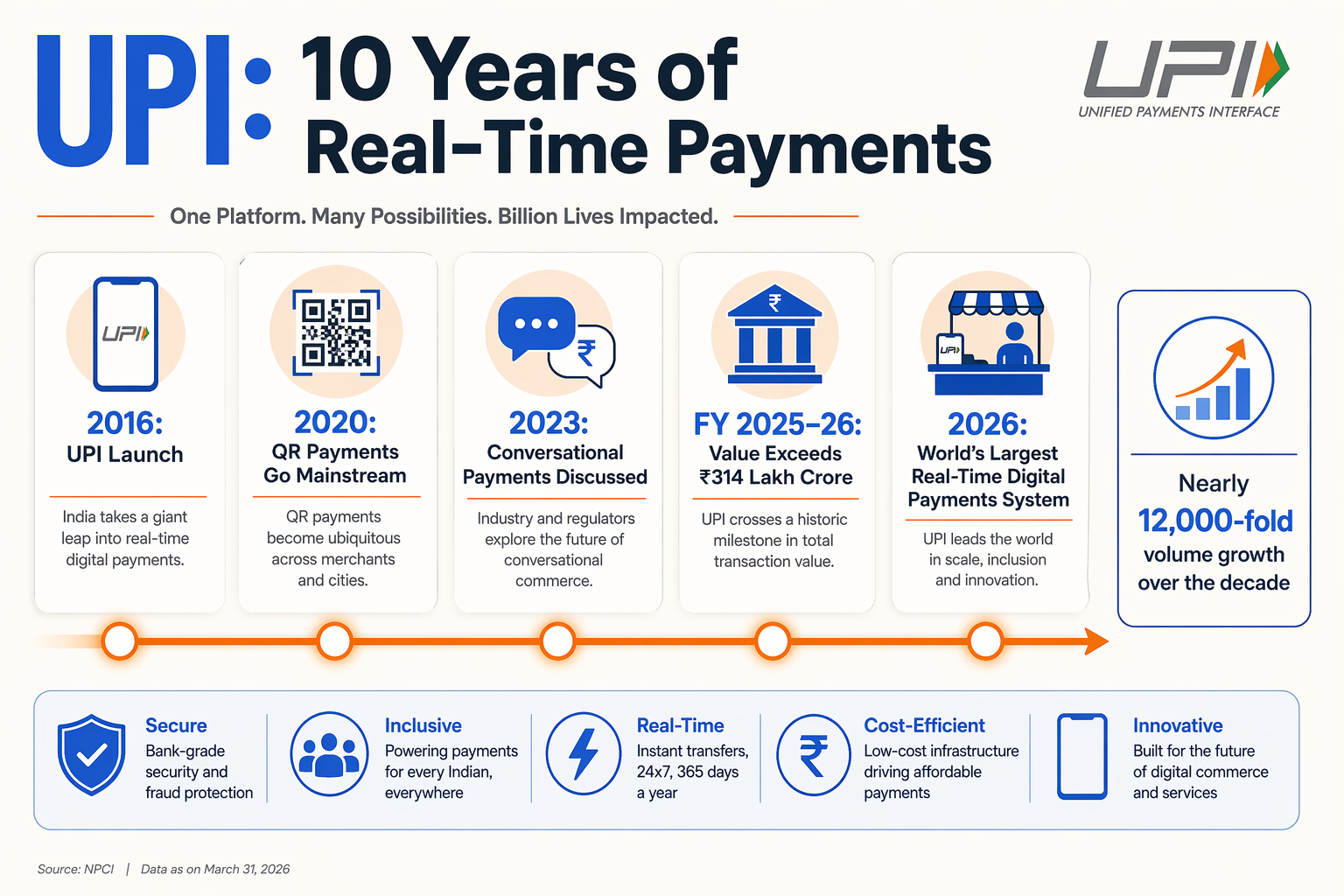

UPI began as a payments interface, but its deeper significance is that it created a real-time, interoperable rail between banks, apps, merchants, and consumers. Unlike card networks that depend on merchant acquiring infrastructure, UPI made account-to-account transfers usable through simple identifiers—mobile numbers, VPAs, and QR codes. That reduced friction for both sides of commerce: consumers could pay instantly, while even the smallest merchants could accept digital payments without expensive hardware.

The European Payments Council describes UPI as “revolutionising real-time digital payments in India,” highlighting how NPCI’s infrastructure supports instant transactions while maintaining security across the customer lifecycle. This matters because real-time payments are not just faster versions of older payments; they change user expectations. Once money moves instantly, customers expect everything around the transaction to move instantly too:

- Instant payment confirmation

- Real-time order updates

- Immediate refunds or dispute status

- Automated receipts and invoices

- Faster merchant reconciliation

- Always-on customer support

That is why UPI’s evolution is now tied to broader digital infrastructure, not just fintech adoption.

The Stack: Payments, Identity, Credit, and Automation

India’s payments journey is also part of a larger digital public infrastructure story. PwC’s Indian Payments Handbook 2023–2028 notes that the RBI has envisaged a digital public tech platform for frictionless credit and conversational payments in UPI. This signals a major shift: payments are becoming connected to credit decisioning, customer communication, and embedded commerce.

In practical terms, this means a merchant payment flow may soon look less like a standalone transaction and more like an automated business workflow:

- A customer asks a question on WhatsApp or voice.

- An AI assistant recommends a product or service.

- The customer receives a UPI payment link or QR.

- Payment confirmation triggers inventory, invoice, delivery, or appointment workflows.

- Customer support continues automatically in the same conversation.

This is where platforms such as CallMissed fit into the broader trend. Businesses are increasingly connecting UPI payment journeys with AI voice agents, WhatsApp chatbots, multilingual support, and automated follow-ups, so the payment is no longer the end of the customer interaction—it becomes the trigger for the next action.

The Governance Layer: Speed Now Requires Stronger Controls

As UPI became mass infrastructure, safety became inseparable from scale. The Press Information Bureau states that NPCI provides an AI/ML-based fraud-monitoring solution to banks for “generating alerts and declining suspicious transactions.” That is an important architectural point: fraud prevention is moving from manual review to real-time risk scoring.

The fraud landscape is also evolving. Research on UPI fraud identifies growing vulnerabilities from:

- Phishing

- Impersonation

- Scams

- Synthetic identities

- Mule accounts

These risks are amplified by the very strengths that made UPI popular—speed, convenience, and wide accessibility. A scam that succeeds in a real-time payment environment can move money before a victim has time to react. That is why 2026 is expected to be defined not only by growth, but by stricter verification and smarter monitoring.

Reports around new digital payment rules indicate tighter security expectations from April 1, 2026, including stronger authentication frameworks. Separately, NPCI’s earlier international UPI change from April 2025 removed the option to pay using saved or shared QR codes outside India, reinforcing the direction of travel: more convenience, but with tighter controls around misuse.

The Context for 2026: UPI as Business Infrastructure

The key background for 2026 is simple: UPI is no longer just a consumer payment habit. It is becoming a programmable layer for business operations. The next opportunity is not merely “accept UPI payments,” but to automate what happens before and after the payment.

For Indian businesses, that means:

- Faster collections and fewer manual follow-ups

- Better reconciliation across branches and channels

- Payment-linked customer support

- Fraud-aware onboarding and transaction checks

- UPI flows embedded into WhatsApp, voice, and app experiences

In short, India’s real-time payments rail has matured into mass digital infrastructure. The viral opportunity now sits at the intersection of instant money movement, trusted security, and automated business response.

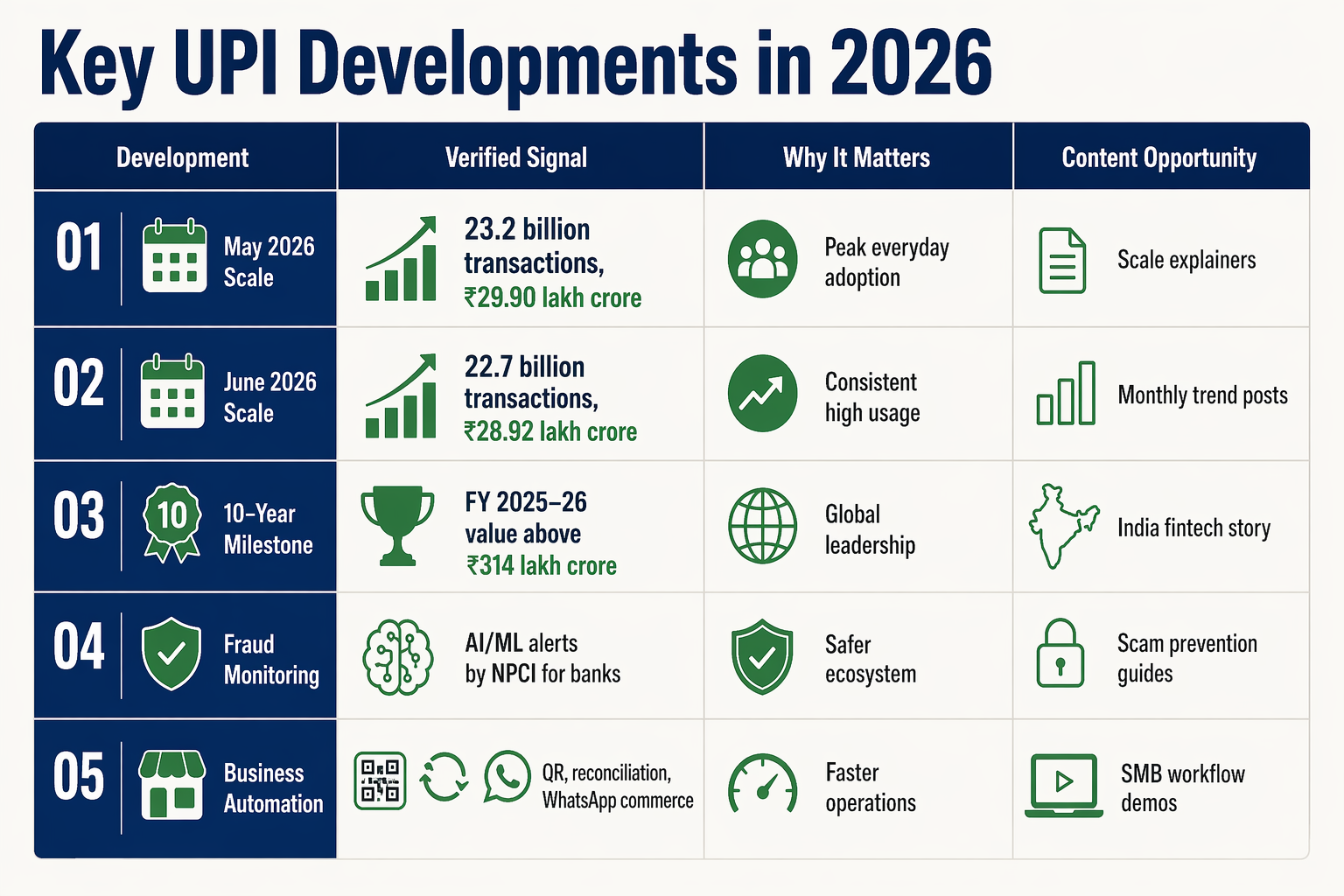

Key Developments (TABLE): 2026 UPI Scale, Safety Signals and Automation Trends

What the 2026 UPI Shift Looks Like in Practice

The next phase of UPI & digital payments in India is not one single upgrade—it is a stack of changes across scale, fraud controls, authentication, global usage, and automation. The useful way to read 2026 is as a transition from “instant payment” to instant, verified, workflow-ready payment infrastructure.

| Development | 2026 Signal | Source / Date | Business Impact |

|---|---|---|---|

| UPI as real-time commerce infrastructure | UPI continues evolving beyond peer-to-peer transfers into merchant payments, credit, refunds, and embedded commerce | PwC’s Indian Payments Handbook 2023–2028 highlights conversational payments in UPI and frictionless credit | Businesses can build payment journeys directly into chat, apps, billing, and support flows |

| AI-led fraud monitoring | NPCI provides an AI/ML-based fraud-monitoring solution to banks for alerts and declining suspicious transactions | Press Information Bureau, Government of India | Fraud checks are becoming more automated, real-time, and institution-wide |

| Stronger safety rules | Reports point to tighter digital payment security from April 1, 2026, including stronger authentication expectations | RBI/NPCI-linked 2026 digital payment rule coverage | Merchants should prepare for better identity checks, fewer risky flows, and more compliance-led UX |

| International UPI controls | From April 2025, NPCI removed saved/shared QR code payments for international UPI usage | OxigenWallet summary of NPCI rule change | Cross-border UPI becomes more controlled, reducing misuse of static or forwarded QR codes |

| Fraud risk expansion | UPI fraud research flags phishing, impersonation, scams, synthetic identities, and mule accounts | IJSRET vulnerability analysis | Businesses need customer education, transaction monitoring, and support escalation systems |

| Payment-linked automation | WhatsApp commerce, AI voice agents, payment reminders, and automated reconciliation are becoming mainstream use cases | Market trend + business automation demand in 2026 | Platforms like CallMissed can connect payment events with AI calls, WhatsApp chatbots, and multilingual support |

Why These Developments Matter Together

Individually, these updates may look like compliance changes or product enhancements. Together, they point to a bigger shift: UPI is becoming programmable business infrastructure.

For a small retailer, that could mean automated payment reminders on WhatsApp. For a lending company, it could mean UPI-linked credit collection flows. For an e-commerce brand, it could mean instant refunds, payment confirmation messages, and AI-led customer support after failed transactions. For banks and fintechs, it means fraud detection needs to happen in milliseconds—not after a complaint is filed.

The safety layer is especially important because speed cuts both ways. The same real-time rails that make UPI convenient also increase exposure to fast-moving fraud. That is why the PIB’s note that NPCI offers AI/ML-based fraud monitoring to all banks is significant: fraud prevention is no longer only a customer-awareness problem; it is becoming an infrastructure problem.

The Automation Opportunity for Businesses

The viral opportunity in 2026 is not just “accept UPI.” Most businesses already do that. The opportunity is to automate what happens before, during, and after payment.

Businesses should focus on:

- Before payment: invoice generation, payment links, WhatsApp reminders, customer verification

- During payment: real-time confirmation, fraud flags, assisted checkout, fallback options

- After payment: reconciliation, receipts, refunds, support tickets, repeat purchase nudges

This is where AI communication infrastructure becomes relevant. For example, platforms like CallMissed help businesses connect UPI-driven workflows with AI voice agents, WhatsApp chatbots, LLM inference across 300+ models, and Speech-to-Text support for 22 Indian languages. That matters in India because payment support is often multilingual, high-volume, and time-sensitive.

The key lesson for 2026: UPI’s next growth story will not be measured only by transaction volume. It will be measured by how safely and intelligently businesses can automate around every transaction.

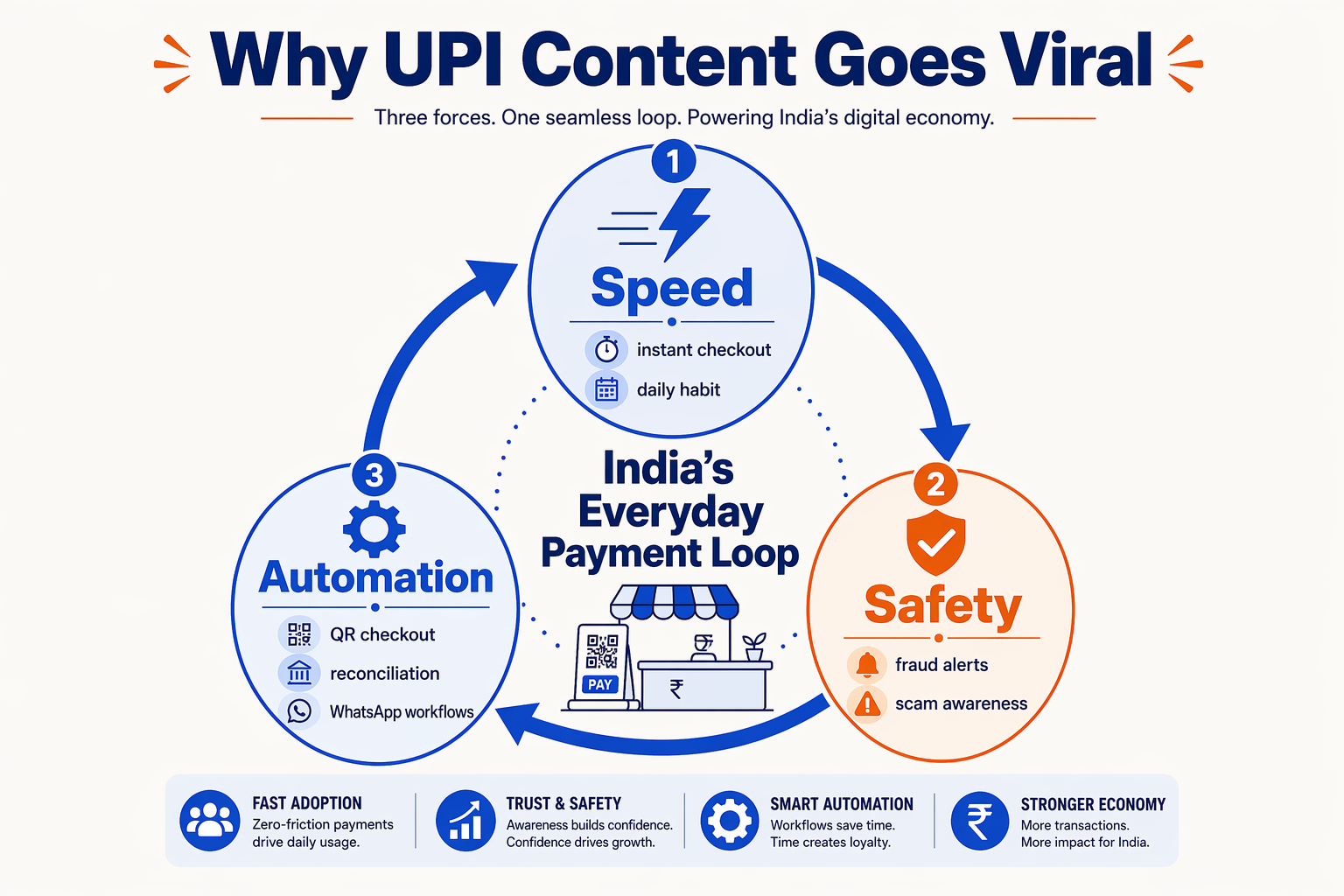

In-Depth Analysis: Speed, Trust and the Viral Mechanics of UPI Content

Why UPI Content Travels So Fast

UPI is viral because it sits at the intersection of money, habit, and anxiety. Almost every Indian consumer has a payment story: a QR scan that worked instantly, a refund that arrived in seconds, a failed transaction panic, or a suspicious “collect request” from a fraudster. That makes UPI content unusually shareable—it is not abstract fintech; it is daily life.

The strongest UPI content in 2026 usually works because it answers one of three urgent questions:

- “Can I pay faster?”

Consumers care about instant checkout, UPI Lite, QR payments, and fewer failed transactions.

- “Is my money safe?”

Fraud prevention content spreads quickly because UPI scams feel personal and immediate.

- “Can my business automate this?”

Merchants want payment links, auto-reconciliation, reminders, refunds, support, and CRM workflows connected to payments.

PwC’s Indian Payments Handbook 2023–2028 captures this shift clearly, noting that India’s next payments phase is being shaped by digital public infrastructure, frictionless credit, and conversational payments in UPI. That is why UPI is no longer just a transaction rail—it is becoming a content, commerce, and automation layer.

The Speed Story: Instant Payments Create Instant Expectations

UPI has trained users to expect real-time confirmation. The problem is that many businesses still operate around slow back-office processes: manual reconciliation, delayed invoice matching, missed customer calls, and disconnected support teams.

This gap creates a major viral and commercial opportunity. Content that shows “before vs after” business workflows performs well because the pain is obvious:

- A customer pays, but the business cannot identify the order.

- A retailer receives multiple QR payments but reconciles them manually.

- A service provider misses calls from customers asking, “Payment ho gaya kya?”

- A refund is processed, but no one informs the customer.

The next wave of digital payment adoption will be about what happens after the payment. Businesses need automated confirmations, WhatsApp receipts, payment-linked support tickets, and voice agents that can answer transaction queries 24/7. Platforms such as CallMissed fit into this trend by connecting AI voice agents and WhatsApp chatbots with customer communication workflows, helping businesses respond instantly when payments trigger questions, orders, or service requests.

The Trust Story: Safety Is Now a Growth Feature

Speed creates adoption, but trust sustains it. As UPI usage expands, fraud content is becoming one of the most viral categories in Indian fintech because it combines urgency with practical value.

The Press Information Bureau has stated that NPCI provides an AI/ML-based fraud-monitoring solution to banks for generating alerts and declining suspicious transactions. The European Payments Council also highlights that NPCI secures UPI across the customer lifecycle through comprehensive fraud prevention and risk controls.

That matters because UPI fraud is no longer limited to simple mistakes. Research on UPI vulnerabilities points to risks including:

- Phishing

- Impersonation

- Scams

- Synthetic identities

- Mule accounts

Safety-focused content spreads because users want clear, memorable rules: never approve unknown collect requests, verify merchant names, avoid screen-sharing during payment support, and treat “urgent refund” calls with suspicion.

The 2026 Viral Formula for UPI Topics

The most effective UPI content blends utility + emotion + proof. In practice, that means:

- Start with a real-life scenario

Example: “A customer paid ₹2,500, but the merchant never received confirmation.”

- Explain the rule or risk simply

Tie it to known changes, such as tighter digital payment security expectations from April 1, 2026, or NPCI’s earlier April 2025 restriction on saved/shared QR codes for international UPI payments.

- Show the automation angle

Demonstrate how businesses can reduce disputes with instant alerts, reconciliation, WhatsApp updates, and AI-assisted support.

- End with a checklist

Viral UPI content often gets saved and forwarded when it gives users a short action plan.

The key insight: UPI’s 2026 opportunity is not just “faster payments.” It is faster trust—the ability to pay, verify, communicate, and resolve issues in one seamless loop.

Impact & Implications: What Massive UPI Adoption Changes for Consumers and Merchants

Consumers: Payments Become Faster, but Expectations Become Higher

Mass UPI adoption has changed what Indian consumers consider “normal.” A payment that takes minutes, requires manual confirmation, or creates uncertainty now feels broken. The real implication is not just instant money movement—it is instant trust.

For consumers, UPI’s next phase creates three major shifts:

- Speed becomes invisible: Users no longer think of UPI as “digital payments”; they expect checkout, refunds, bill splits, subscriptions, and merchant confirmations to happen in real time.

- Safety becomes part of the user experience: With reports pointing to tighter digital payment security from April 1, 2026, stronger authentication and fraud controls will increasingly shape how consumers approve transactions.

- Payments become conversational: PwC’s Indian Payments Handbook 2023–2028 highlights conversational payments in UPI as a major direction. That means users may increasingly pay inside chat, voice, and assisted commerce flows—not just inside banking or payment apps.

This also raises the bar for dispute handling. If a consumer pays instantly but receives no order update, refund timeline, or support response, the payment experience feels incomplete. In other words, the transaction is no longer the end of the journey—it is the trigger for service.

Merchants: UPI Turns Cash Flow Into Real-Time Operations

For merchants, massive UPI adoption changes the economics of running a business. Earlier, payment collection, reconciliation, customer confirmation, and support were separate workflows. Now, they can be connected into one automated loop.

A small retailer, clinic, coaching center, restaurant, or D2C brand can use UPI-linked workflows to:

- Confirm payments instantly and reduce manual follow-ups.

- Trigger invoices, receipts, or order updates automatically.

- Segment customers based on payment history or repeat purchases.

- Detect suspicious transaction patterns before losses escalate.

- Automate reminders for pending payments, renewals, or subscriptions.

This is why UPI is becoming more than a checkout method. It is becoming a business automation layer. The opportunity is especially strong for India’s MSMEs, where payment confirmation and customer communication still often happen manually over phone calls or WhatsApp.

Platforms such as CallMissed fit into this shift by helping businesses connect payment events with AI voice agents, WhatsApp chatbots, and multilingual customer communication—for example, automatically answering “Has my payment been received?” or sending a WhatsApp receipt after a successful transaction.

Safety Becomes a Competitive Advantage

The faster payments move, the faster fraud can move too. Research on UPI fraud points to vulnerabilities including phishing, impersonation, scams, synthetic identities, and mule accounts. These are not abstract risks; they directly affect consumer confidence and merchant losses.

That is why security infrastructure is becoming central to UPI’s next chapter. The Press Information Bureau notes that NPCI provides an AI/ML-based fraud-monitoring solution to banks for generating alerts and declining suspicious transactions. The European Payments Council also highlights NPCI’s role in securing UPI across the customer lifecycle, not just at the point of transaction.

For merchants, this means safety will increasingly influence customer loyalty. Businesses that clearly communicate payment status, use verified channels, avoid suspicious payment links, and respond quickly to failed or disputed payments will win more trust.

The Big Implication: Payments and Communication Are Converging

The most important change is structural: payment systems and customer communication systems are merging. A UPI payment can now trigger a WhatsApp message, a support ticket, a delivery update, a refund workflow, a credit offer, or a fraud alert.

This creates a powerful opportunity in 2026: businesses that treat UPI as a workflow engine—not just a payment rail—will move faster, reduce manual work, and deliver safer customer experiences. Consumers get convenience. Merchants get automation. The ecosystem gets more intelligent, more secure, and more deeply embedded in everyday commerce.

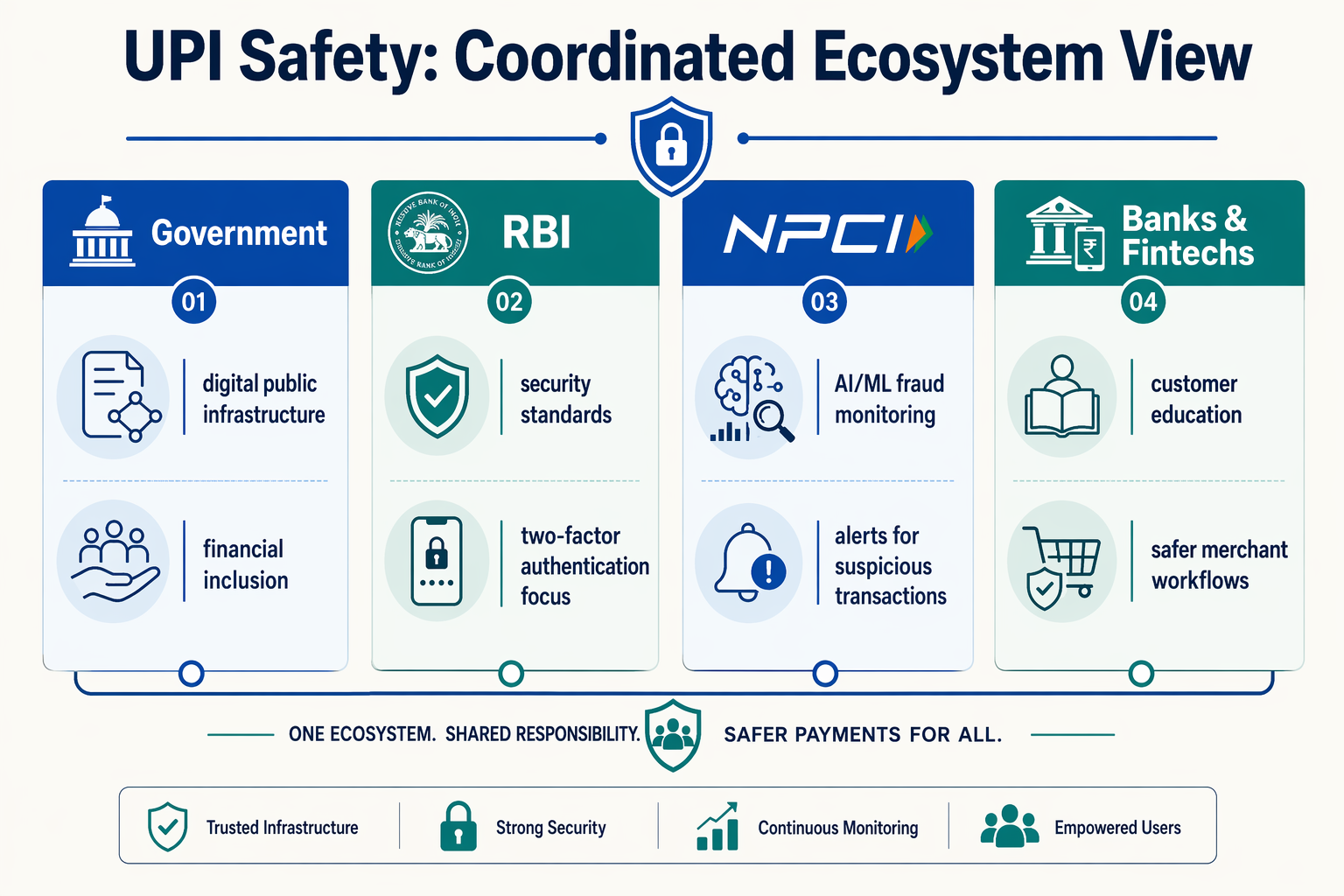

Expert Opinions: What Government, RBI, NPCI and Fintech Voices Emphasize

Government View: Scale Must Come With Trust

The Government of India’s message is increasingly clear: digital payments growth is not just a fintech success story—it is public infrastructure. The Press Information Bureau (PIB) highlights “coordinated efforts of Government, RBI and NPCI” in accelerating digital payment growth, but the more important signal is its emphasis on fraud controls. PIB specifically notes that NPCI provides an AI/ML-based fraud-monitoring solution to all banks for “generating alerts and declining suspicious transactions.”

That matters because UPI’s next growth phase depends on confidence. If consumers fear scams, payment links, QR codes, or collect requests, adoption slows. Government positioning is therefore focused on:

- Consumer protection through better fraud detection

- Bank participation in real-time risk monitoring

- Digital public infrastructure that can scale safely

- Financial inclusion without compromising security

In short, the government sees UPI as a national rails system—not merely an app-based convenience.

RBI View: Payments Are Becoming Programmable

The Reserve Bank of India’s direction is more structural. As cited in PwC’s Indian Payments Handbook 2023–2028, the RBI has envisaged a digital public tech platform for frictionless credit and conversational payments in UPI. This points to a future where payment, identity, credit assessment, and customer interaction become tightly connected.

The “conversational payments” signal is especially important for 2026. It suggests payments may increasingly happen inside natural user journeys—chat, voice, commerce apps, service bots, and assisted channels—rather than only inside banking apps.

For businesses, this means UPI will not remain limited to “pay now” flows. It will power:

- Credit-linked checkout

- Subscription and mandate experiences

- Voice or chat-led payment initiation

- Automated collections and reminders

- Real-time refunds and reconciliation

This is where platforms like CallMissed fit into the wider trend: AI voice agents and WhatsApp chatbots can help businesses guide customers through payment reminders, order confirmations, and support queries while keeping UPI as the transaction layer.

NPCI View: Security Across the Customer Lifecycle

NPCI’s role is not only to run the UPI network but also to standardize how trust works across participants. The European Payments Council notes that NPCI ensures UPI security “throughout the customer lifecycle” by implementing comprehensive fraud-prevention measures. That phrase—customer lifecycle—is important because fraud does not happen only at the moment of payment.

Risk can appear during:

- User onboarding

- Device binding

- QR-code sharing

- Payment-link clicks

- Collect-request approvals

- Merchant verification

- Refund and dispute flows

The April 2025 change restricting saved or shared QR codes for international UPI payments, referenced in 2026 rule summaries, reflects this lifecycle thinking. Instead of treating every QR as permanently safe, the ecosystem is moving toward context-aware authorization.

Fintech View: Automation Is the Commercial Opportunity

Fintech leaders are reading these signals as a major automation opportunity. PwC’s 2023–2028 outlook connects UPI’s future with conversational interfaces, digital public infrastructure, and frictionless credit. Meanwhile, fraud research warns that UPI’s “magnitude, speed, and functionality” have increased exposure to phishing, impersonation, scams, synthetic identities, and mule accounts.

That combination creates a clear fintech agenda: make payments faster for legitimate users and harder for attackers.

The strongest 2026 product opportunities are likely to come from fintechs that combine:

- Real-time risk scoring

- AI-assisted customer support

- Multilingual payment guidance

- Automated merchant reconciliation

- Verified payment journeys

- UPI-linked CRM and commerce workflows

For India’s small businesses, the practical need is simple: they do not just want a successful payment notification; they want the invoice marked paid, the customer updated, the order moved forward, and the support team informed. With multilingual speech-to-text in 22 Indian languages and AI communication workflows, solutions such as CallMissed show how payment automation can extend beyond fintech apps into everyday business operations.

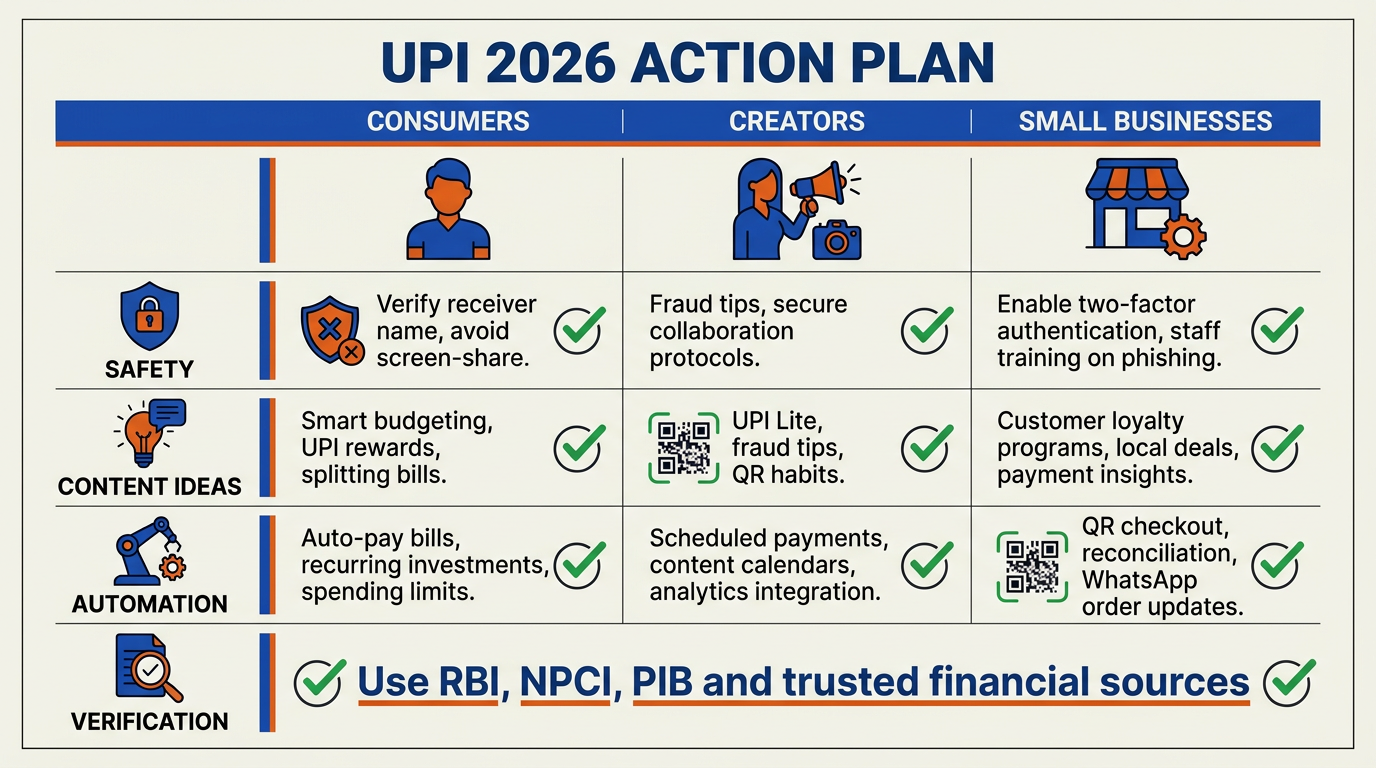

What This Means For You (TABLE): Practical Actions for Users, Creators and Small Businesses

Turning the 2026 UPI Shift Into Daily Advantage

For consumers, creators, and small businesses, the message is simple: UPI is no longer just a payment button—it is a workflow trigger. Every scan, collection request, subscription, refund, or failed payment can now feed into customer support, inventory, reminders, fraud checks, and accounting.

That matters more in 2026 because the ecosystem is becoming both faster and stricter. Reports on new digital payment rules point to tighter security from April 1, 2026, while NPCI’s earlier April 2025 change removed saved/shared QR codes for international UPI payments. At the same time, the Press Information Bureau has confirmed that NPCI provides an AI/ML-based fraud-monitoring solution to banks for generating alerts and declining suspicious transactions.

Here’s how different groups can act on this shift.

| Who You Are | What To Do Now | Why It Matters in 2026 | Useful Tools / Signals | Risk To Avoid |

|---|---|---|---|---|

| Everyday UPI users | Enable app locks, check payee names, avoid unknown collect requests | UPI fraud research flags phishing, impersonation, scams, synthetic identities, and mule accounts as rising risks | Bank alerts, UPI PIN hygiene, device security | Approving “receive money” requests that actually debit your account |

| Small retailers | Use dynamic QR codes, auto-reconciliation, and instant payment confirmation | Static QR workflows are easier to misuse; automation reduces manual settlement errors | POS-linked UPI, accounting integrations, SMS/WhatsApp receipts | Depending only on screenshots as proof of payment |

| Creators & freelancers | Add payment links, UPI Lite for low-value sales, and automated reminders | Faster collection improves cash flow for courses, events, consultations, and digital products | UPI payment links, WhatsApp broadcasts, invoice tools | Mixing personal and business payments without records |

| D2C brands | Connect UPI payments with order status, refunds, and support tickets | PwC highlights conversational payments in UPI as a major next-stage trend | WhatsApp commerce, CRM, chatbot flows | Making customers chase support after payment failures |

| Service businesses | Automate booking deposits, renewal reminders, and post-payment calls | Payments can trigger operations instantly: appointment confirmation, invoice, feedback, upsell | AI voice agents, WhatsApp bots, calendar/payment APIs | Manual follow-ups that delay service delivery |

| Growing SMEs | Build fraud review rules and payment-linked dashboards | NPCI already uses AI/ML-based fraud monitoring at ecosystem level; businesses need their own layer too | Risk scoring, transaction logs, role-based access | Giving too many staff members unrestricted payment access |

The Best Practical Move: Link Payments to Communication

The biggest automation gap for Indian businesses is not accepting UPI—it is what happens after payment. Many businesses still manually confirm transfers, send receipts, update customers, or ask staff to call buyers after failed transactions.

A better 2026 workflow looks like this:

- Customer pays through UPI or QR

- System verifies payment status

- Receipt or order confirmation is sent automatically

- Customer gets WhatsApp or voice support if payment fails

- Data flows into CRM, accounting, or fulfilment software

This is where platforms such as CallMissed fit into the broader payments opportunity. A business can connect payment events with AI voice agents, WhatsApp chatbots, and multilingual communication—useful in a country where support often needs to happen across regional languages, not just English.

A Simple Checklist Before You Scale

Before adding more payment channels, check these basics:

- Separate business and personal UPI IDs

- Use verified merchant QR codes

- Automate receipts and reconciliation

- Train staff to detect collect-request scams

- Review failed, refunded, and disputed transactions weekly

- Create customer support flows for payment confusion

The viral opportunity around UPI in 2026 is not only about faster transactions. It is about making every transaction safer, traceable, and actionable—so users avoid fraud, creators collect faster, and small businesses operate with less manual work.

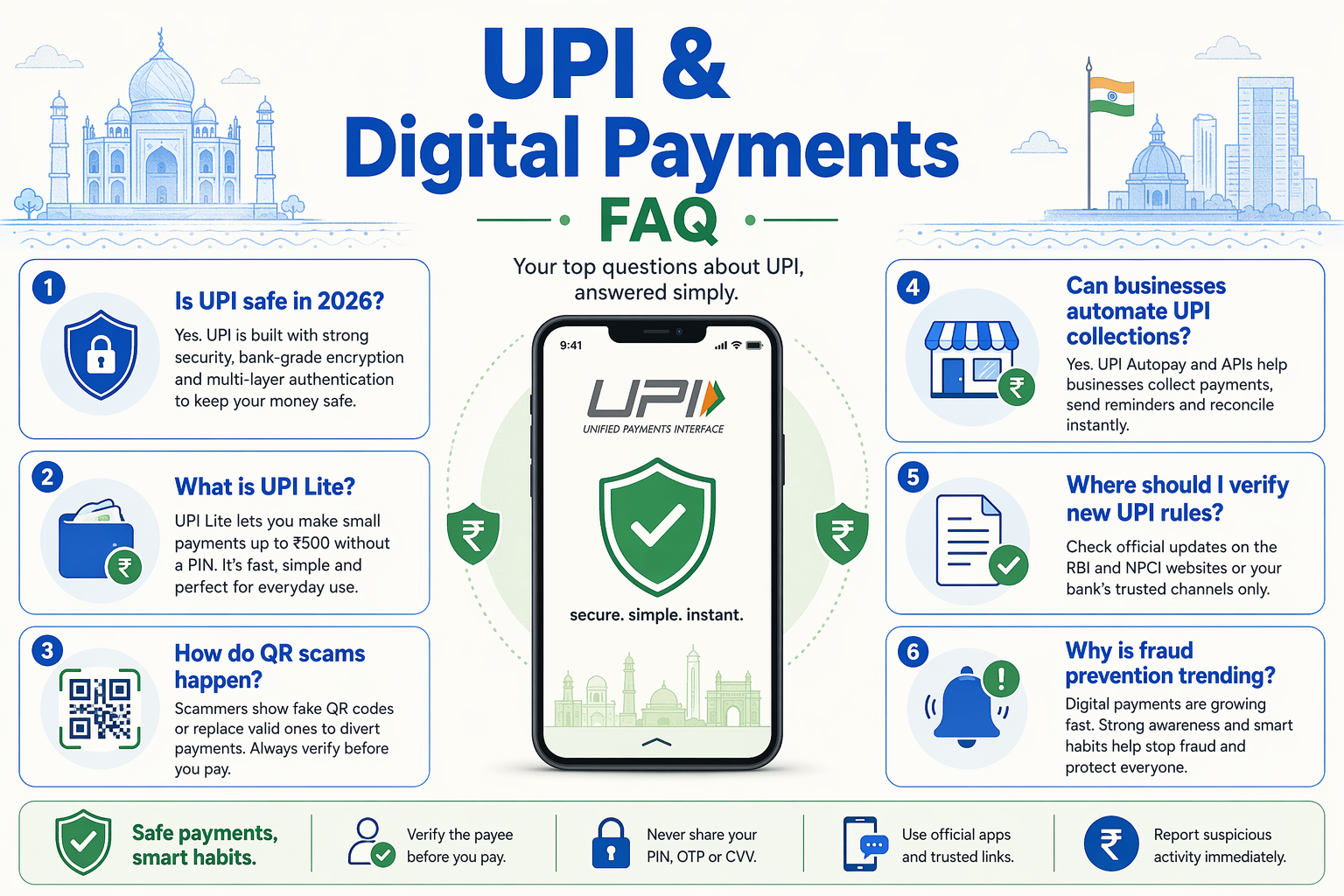

Frequently Asked Questions

What is the biggest 2026 opportunity in UPI & Digital Payments in India?

Are UPI payments safe in 2026?

What are the latest UPI new rules in 2026?

How can small businesses automate UPI collections and customer communication?

Why are UPI & Digital Payments in India important for merchants beyond QR codes?

What fraud risks should users know about in UPI & Digital Payments in India?

Conclusion

India’s UPI story in 2026 is no longer just about faster payments—it is about building faster, safer, more automated businesses on top of real-time digital rails.

Key takeaways:

- Speed has become the default: UPI has turned instant payments into an everyday habit, from QR codes to mobile-number transfers and emerging conversational payment flows.

- Safety is now central to growth: NPCI’s AI/ML-based fraud-monitoring solution, highlighted by PIB, shows how fraud detection is becoming infrastructure-level, especially as phishing, impersonation, mule accounts, and synthetic identities rise.

- Rules are tightening: From April 2025 restrictions on saved/shared QR codes for international UPI payments to expected stronger security from April 1, 2026, the ecosystem is moving toward more verified transactions.

- Automation is the next opportunity: Reconciliation, refunds, collections, customer support, WhatsApp commerce, and payment-linked workflows are where businesses can unlock the next wave of efficiency.

What to watch next: how conversational UPI, credit-on-UPI, UPI Lite, and AI-powered support reshape customer journeys. To stay ahead, explore CallMissed, an AI infrastructure platform powering voice agents, WhatsApp chatbots, and multilingual business communication. The real question is: will your business only accept digital payments—or automate around them?

Related Posts

Ready to automate customer conversations?

Launch AI voice agents and WhatsApp bots with CallMissed — one API, 22+ Indian languages.