India’s Startup Boom: Record Growth & Deep-Tech Momentum

In a year when global venture capital pulled back sharply, India achieved something that defies conventional wisdom: the government recognized a record...

India’s Startup Boom: Record Growth & Deep-Tech Momentum

In a year when global venture capital pulled back sharply, India achieved something that defies conventional wisdom: the government recognized a record 55,200 startups in FY26, marking a 44% year-on-year surge, even as overall startup funding contracted by 26% during the same quarter. That tension—between explosive registration growth and a tighter capital environment—captures exactly why India’s startup boom has become the world’s most closely watched entrepreneurial experiment. This is no longer just a story of discount-driven consumer apps and quick-commerce delivery wars; it is a fundamental economic transformation that has taken the ecosystem from fewer than 500 startups in 2014 to over 190,000 registered by 2025, catapulting India to the rank of the world’s third-largest startup hub with 100+ unicorns and a combined valuation exceeding $700 billion.

What makes this inflection point truly historic, however, is not merely

Introduction

India’s startup ecosystem has entered a new phase of hyper-growth and structural transformation. In Fiscal Year 2026 alone, the country recognized a record 55,200 startups—a figure that cements India as one of the world’s most prolific incubators and follows a reported 44% year-on-year growth trajectory in new registrations. Yet this extraordinary volume tells only part of the story. In the same quarterly window, overall startup funding contracted by 26% year-on-year, underscoring a critical inflection point: India’s startup boom is no longer defined merely by capital abundance or speculative growth, but by the maturity, operational resilience, and increasingly sophisticated technological orientation of its founders.

To grasp the sheer scale of this shift, consider the longitudinal data. According to the Observer Research Foundation (ORF), India went from fewer than 500 startups in 2014 to over 190,000 registered by 2025. This trajectory has positioned the nation as the third-largest startup ecosystem globally, with major milestones including:

- 100+ unicorns and a combined valuation exceeding $700 billion built over the last decade (KPMG)

- A near 400-fold increase in registered startups between 2014 and 2025

- Record-breaking 55,200 new recognitions in FY26, marking the fastest annual incubation rate to date

What began as a wave of consumer internet aggregators and horizontal SaaS platforms has evolved into a far more foundational, infrastructure-grade movement.

DeepTech and AI Take Center Stage

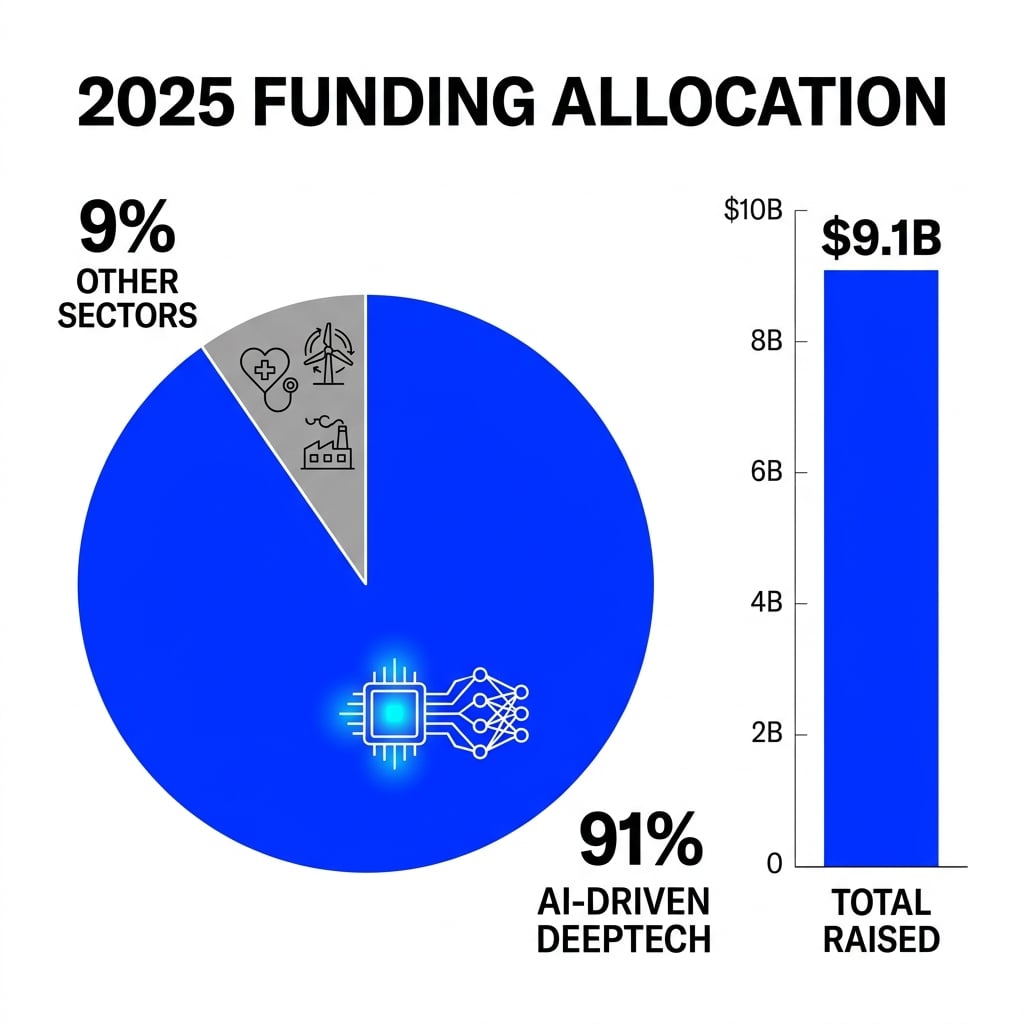

Perhaps the most consequential evolution in this funding cycle is the decisive pivot toward deep-tech and artificial intelligence. Indian technology startups raised $9.1 billion in 2025, marking a robust 23% year-on-year increase, with artificial intelligence alone accounting for a staggering 91% of all deep-tech investments. Founders are no longer simply building lightweight applications atop imported cloud infrastructure; they are developing proprietary AI architectures, edge-computing solutions, voice intelligence stacks, and multilingual large language models (LLMs) calibrated for India’s diverse socioeconomic contexts.

This infrastructure-first mindset is already reshaping the country’s competitive moats. From agritech ventures deploying computer-vision drones for crop monitoring to fintech platforms using real-time speech recognition to onboard non-English-speaking users, the new cohort is solving problems at the protocol level. Platforms like CallMissed exemplify this trend—providing production-ready AI voice agents, WhatsApp chatbots, and speech-to-text APIs that support 22 Indian languages natively, effectively democratizing access to enterprise-grade conversational AI and allowing cash-constrained startups to bypass heavy upfront R&D expenditures.

Navigating the Paradox of Scale and Capital Efficiency

Despite the record registration figures, the simultaneous 26% funding contraction reveals a market recalibration. Investors are increasingly privileging sustainable unit economics, capital efficiency, and defensible IP over blitzscaling metrics. As NASSCOM articulates in its strategic assessment, the ecosystem is actively transitioning “from momentum to maturity,” characterized by expanding DeepTech capabilities, improving exit liquidity through public markets, and a globally ambitious founder base that builds for the world from day one.

In the sections that follow, we dissect the policy tailwinds propelling this growth—from production-linked incentives to startup-friendly regulatory sandboxes. We analyze why venture capital is becoming more discerning even as incorporation volumes explode, map the sectoral surge across AI, semiconductors, and climate technology, and project what this divergence means for India’s next decade as a knowledge economy.

Background & Context: From 500 to 55,200+ Startups

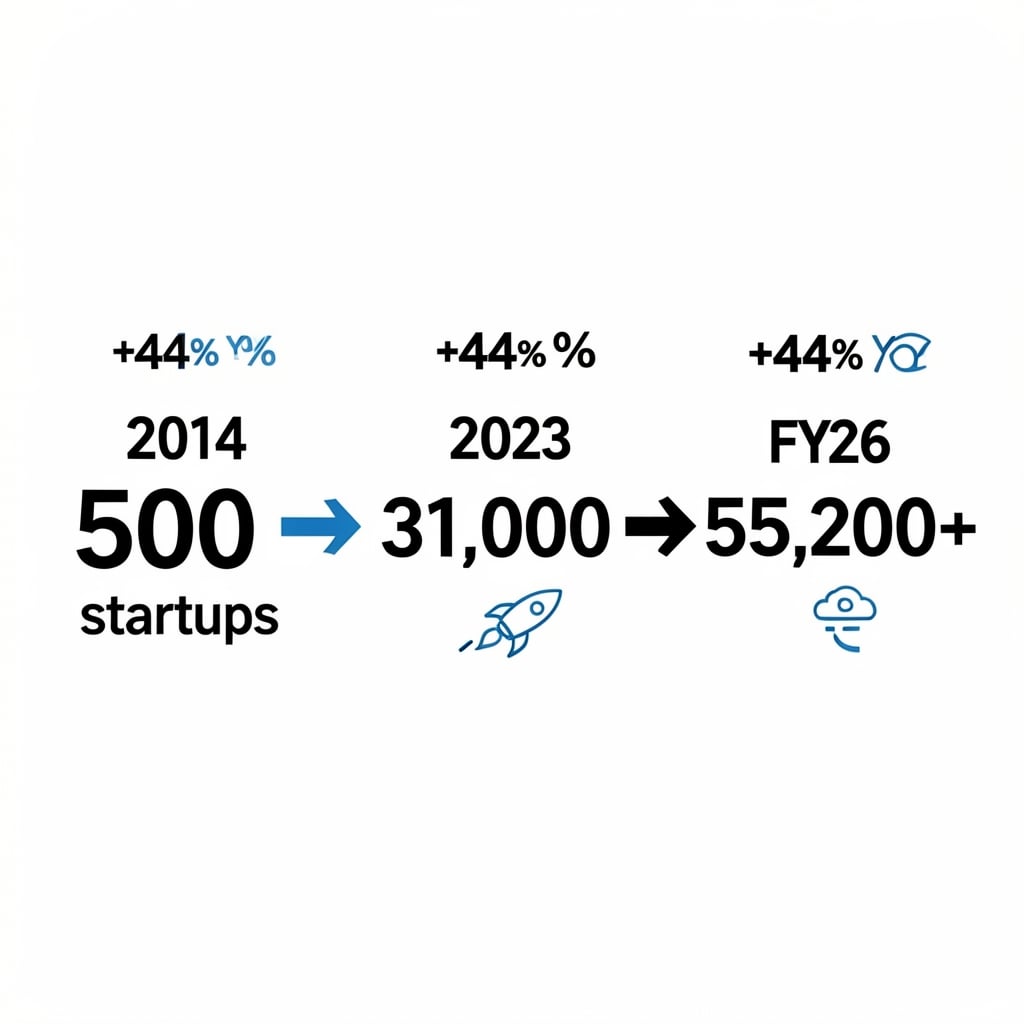

India's startup ecosystem has undergone one of the most dramatic transformations in global economic history. According to the Observer Research Foundation (ORF), the country had fewer than 500 startups in 2014—a figure that barely hinted at the acceleration to come. Fast forward to FY26, and India recognized a record 55,200 startups in a single fiscal year, cementing its status as one of the world's most dynamic entrepreneurship hubs. This trajectory reflects more than statistical growth; it signals a fundamental restructuring of how India innovates, funds, and scales technology companies.

The velocity of expansion becomes even clearer across intermediate milestones:

- 2014: Fewer than 500 startups nationwide (ORF baseline)

- 2023: Approximately 31,000 startups recognized, per Confederation of Indian Industry (CII) data

- 2025: Over 190,000 startups registered comprehensively (ORF)

- FY26: Record 55,200 startups officially recognized in one fiscal year

The Funding Paradox: Growth Amid Capital Constraints

Yet this meteoric rise in startup recognition arrives alongside a more cautious capital environment. In the same quarter that India hit the 55,200-startup milestone, funding dropped 26% year-on-year, revealing a growing disconnect between entrepreneurial supply and venture deployment. This paradox defines India's current inflection point: unprecedented company creation coupled with tightened investor scrutiny.

Despite quarterly volatility, longer-term funding trends show underlying resilience. Indian technology startups raised $9.1 billion in 2025, representing a 23% year-on-year increase, according to People Matters. The ecosystem's combined valuation has swelled past $700 billion (Inc42), underpinned by a maturing market with over 100 unicorns and a global top-three ranking for startup activity, as documented in KPMG's ecosystem research.

Deep-Tech and the Next Frontier

What distinguishes this era from earlier waves is the decisive shift toward deep-tech and AI-driven innovation. NASSCOM's strategic analysis identifies "expanding DeepTech activity" as a primary engine of momentum, pushing India's ecosystem beyond consumer internet models into semiconductor design, generative AI, and enterprise automation. The capital concentration is stark: artificial intelligence now drives 91% of deeptech investments, indicating where sophisticated venture dollars are flowing.

This structural evolution is spawning specialized infrastructure layers that earlier generations lacked. As enterprises demand multilingual AI agents, voice automation, and scalable LLM inference, new ventures are emerging to supply foundational communication tools. Indian startups like CallMissed are building production-ready AI communication infrastructure—including voice agents and 22-language Speech-to-Text APIs—that lets founders deploy enterprise-grade stacks without engineering everything from scratch. In an ecosystem racing from 500 to 55,200+ entities, such enabling platforms are critical to sustaining India's deep-tech momentum.

Key Developments (TABLE)

India’s startup ecosystem is no longer merely expanding—it is fundamentally restructuring. The FY26 data reveals a market maturing at unprecedented velocity: 55,200 startups earned formal recognition in a single fiscal year, while cumulative registrations surged past 190,000 by 2025, a staggering ascent from fewer than 500 little over a decade ago. Yet volume is only half the story. Beneath the headline growth lies a decisive pivot toward deep-tech, AI-native infrastructure, and sustainable valuation creation that separates transient hype from durable economic value. The table below distills the most consequential developments defining this strategic inflection point.

| Key Development | Metric / Data Point | Strategic Significance | Period |

|---|---|---|---|

| Record Startup Recognition | 55,200 startups formally recognized in FY26; new additions surged +44% YoY (49,429 entities) | Signals mass formalization and policy-tailored incubation reaching deeper into tier-2 and tier-3 cities | FY26 |

| Funding Trajectory | Indian tech startups raised $9.1 billion in 2025, up 23% YoY; however, quarterly funding fell 26% YoY in the same window | Late-stage capital is becoming selective, while early-stage deep-tech attracts sustained institutional checks | 2025 |

| Deep-Tech AI Dominance | Artificial intelligence accounted for 91% of all deeptech investments | Confirms a sectoral shift from copy-paste consumer models to proprietary AI and infrastructure R&D | 2025 |

| Ecosystem Scale & Global Rank | 190,000+ registered startups by 2025; ecosystem ranks 3rd globally with 100+ unicorns | India has transitioned from an emerging satellite market to a top-tier startup superpower | 2014–2025 |

| Decade-Long Valuation Build | Combined startup valuation crossed $700 billion+ over the last decade | Long-term wealth and IP creation now rival traditional industrial economy outputs and deepen exit liquidity | Last decade |

| Historical Growth Arc | Active startups grew from 2,000 (2014) to 31,000 (2023)—a 15x expansion in under a decade | Demonstrates non-linear acceleration once regulatory, capital, and digital infrastructure aligned | 2014–2023 |

What the Numbers Reveal

The juxtaposition of record registrations and volatile funding is not contradictory—it is diagnostic. The 26% quarterly drop in capital deployment (per FY26 data) alongside the 23% annual funding increase to $9.1 billion suggests investors are consolidating around high-conviction bets rather than spraying capital indiscriminately across sectors. Winners are attracting larger, more structured rounds; the rest now face a markedly tighter diligence filter where unit economics and technical moats matter more than growth-at-all-costs narratives.

The 91% AI share of deeptech deals is the clearest signal yet that India’s next unicorns will be built on proprietary models, not marketplace aggregation. This is precisely where communication and inference infrastructure become mission-critical. Platforms such as CallMissed exemplify the new enabling layer: by offering a multi-model API gateway with 300+ LLMs, multilingual Speech-to-Text spanning 22 Indian languages, and production-ready voice agents, they allow resource-constrained startups to deploy frontier AI without incurring heavy capex. The result is a democratized deep-tech pipeline that feeds directly into the FY26 growth narrative.

Policy Tailwinds and Structural Maturity

Several non-financial factors undergird the table’s headline metrics:

- Regulatory recognition of 55,200+ startups unlocks tax exemptions, self-certification compliance, and preferential public procurement access.

- A global top-three ranking means India now competes with the U.S. and China for talent retention and R&D centers, not merely cost arbitrage.

- The $700 billion+ valuation base indicates that exit markets—IPOs, M&A, and secondary sales—are deepening, effectively recycling risk capital back into seed-stage funds.

Looking ahead, the startups that scale in FY27 will likely be those that treat AI infrastructure as a utility rather than a science project. With foundational platforms handling the inference stack and multilingual communication layers, India’s 190,000-plus founders can focus on domain-specific breakthroughs—propelling the next wave from statistical boom to sustained industrial maturity.

In-Depth Analysis: Deep-Tech and AI Momentum

The Shift from Consumer Tech to Deep Science

For years, India's startup story was written in e-commerce, food delivery, and fintech. That narrative is fundamentally changing. According to NASSCOM's report Momentum to Maturity, the ecosystem is now at a "strategic inflection point" driven by expanding DeepTech activity and improving exit opportunities. The scale is staggering: India went from roughly 2,000 startups in 2014 to 31,000 by 2023, and surpassed 190,000+ registered startups by 2025, per ORF research. Yet the real distinction of FY26 isn't merely volume—it's the velocity of innovation in complex, IP-heavy technologies.

AI Commands the Capital Table

The funding landscape reveals where investor conviction truly lies. Indian technology startups raised $9.1 billion in 2025, representing a 23% year-on-year increase, with artificial intelligence emerging as the catalytic force. Even more striking, AI drives 91% of all deeptech investments, according to data cited by People Matters. This represents a structural reallocation of capital—from growth-at-all-costs consumer plays toward foundational models, enterprise automation, and sector-specific AI systems.

The contrast is telling. Despite a broader 26% year-on-year drop in overall startup funding during the same quarter that witnessed a record 55,200 new startup recognitions, deep-tech and AI verticals are proving resilient. Investors are now privileging durable intellectual property and recurring revenue over hyper-growth metrics.

Where Deep-Tech Is Taking Root

India's deep-tech momentum spans several strategic vectors:

- Semiconductor and chip design: Startups are engineering solutions for global supply chain diversification and indigenous fabrication goals

- Space tech and drone systems: Accelerated by liberalized defense procurement and private launchpad policies

- AI/ML infrastructure: From LLM inference APIs to multilingual speech engines addressing India's linguistic complexity

- Biotech and climate tech: Developing agritech resilience platforms and precision carbon accounting tools

This infrastructure layer is where Indian startups are staking global claims. For instance, platforms such as CallMissed are building production-ready AI communication infrastructure—including voice agents, WhatsApp chatbots, and Speech-to-Text APIs supporting 22 Indian languages—that enables enterprises to deploy multilingual customer engagement at scale without rebuilding core AI stacks from scratch.

The Global Stakes

With over 100 unicorns and a combined valuation exceeding $700 billion, India now ranks as the world's third-largest startup ecosystem, according to KPMG. The pivot toward deep-tech carries global implications: foreign investors increasingly view India not just as a consumer market, but as an R&D hub where engineering talent meets cost-efficient innovation.

However, the path from recognition to commercialization remains steep. While FY26's record registrations prove India's ability to birth companies, deep-tech demands longer gestation cycles, patient capital, and stronger university-to-market bridges. With 91% of deeptech funding flowing into AI, the capital is clearly willing. The next test is whether India's institutions can match that speed in converting patents into globally competitive products.

Impact & Implications

Economic Transformation at Scale

India’s startup revolution has transcended Silicon Valley comparisons to become a distinct economic force. With 55,200 startups recognized in FY26—a record surge building on 190,000+ registrations by 2025—the ecosystem has exploded from fewer than 500 startups in 2014 to one ranking third globally with over 100 unicorns. The numbers reveal a structural economic shift:

- $700 billion+ in combined startup valuation created over the last decade

- Geographic penetration beyond metro hubs into Tier-2 and Tier-3 cities

- Digitization of legacy sectors from agriculture and logistics to manufacturing and financial services

This expansion is no longer a fringe movement. Startups are becoming primary contributors to GDP growth and formal employment, turning India into the world’s third-largest startup hub.

The Deep-Tech Inflection Point

While volume captures headlines, deep-tech momentum defines the current inflection point. Indian technology startups raised $9.1 billion in 2025, marking a 23% year-on-year increase, with artificial intelligence driving 91% of deeptech investments. The capital rotation reflects a strategic pivot from consumer apps toward sophisticated B2B and infrastructure plays:

- Semiconductor design and chip innovation

- Climate tech and sustainable engineering

- AI-native enterprise tools and multilingual communication stacks

Crucially, Indian startups are no longer just consuming AI; they are deploying it at scale across voice, text, and regional languages. Platforms like CallMissed exemplify this infrastructure layer—offering production-ready AI voice agents, WhatsApp chatbots, and speech-to-text APIs across 22 Indian languages that let deep-tech founders integrate sophisticated communication stacks without building from scratch.

Capital Contradictions and Signals of Maturity

Yet, the boom carries internal tensions. Despite the record 55,200 startup recognitions, funding dropped 26% year-on-year in the same FY26 quarter. This divergence—more startups, tighter capital—suggests the ecosystem is entering a maturity phase where investor discipline replaces indiscriminate growth bets. According to NASSCOM’s analysis, the ecosystem has reached a strategic inflection point, where sustainable success now depends on stronger exit opportunities, clearer monetization pathways, and robust unit economics.

For founders, the implication is clear: capital-efficient innovation now outranks growth-at-all-costs. The startups thriving in this environment are leveraging India’s cost arbitrage while solving globally relevant problems through proprietary deeptech IP, LLM inference infrastructure, and domain-specific automation.

Global Competitiveness and Strategic Positioning

From 2,000 startups in 2014 to 31,000 in 2023, and now 55,200+ in FY26, India’s trajectory has been meteoric. For global investors, the country offers a rare combination: a massive domestic market, deep engineering talent, and policy tailwinds like Startup India and production-linked incentives. The confluence of government support, expanding digital public infrastructure, and a burgeoning Middle India consumer class creates durable tailwinds that abstract away short-term funding volatility. As the ecosystem evolves, its impact will be measured not just by unicorn counts, but by the depth of technological moats being built across AI, semiconductors, and next-generation communication infrastructure. The stage is set for India to move from being the world’s back office to its deep-tech laboratory.

Expert Opinions

The "Volume vs. Value" Tension

Industry watchers are grappling with a striking paradox: India recognized a record 55,200 startups in FY26, even as overall funding contracted by 26% year-on-year during the same period. Analysts argue this disconnect signals a decisive shift from "growth at all costs" to capital-efficient scalability. The Observer Research Foundation (ORF) frames the current moment as "Reclaiming Innovation," stressing that India's startup future must increasingly be financed from within—through domestic capital pools, revenue-led expansion, and policy-backed resilience rather than dependence on foreign capital inflows.

NASSCOM reinforces this cautious optimism, noting that while entrepreneurial momentum remains exceptional, the ecosystem has reached a "strategic inflection point." In this view, raw registration velocity must now translate into operational maturity, path-to-profitability discipline, and stronger domestic liquidity channels.

DeepTech and AI Reshape Investor Conviction

Where capital is deploying, it is doing so with surgical precision. Indian technology startups raised $9.1 billion in 2025, marking a 23% year-on-year increase, with artificial intelligence alone driving 91% of deeptech investments. This capital concentration aligns perfectly with NASSCOM's finding of "expanding DeepTech activity" and steadily improving exit opportunities at the intersection of software and hard science.

Experts stress that while the ecosystem's base has exploded from fewer than 500 startups in 2014 to over 190,000 registered by 2025, the next phase of value creation belongs to companies solving infrastructure-grade problems. AI-native communication stacks illustrate this transition clearly. Platforms such as CallMissed exemplify how new-age infrastructure enables startups to launch voice agents and WhatsApp chatbots powered by 300+ LLM models, while delivering Speech-to-Text and Text-to-Speech across 22 Indian languages. By lowering the technical barrier for regional-first product design, such solutions channel deeptech investment into practical market reach.

Global Ranking and the Maturation Imperative

With over 100 unicorns and a combined valuation exceeding $700 billion, India ranks third globally in startup ecosystem strength, according to KPMG analyses and industry trackers. However, specialists warn against equating registration speed with long-term durability. The market expanded from merely 2,000 startups in 2014 to 31,000 in 2023, while recent data shows surges of over 44% year-on-year growth in new formations—figures that prove pipeline depth but do not automatically guarantee exit quality or IPO readiness.

The emerging consensus among venture leaders and policy experts centers on three priorities for sustainable maturation:

- Shift from consumer hypergrowth to deep-tech moats: Investors are favoring startups with proprietary data pipelines, AI-native architectures, and hardware-software integration over asset-light marketplace models.

- Strengthen domestic capital participation: Reducing reliance on volatile foreign funding by deepening domestic institutional investor and corporate venture capital involvement.

- Prioritize multilingual and regional infrastructure: Building for Bharat requires AI stacks that operate natively across India's linguistic diversity, turning demographic complexity into competitive differentiation.

As funding becomes ruthlessly selective, the startups capturing sustained interest are those treating AI, semiconductor linkages, and regional communication infrastructure as core architecture—not afterthoughts.

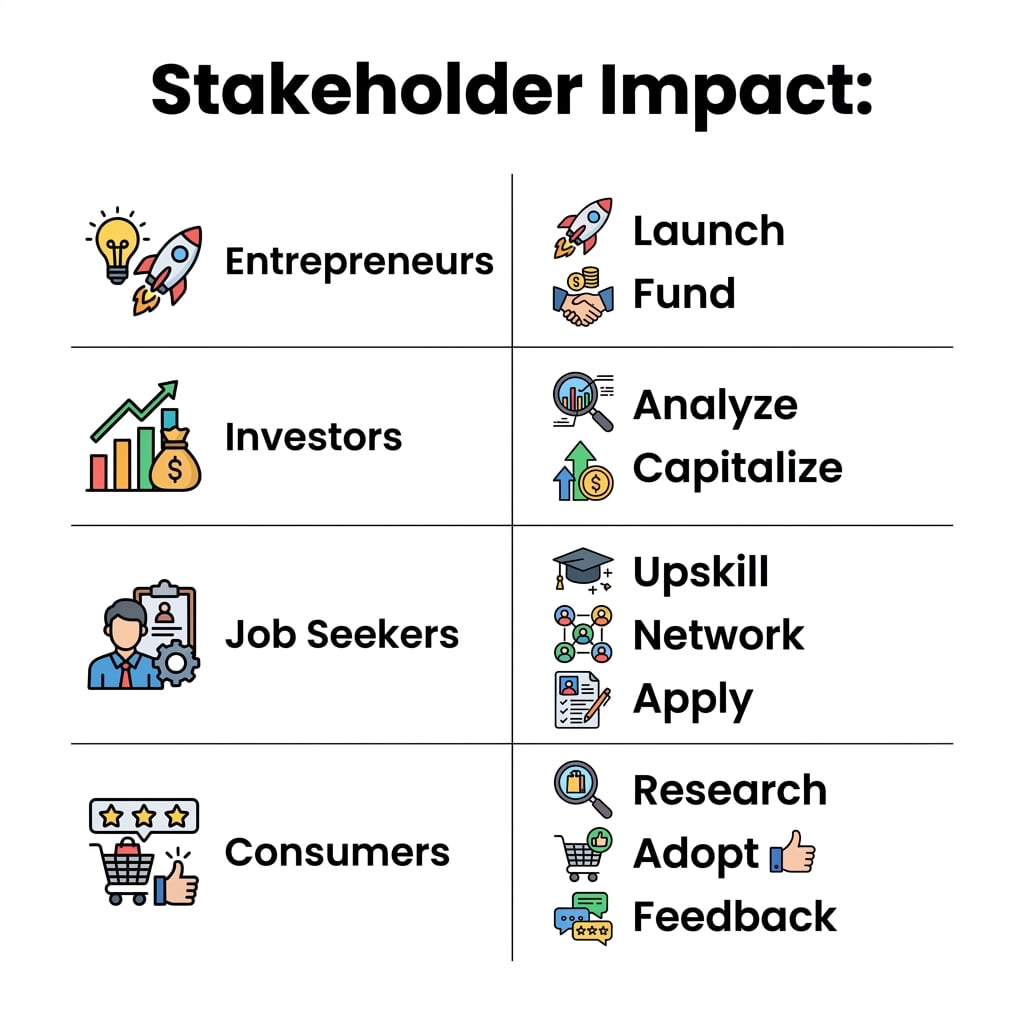

What This Means For You (TABLE)

The numbers are loud, but the signal matters more than the noise. With 55,200 startups officially recognized in FY26—a record—and the ecosystem swelling to over 190,000 registered startups by 2025, India's market is no longer emerging; it is the primary arena. Yet that same quarter revealed a 26% year-on-year drop in funding, a clear warning that capital is reallocating toward quality and real technology, not just pitch decks. Whether you are building, backing, buying from, or joining these ventures, the playbook has changed.

The Stakeholder Playbook for FY26

| Stakeholder | What the FY26 Data Signals | Your Strategic Imperative | Key Trend to Ride |

|---|---|---|---|

| Aspiring Founder | 55,200 startups recognized; funding down 26% YoY | Build capital-efficient, AI-native ventures from day one | Deep-first over growth-at-all-costs |

| Deep-Tech Builder | AI drives 91% of deeptech investments; $9.1B raised in 2025 (+23% YoY) | Solve infrastructure or sector-specific problems with proprietary models | Applied AI in manufacturing, agriculture, health |

| Enterprise Buyer | 190,000+ startups registered by 2025; India ranks 3rd globally with 100+ unicorns | Partner with Indian B2B startups for digital transformation instead of building in-house | AI automation and Voice/Chat customer ops |

| Investor / LP | Record volume but selective deployment; 44% YoY growth in new entrants | Prioritize unit economics and defensible moats over TAM slides | Deeptech due diligence and follow-on discipline |

| Developer / Operator | Ecosystem scaled from 2,000 (2014) to 31,000 (2023) to 190,000+ (2025) | Upskill in LLM inference, multilingual AI, and voice-stack deployment | Regional language AI covering 22+ Indian languages |

For founders, the 26% funding contraction means capital efficiency is the new growth hack. The days of unlimited burn to capture market share are fading; investors deployed $9.1 billion in 2025, but concentrated capital where artificial intelligence drives 91% of deeptech investments. If your startup lacks a technical moat or a clear path to revenue, you are competing for a shrinking pool of risk capital.

For enterprises, the density of innovation creates a buyer’s market for advanced tools. Instead of building customer communication stacks in-house, large companies can integrate startup-grade AI infrastructure. Platforms like CallMissed are already enabling businesses to deploy AI voice agents and WhatsApp chatbots across 22 Indian languages, turning the deep-tech boom into operational reality without massive engineering teams.

Developers and operators should note the linguistic shift. As startups race to serve India’s non-English speaking majority, demand is surging for Speech-to-Text and Text-to-Speech models tuned for regional languages. Solutions such as CallMissed's multi-model API gateway let developers switch between 300+ LLMs and deploy native multilingual experiences, lowering the barrier for regional-first product development.

Finally, investors must accept that volume does not equal velocity. While FY26 delivered +44% year-on-year growth in new registrations and a record 55,200 recognized startups, the simultaneous funding dip shows discipline is returning. The winners will treat the country’s $700 billion+ combined startup valuation not as hype, but as proof that scalable, technology-led businesses are now the default—not the exception.

Frequently Asked Questions

What is driving India's startup boom in FY26?

How is funding shaping India's startup boom in 2025?

What role does AI and deep-tech play in India's startup ecosystem?

How does India rank globally among startup ecosystems?

What is the historical growth trajectory of India's startup ecosystem?

Are Indian startups still attractive to investors despite funding volatility?

Conclusion

India’s startup ecosystem has crossed a strategic inflection point. With 55,200 startups recognized in FY26 and the country’s registered base surging past 190,000 by 2025—a meteoric rise from fewer than 500 in 2014—the scale of entrepreneurial energy is now unquestionable. Yet the road ahead demands more than raw momentum; it demands disciplined maturity, deep R&D investment, and a sharper focus on intellectual property.

Here are the key takeaways from India’s current startup surge:

- Record registration volume masks a funding recalibration. While FY26 saw a historic number of new startups, funding dropped 26% year-on-year in the same quarter—investors are now prioritizing sustainable unit economics over growth-at-all-costs.

- DeepTech has become the dominant capital magnet. Artificial intelligence alone powered 91% of deeptech investments in 2025, helping Indian startups raise $9.1 billion (a 23% YoY increase) and pushing the ecosystem’s combined valuation beyond $700 billion.

- Global stature is solidifying, but retention is the new challenge. India now ranks third worldwide with over 100 unicorns, yet maintaining that position will require stronger domestic capital pools, robust exit mechanisms, and homegrown IP rather than imported playbooks.

- The widening gap between registration volume and tighter capital access suggests that the next decade will favor startups solving hard infrastructure problems—from semiconductor design to multilingual AI stacks—instead of pure consumer-market aggregators.

Looking ahead, the critical narrative to watch is whether India can convert this registration boom into a deep-tech manufacturing and product-leadership base. As global capital increasingly flows toward AI, climate tech, and advanced robotics, the startups that build proprietary models and own their supply chains will define India’s next cohort of unicorns.

To explore how AI communication infrastructure is evolving alongside this deep-tech wave, check out CallMissed—an AI platform powering voice agents and multilingual chatbots that helps businesses scale customer engagement across India’s linguistic diversity.

The question is no longer whether India can produce startups at scale. It is whether the ecosystem can build the next generation of globally competitive, IP-led technology companies. Will your business be a consumer of that future—or a creator of it?

Discussion

Related Posts

Ready to automate customer conversations?

Launch AI voice agents and WhatsApp bots with CallMissed — one API, 22+ Indian languages.