Embodied AI: Robots, Physical Reasoning, and 2026 Reality

A 2026 grounded look at embodied AI — Figure $39B, Tesla Optimus, 1X NEO, vision-language-action models, what is working, and what is still hard.

Embodied AI in 2026 is in an awkward middle place — past the YouTube-demo phase, well short of the "robots in every home" pitch decks. Funding is enormous, capability progress is real, and the gap between staged demos and reliable autonomous operation remains larger than the marketing suggests. Here is a grounded look at where the field is.

The companies and their valuations

A handful of humanoid robotics companies dominate the conversation:

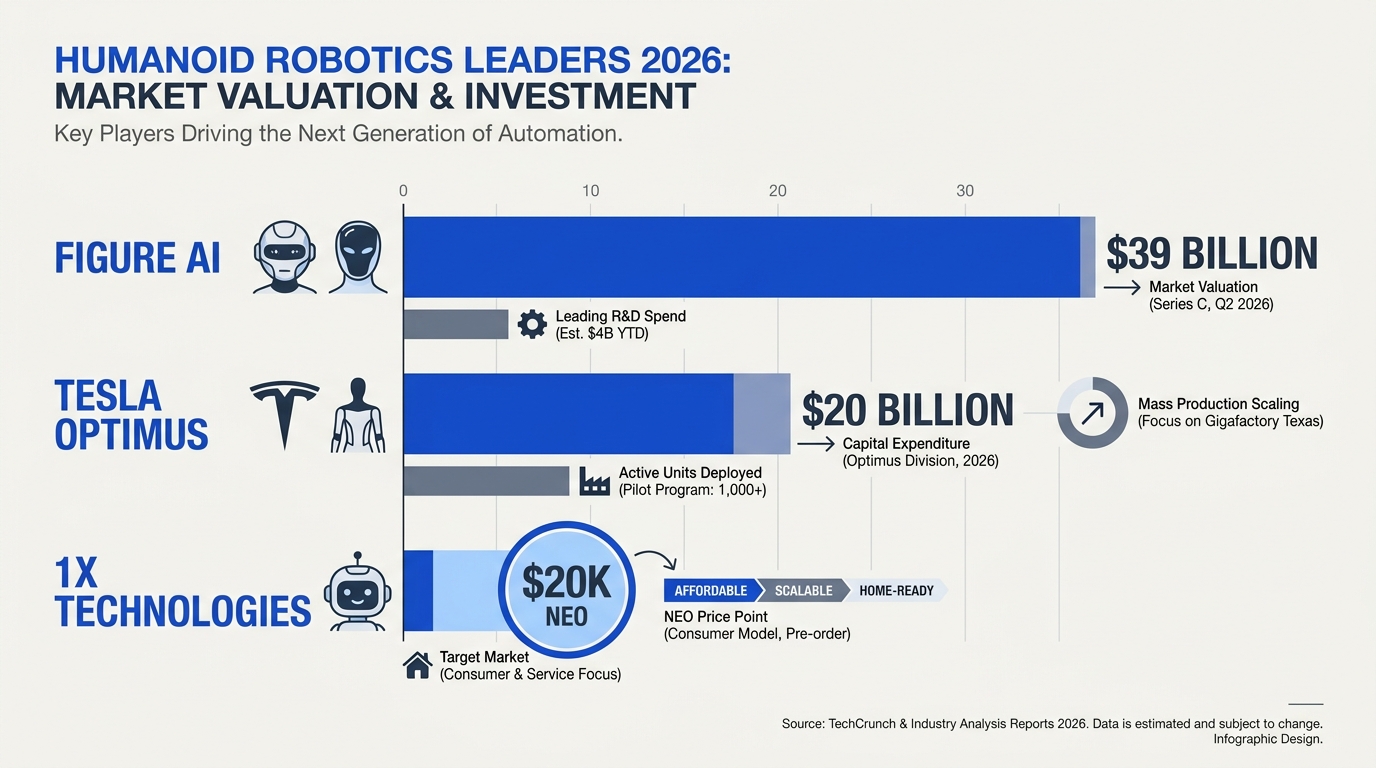

- Figure AI — valued at $39 billion after raising $1B in September 2025, per reporting on the funding round. Focused on commercial/industrial humanoid robots.

- Tesla Optimus — self-funded by Tesla, with $20B in 2026 capex covering manufacturing and compute. Production lines targeting 1M units/year at Fremont, with Gigafactory Texas planned for 10M units/year starting 2027 [per Tesla's stated production plans].

- 1X Technologies — focused on home robotics with the NEO humanoid (66 lb, 4-hour battery, $20K or $499/month pre-order).

- Chinese leaders — Unitree, AgiBot, UBTech, and Fourier produce humanoids at lower price points, with significant domestic market traction.

Numbers are large; deployments at meaningful scale remain limited. Most public demos involve significant tele-operation or scripted environments. [Inference]

What's working

Real capability progress in 2026:

Vision-language-action (VLA) models

The dominant architecture for general-purpose robotic policies. Take a vision-language foundation model, fine-tune on robot trajectories, output continuous control. Models like Google's RT-2 line and successors have shown that web-scale vision-language pretraining transfers to robot tasks. Performance is meaningful; absolute reliability for unstructured environments is still well below human.

Dexterous manipulation

Bimanual dexterous tasks (folding clothes, plugging cables, peeling fruit) that were impossible for general-purpose robots in 2020 are demonstrated by 2026, often with hours of teleoperated training data per task. Generalization across tasks remains the bottleneck.

Locomotion

Bipedal walking, running, and stair-climbing are roughly solved on flat-ish terrain. Robust outdoor mobility — uneven ground, slopes, slippery surfaces — is harder but progressing.

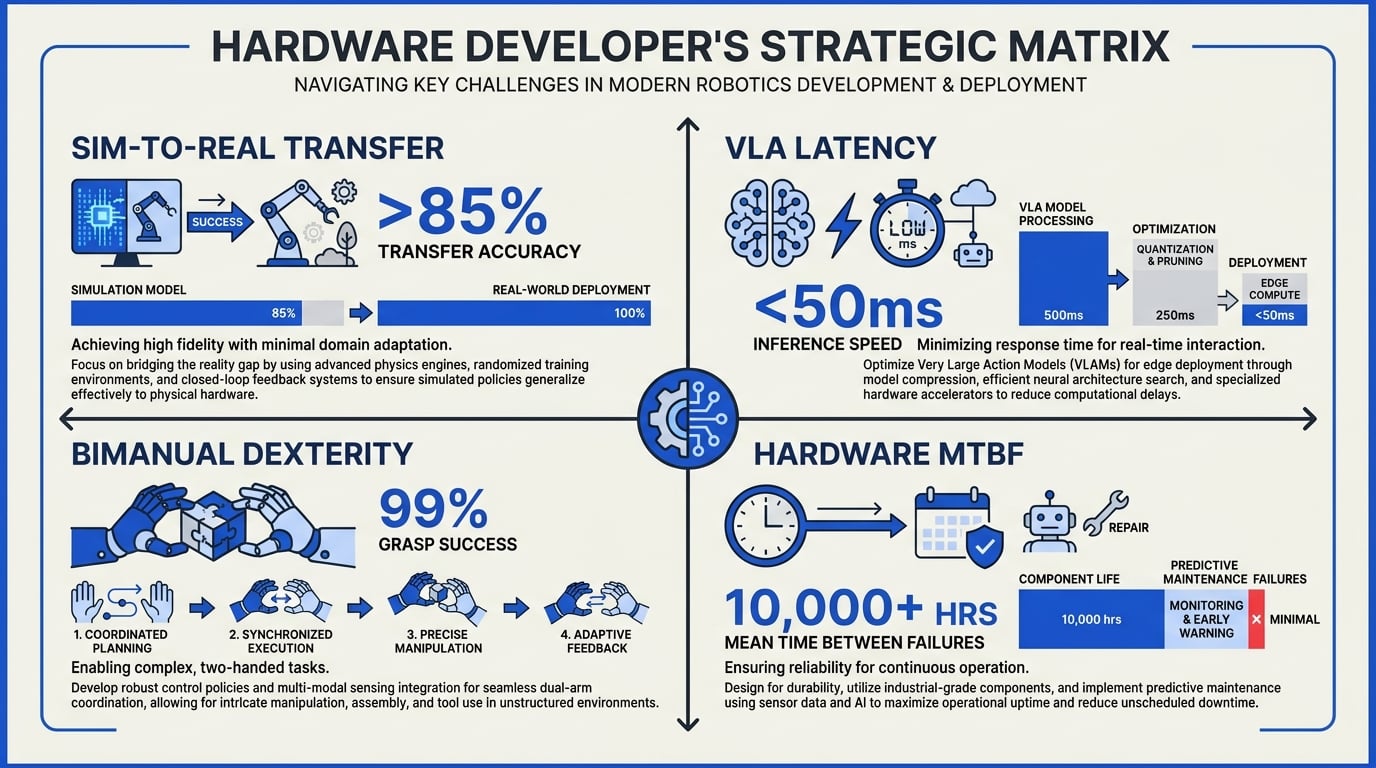

Sim-to-real transfer

Training in simulation and deploying on hardware works for many tasks now; domain randomization, simulation-real gap closing techniques, and large-scale simulation are mature.

What's still hard

The real bottlenecks:

Long-horizon autonomous tasks

Pick up the laundry basket, walk to the laundry room, open the machine, load the clothes, add detergent, start the cycle, return. Each sub-task is achievable in isolation; chaining 10+ sub-tasks across a real home with reliability is not. Compounding error rates make the end-to-end probability of success low.

Safety in human-shared spaces

A humanoid robot near a person is a safety problem. Physical safety standards for in-home humanoids are still being developed. Insurance, liability, and regulatory frameworks have not caught up.

Battery and compute density

A useful in-home humanoid needs all-day operation. Current batteries hit roughly 4-hour runtime. Onboard compute for VLA models pulls power and adds weight. The hardware fundamentals are not yet at the operating point.

Cost

A capable humanoid in 2026 sits in the $20-50K price range for early units. To displace a household appliance market, the price needs to come down 5-10x. The path is plausible (volume manufacturing, component cost reduction) but not yet realized.

Data

VLA models need orders of magnitude more robot trajectory data than is publicly available. Companies invest heavily in teleoperation data collection, but per-task data costs remain a moat that limits new entrants.

What you can actually buy or use

A 2026 reality check on availability:

- Industrial humanoid robots are starting commercial pilots — Figure with BMW, Apptronik with Mercedes, Agility Robotics with various logistics customers. Pilots are real; productionized fleets at scale are limited.

- 1X NEO is available for pre-order in select markets; volumes and capabilities are limited.

- Tesla Optimus public sales target late 2027 [per Tesla's stated timeline].

- Quadruped robots (Boston Dynamics Spot, Unitree Go2/B2) are available and deployed for inspection, security, and research.

- VLA model training — Google's Gemini Robotics models, Physical Intelligence's pi-0, NVIDIA's GR00T are increasingly available to research and commercial customers.

If you are a builder integrating embodied AI in 2026, the practical entry points are quadrupeds for inspection and arms for industrial manipulation — not humanoids in homes.

The factory-first thesis

Multiple companies — Tesla, Figure, Apptronik, Agility — are pursuing factory deployment first, then logistics, then office, then home. The reasoning: factories are structured environments with tolerances of error humans monitor and tasks that justify high-cost hardware. The capability ladder there is well-defined; the home is much harder.

This thesis predicts useful, deployed humanoid robots in industrial settings within the next 2-3 years and broader deployment delayed by 5+ years. [Speculation — based on stated company strategies]

Where Chinese competitors fit

Unitree, AgiBot, and others ship at significantly lower price points (often $10-20K for capabilities that Western companies price at $30-50K) and have access to large domestic deployment opportunities. The competitive picture is real and shapes how Western humanoid pricing evolves.

What a builder should track

If you are watching embodied AI as a builder:

- VLA architecture progress. New papers from DeepMind, Physical Intelligence, NVIDIA, and Chinese labs.

- Per-task data efficiency. How much trajectory data is needed for new task generalization.

- Industrial pilot conversion. Which humanoid pilots become recurring contracts.

- Battery/compute density curves. When all-day humanoid operation becomes feasible.

- Regulatory frameworks. Who is shaping in-home humanoid safety standards.

Bottom line

Embodied AI in 2026 is a serious, capital-rich, technically progressing field. The gap between investor expectations and deployed reality is wide, and most public demos do not survive an honest interrogation about teleoperation, environment structuring, or task generality. The companies that succeed will be the ones with the patience to ship industrial deployments first, build trajectory-data moats, and ride down the cost curve over years, not quarters.

Frequently Asked Questions

How autonomous are 2026 humanoid robots actually?

When will I be able to buy a useful home humanoid robot?

Why are humanoid robotics valuations so high in 2026?

Related Posts

Ready to automate customer conversations?

Launch AI voice agents and WhatsApp bots with CallMissed — one API, 22+ Indian languages.