AI's Power Grid Problem: 63GW and Counting

How AI is reshaping the US power grid in 2026 — AEP's 63GW pipeline, data center siting, nuclear renaissance, and what builders should know.

The most under-reported AI story of 2026 is not happening in San Francisco or in a lab. It is happening on transmission planning maps in Ohio, Texas, and Virginia, where AI-driven data center demand is reshaping the US power grid faster than anyone budgeted for. The numbers are staggering and they have practical implications for every AI builder.

The 63GW signal

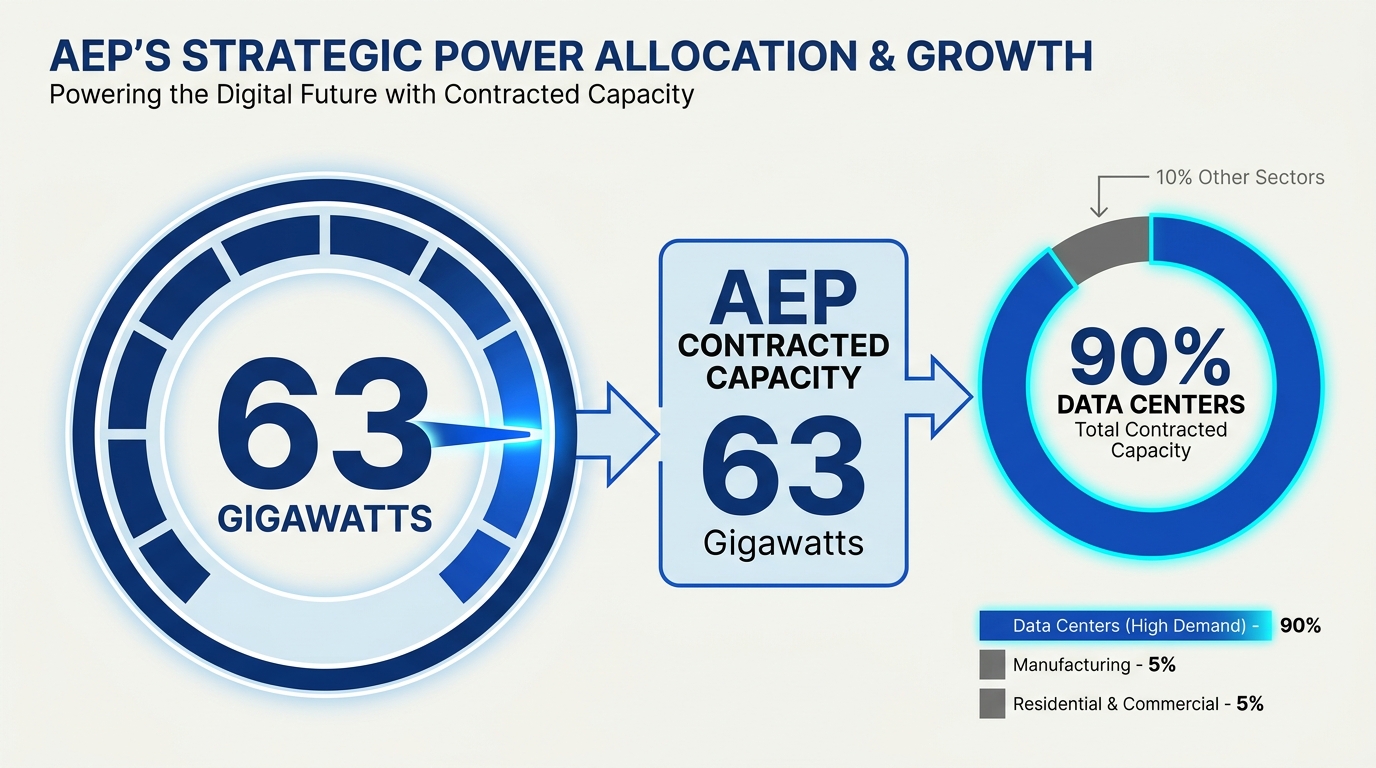

American Electric Power (AEP) reported that its pipeline of contracted capacity has surged to 63 gigawatts, with 90% of that demand from data center customers, per Data Center Dynamics. For context, 1 gigawatt is roughly the output of one mid-size nuclear reactor. AEP is one utility serving one region.

In Q1 2026 alone, AEP signed 7GW of new large-load agreements, primarily in Ohio and Texas. The PJM Interconnection grid that AEP serves has approximately 190GW of active interconnection queue, much of it data-center-driven. AEP expanded its capital plan by $6B to $78B, with $33B (42%) earmarked for transmission alone.

The broader market

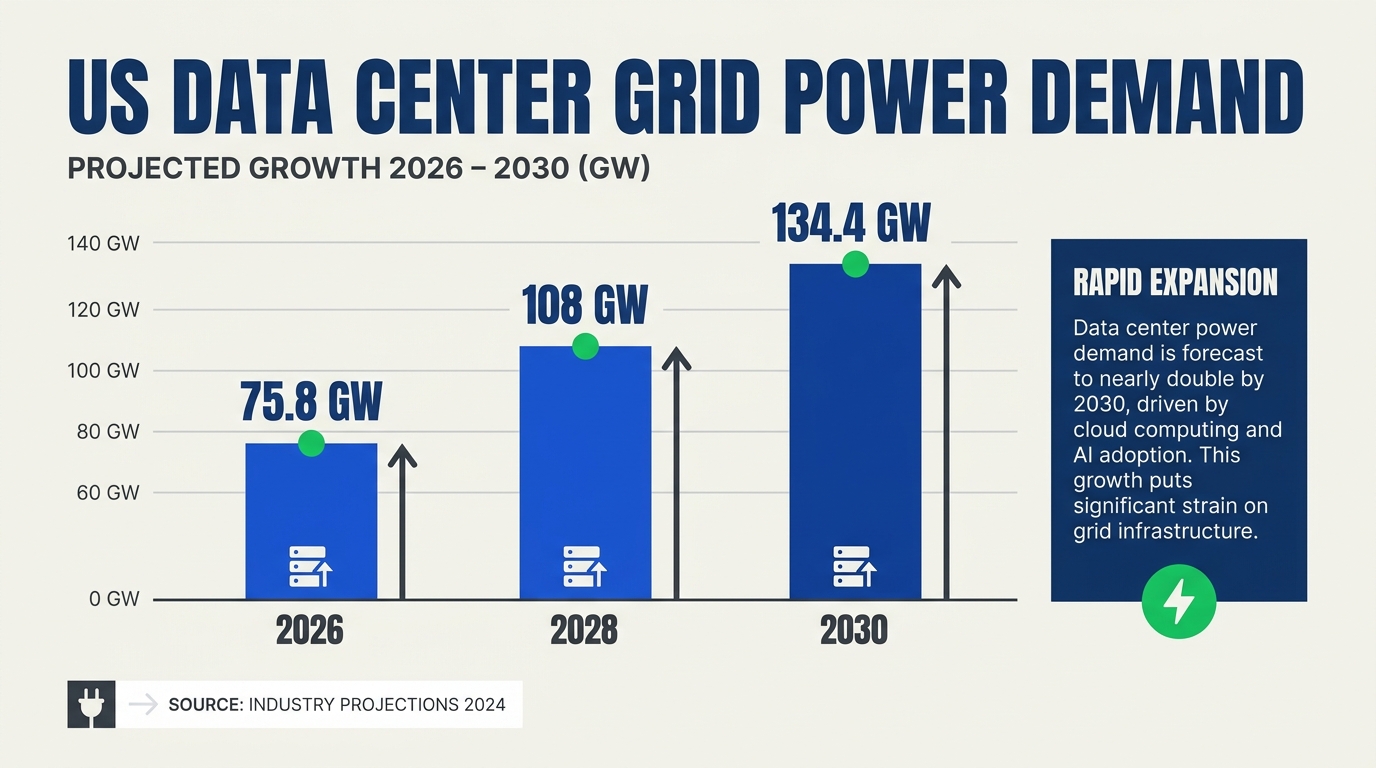

US data center grid-power demand is forecast to reach 75.8 GW for IT, cooling, lighting, and other uses in 2026, expanding to 108 GW in 2028 and 134.4 GW in 2030, per S&P Global Commodity Insights.

Texas alone projects power demand quadrupling by 2032 driven by data center growth, with the ERCOT interconnection queue reportedly at over 200GW.

These are not incremental numbers. They imply a multi-decade rebuild of the US grid that is not currently funded, planned, or permitted at scale.

Why this is happening now

Three forces converged:

1. Inference is the cost driver

Training a frontier model takes enormous compute, but training is one-shot. Inference is continuous and grows with usage. As AI products go to market, inference compute compounds. The same model that took 10MW-months to train can take 100MW-years to serve.

2. Density per rack has spiked

GPU racks pull 30-100 kW each, versus 5-15 kW for traditional servers. A single AI data center campus can demand more power than a city of 100,000 people.

3. Hyperscaler concentration

A handful of hyperscalers — Microsoft, Google, Amazon, Meta, Oracle — drive most demand. They prefer large campuses (1+ GW) clustered near grid capacity. This concentrates load, strains specific transmission nodes, and shifts pricing.

The supply response

Three categories of response are deploying:

Nuclear renaissance

Nearly every hyperscaler has signed nuclear PPAs since 2024 — Microsoft (Three Mile Island restart), Amazon (Talen), Google (Kairos SMR), Meta (RFP for SMR partners). The "nuclear renaissance" is real but slow: small modular reactors at scale are 5-10 year deployment timelines.

Natural gas

The fastest-deployable response. Multiple utilities are building or extending gas plants explicitly to serve data center load. This conflicts with corporate decarbonization commitments and is contested politically.

Behind-the-meter generation

Some campuses install on-site generation (gas turbines, fuel cells) to bypass grid constraints. Amazon's reported moves toward private power grids signal this shift.

Renewables + storage

Solar and wind capacity continues to grow but does not match data center load profiles cleanly (24/7 demand vs. variable supply). Long-duration storage is the gap; deployments are scaling but lag demand.

What this means for AI builders

You may not run a data center, but the grid story affects you in five practical ways:

1. Inference cost

Power is roughly 30-40% of data center operating cost. As power prices rise, inference prices follow. The frontier-model price decline of the last 3 years was driven by efficiency gains and competition; constrained power could slow or reverse that decline. [Inference]

2. Capacity availability

Hyperscaler GPU capacity is gated by data center capacity, which is gated by grid interconnection queues. "Sold-out" frontier model APIs during demand spikes are downstream of grid constraints, not just chip supply.

3. Geographic distribution

Where you deploy matters more in 2026 than it did in 2020. Some regions have plenty of capacity (Phoenix, Dallas-Fort Worth, parts of Virginia); others are sold out. Multi-region failover increasingly maps to grid availability.

4. Sustainability accounting

If your product carries sustainability commitments, your AI usage now has measurable carbon implications that go beyond your direct operations. The Scope 3 accounting picture for AI is being rebuilt.

5. Regulatory exposure

Some jurisdictions are starting to push back — moratoria on new data centers in some Virginia counties, debates over residential rate impacts, scrutiny of hyperscaler tax incentives. AI infrastructure is becoming politically contested.

The optimization angle

For builders, the practical response is efficiency:

- Cache aggressively. Avoid recomputing what you computed last week.

- Route by task complexity. Cheap models for cheap tasks; reserve frontier inference for hard ones.

- Batch and asynchronously process. Daily reports do not need real-time inference.

- Distill where possible. A 70B model fine-tune for your task may match a frontier model at 1/20 the cost.

- Measure cost per outcome, not cost per call. Optimize on the unit your business cares about.

These were already best practices for cost; they are increasingly best practices for grid responsibility.

Where this goes

[Speculation] Plausible scenarios for the next 5 years:

- Grid-led capability gap. Frontier capability that can be trained but not served at scale because of inference power constraints.

- Geographic divergence. Some regions become "AI hubs" because of grid availability; others lose AI infrastructure entirely.

- Power-aware product design. Products optimize architecture explicitly for power efficiency, similar to how mobile-first design optimized for battery.

- Long-duration storage breakthrough. A storage technology that can shape renewable supply to data-center demand profiles changes the economics significantly.

- Nuclear-AI bundling. Hyperscalers operate or co-own nuclear facilities at scale.

None of these are certain. All of them affect your AI infrastructure strategy.

Bottom line

The AI compute story has a hardware supply chain — chips, networking, cooling — that gets most of the press. The deeper supply chain is electricity, and the constraints there are real, multi-decade, and increasingly visible in headline numbers. AEP's 63GW pipeline is a number every AI builder should remember; it is one utility, one region, and one snapshot of a trend that is just getting started.

Frequently Asked Questions

Is the AI power demand really that large?

Will inference prices rise because of grid constraints?

What is the "nuclear renaissance" for AI?

Discussion

Related Posts

Ready to automate customer conversations?

Launch AI voice agents and WhatsApp bots with CallMissed — one API, 22+ Indian languages.